Advertisement

What Is China Sanjiang Fine Chemicals's (HKG:2198) P/E Ratio After Its Share Price Rocketed?

China Sanjiang Fine Chemicals (HKG:2198) shareholders are no doubt pleased to see that the share price has bounced 31% in the last month alone, although it is still down 5.3% over the last quarter. The bad news is that even after that recovery shareholders are still underwater by about 9.6% for the full year.

All else being equal, a sharp share price increase should make a stock less attractive to potential investors. In the long term, share prices tend to follow earnings per share, but in the short term prices bounce around in response to short term factors (which are not always obvious). The implication here is that deep value investors might steer clear when expectations of a company are too high. One way to gauge market expectations of a stock is to look at its Price to Earnings Ratio (PE Ratio). A high P/E ratio means that investors have a high expectation about future growth, while a low P/E ratio means they have low expectations about future growth.

See our latest analysis for China Sanjiang Fine Chemicals

Does China Sanjiang Fine Chemicals Have A Relatively High Or Low P/E For Its Industry?

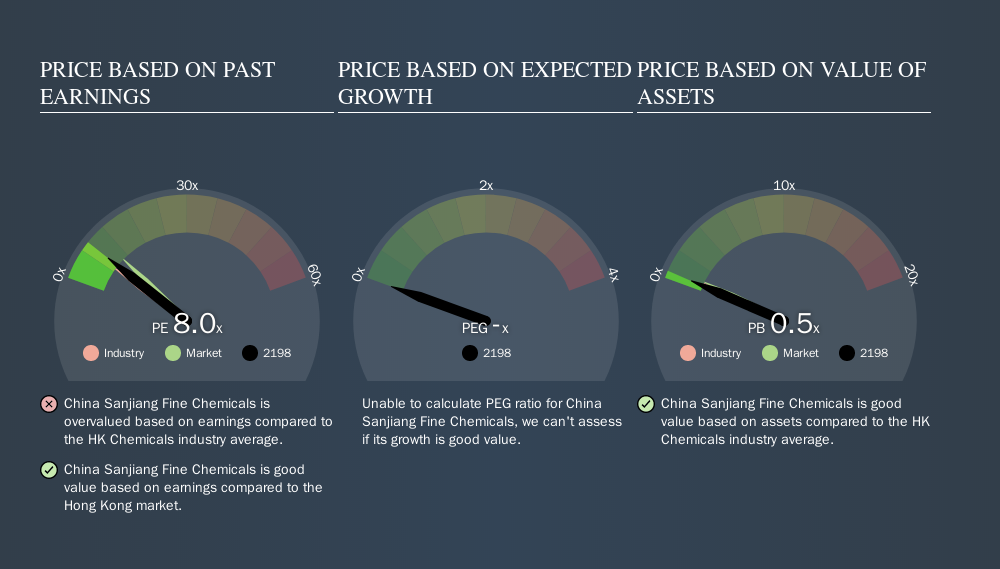

We can tell from its P/E ratio of 7.97 that there is some investor optimism about China Sanjiang Fine Chemicals. You can see in the image below that the average P/E (6.9) for companies in the chemicals industry is lower than China Sanjiang Fine Chemicals's P/E.

That means that the market expects China Sanjiang Fine Chemicals will outperform other companies in its industry.

How Growth Rates Impact P/E Ratios

Generally speaking the rate of earnings growth has a profound impact on a company's P/E multiple. If earnings are growing quickly, then the 'E' in the equation will increase faster than it would otherwise. That means even if the current P/E is high, it will reduce over time if the share price stays flat. So while a stock may look expensive based on past earnings, it could be cheap based on future earnings.

China Sanjiang Fine Chemicals's earnings per share fell by 75% in the last twelve months. And it has shrunk its earnings per share by 14% per year over the last five years. This could justify a pessimistic P/E. The company could impress by growing EPS, in the future. I would further inform my view by checking insider buying and selling., among other things.

A Limitation: P/E Ratios Ignore Debt and Cash In The Bank

One drawback of using a P/E ratio is that it considers market capitalization, but not the balance sheet. Thus, the metric does not reflect cash or debt held by the company. Hypothetically, a company could reduce its future P/E ratio by spending its cash (or taking on debt) to achieve higher earnings.

While growth expenditure doesn't always pay off, the point is that it is a good option to have; but one that the P/E ratio ignores.

So What Does China Sanjiang Fine Chemicals's Balance Sheet Tell Us?

Net debt totals a substantial 136% of China Sanjiang Fine Chemicals's market cap. This level of debt justifies a relatively low P/E, so remain cognizant of the debt, if you're comparing it to other stocks.

The Bottom Line On China Sanjiang Fine Chemicals's P/E Ratio

China Sanjiang Fine Chemicals has a P/E of 8.0. That's below the average in the HK market, which is 10.3. Given meaningful debt, and a lack of recent growth, the market looks to be extrapolating this recent performance; reflecting low expectations for the future. What we know for sure is that investors are becoming less uncomfortable about China Sanjiang Fine Chemicals's prospects, since they have pushed its P/E ratio from 6.1 to 8.0 over the last month. For those who like to invest in turnarounds, that might mean it's time to put the stock on a watchlist, or research it. But others might consider the opportunity to have passed.

Investors should be looking to buy stocks that the market is wrong about. If it is underestimating a company, investors can make money by buying and holding the shares until the market corrects itself. We don't have analyst forecasts, but you might want to assess this data-rich visualization of earnings, revenue and cash flow.

But note: China Sanjiang Fine Chemicals may not be the best stock to buy. So take a peek at this free list of interesting companies with strong recent earnings growth (and a P/E ratio below 20).

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About SEHK:2198

China Sanjiang Fine Chemicals

An investment holding company, manufactures and supplies ethylene oxide and glycol, propylene, polypropylene, methyl tert-butyl ether (MTBE), surfactants, and ethanolamine in Mainland China, Japan, and Singapore, and internationally.

Proven track record and slightly overvalued.

Market Insights

Advertisement

Community Narratives

Vita Life Sciences Set for a 12.72% Revenue Growth While Tackling Operational Challenges

Fair Value AU$2.42|9.5% undervalued

RO

Community Contributor

Vossloh rides a €500 billion wave to boost growth and earnings in the next decade

Fair Value €78.41|7.2% undervalued

CH

Community Contributor

Intuitive Surgical Will Transform Healthcare with 12% Revenue Growth

Fair Value US$325.55|56.5% overvalued

UN

Community Contributor