Advertisement

AAK AB (publ.) (STO:AAK), which is in the food business, and is based in Sweden, saw a decent share price growth in the teens level on the OM over the last few months. With many analysts covering the mid-cap stock, we may expect any price-sensitive announcements have already been factored into the stock’s share price. However, could the stock still be trading at a relatively cheap price? Let’s examine AAK AB (publ.)’s valuation and outlook in more detail to determine if there’s still a bargain opportunity.

Check out our latest analysis for AAK AB (publ.)

What's the opportunity in AAK AB (publ.)?

AAK AB (publ.) appears to be overvalued by 24% at the moment, based on my discounted cash flow valuation. The stock is currently priced at kr158 on the market compared to my intrinsic value of SEK127.56. Not the best news for investors looking to buy! Another thing to keep in mind is that AAK AB (publ.)’s share price is quite stable relative to the market, as indicated by its low beta. This means that if you believe the current share price should move towards its intrinsic value over time, a low beta could suggest it is not likely to reach that level anytime soon, and once it’s there, it may be hard to fall back down into an attractive buying range again.

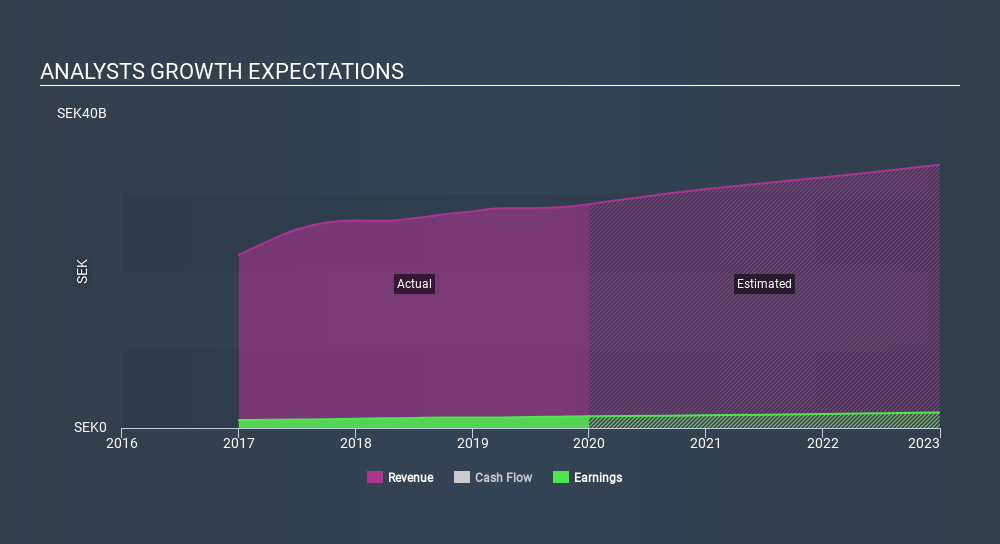

What kind of growth will AAK AB (publ.) generate?

Investors looking for growth in their portfolio may want to consider the prospects of a company before buying its shares. Although value investors would argue that it’s the intrinsic value relative to the price that matter the most, a more compelling investment thesis would be high growth potential at a cheap price. AAK AB (publ.)’s earnings over the next few years are expected to increase by 32%, indicating a highly optimistic future ahead. This should lead to more robust cash flows, feeding into a higher share value.

What this means for you:

Are you a shareholder? It seems like the market has well and truly priced in AAK’s positive outlook, with shares trading above its fair value. However, this brings up another question – is now the right time to sell? If you believe AAK should trade below its current price, selling high and buying it back up again when its price falls towards its real value can be profitable. But before you make this decision, take a look at whether its fundamentals have changed.

Are you a potential investor? If you’ve been keeping an eye on AAK for a while, now may not be the best time to enter into the stock. The price has surpassed its true value, which means there’s no upside from mispricing. However, the positive outlook is encouraging for AAK, which means it’s worth diving deeper into other factors in order to take advantage of the next price drop.

Price is just the tip of the iceberg. Dig deeper into what truly matters – the fundamentals – before you make a decision on AAK AB (publ.). You can find everything you need to know about AAK AB (publ.) in the latest infographic research report. If you are no longer interested in AAK AB (publ.), you can use our free platform to see my list of over 50 other stocks with a high growth potential.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About OM:AAK

AAK AB (publ.)

Develops and sells plant-based oils and fats in Sweden and internationally.

Undervalued with excellent balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Weekly Picks

JO

Jolt_Communications on ZenaTech ·

ZenaTech: A big bet on the rise of AI drones and drones-as-a-service

Fair Value:US$6.8569.9% undervalued

28 followersusers have followed this narrative

0 commentsusers have commented on this narrative

4 likesusers have liked this narrative

TR

tripledub on Intuit ·

A Wonderful Business at a Not-So-Wonderful Price

Fair Value:US$50016.7% undervalued

20 followersusers have followed this narrative

0 commentsusers have commented on this narrative

18 likesusers have liked this narrative

FA

FA_Trader on A1 A.K. Koh Group Berhad ·

A1 A.K. Koh Group Berhad: A simple local food story that could ride on Visit Malaysia 2026

Fair Value:RM 0.3343.9% undervalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

KA

kaladorm on American Integrity Insurance Group ·

Priced for worse weather, but undervalued even for a high hurricane season

Fair Value:US$37.1949.9% undervalued

10 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

Recently Updated Narratives

TR

tripledub on Microsoft ·

Everyone's Terrified Microsoft Will Keep Spending. I'm Terrified They'll Stop.

Fair Value:US$3959.7% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RI

richardfoot on Everest Metals ·

The long game for Everest metals

Fair Value:AU$0.011900.0% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VE

Vestra on Analog Devices ·

ADI: Bridging the Physical and Digital in a Cyclical Super-Recovery

Fair Value:US$40223.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

YA

Yang_ on SoFi Technologies ·

SoFi Technologies: The Apex Aggregator and the Infrastructure of the Modern Financial System

Fair Value:US$22.9833.7% undervalued

49 followersusers have followed this narrative

0 commentsusers have commented on this narrative

36 likesusers have liked this narrative

PD

pdixit1 on Vertiv Holdings Co ·

The Infrastructure AI Cannot Be Built Without

Fair Value:US$408.6438.6% undervalued

40 followersusers have followed this narrative

3 commentsusers have commented on this narrative

18 likesusers have liked this narrative

ZA

ZayaanS on Pro Medicus ·

Pro Medicus: The Market Is Confusing a Lumpy Quarter With a Broken Business

Fair Value:AU$196.7840.2% undervalued

33 followersusers have followed this narrative

7 commentsusers have commented on this narrative

21 likesusers have liked this narrative

Trending Discussion

DS

dsfaggafgafg on Micron Technology ·

This is truly one of the worst predictions of all time. Its forward PE is 3.9x.

0

|0