Advertisement

We Wouldn't Rely On Wuxi Sunlit Science and Technology's (HKG:1289) Statutory Earnings As A Guide

Statistically speaking, it is less risky to invest in profitable companies than in unprofitable ones. Having said that, sometimes statutory profit levels are not a good guide to ongoing profitability, because some short term one-off factor has impacted profit levels. This article will consider whether Wuxi Sunlit Science and Technology's (HKG:1289) statutory profits are a good guide to its underlying earnings.

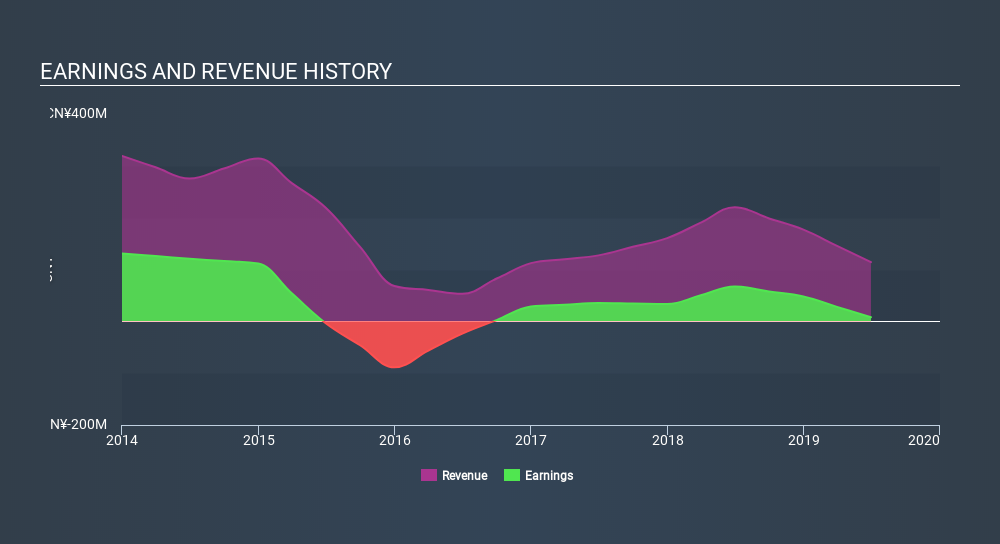

It's good to see that over the last twelve months Wuxi Sunlit Science and Technology made a profit of CN¥7.89m on revenue of CN¥114.3m. The good news is that the company managed to grow its revenue over the last three years, and also move from loss-making to profitable.

See our latest analysis for Wuxi Sunlit Science and Technology

Not all profits are equal, and we can learn more about the nature of a company's past profitability by diving deeper into the financial statements. This article will focus on the impact unusual items have had on Wuxi Sunlit Science and Technology's statutory earnings. Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of Wuxi Sunlit Science and Technology.

The Impact Of Unusual Items On Profit

Importantly, our data indicates that Wuxi Sunlit Science and Technology's profit received a boost of CN¥2.6m in unusual items, over the last year. While it's always nice to have higher profit, a large contribution from unusual items sometimes dampens our enthusiasm. When we analysed the vast majority of listed companies worldwide, we found that significant unusual items are often not repeated. And that's as you'd expect, given these boosts are described as 'unusual'. Wuxi Sunlit Science and Technology had a rather significant contribution from unusual items relative to its profit to June 2019. All else being equal, this would likely have the effect of making the statutory profit a poor guide to underlying earnings power.

Our Take On Wuxi Sunlit Science and Technology's Profit Performance

As we discussed above, we think the significant positive unusual item makes Wuxi Sunlit Science and Technology's earnings a poor guide to its underlying profitability. For this reason, we think that Wuxi Sunlit Science and Technology's statutory profits may be a bad guide to its underlying earnings power, and might give investors an overly positive impression of the company. Sadly, its EPS was down over the last twelve months. The goal of this article has been to assess how well we can rely on the statutory earnings to reflect the company's potential, but there is plenty more to consider. Just as investors must consider earnings, it is also important to take into account the strength of a company's balance sheet. If you're interestedwe have a graphic representation of Wuxi Sunlit Science and Technology's balance sheet.

This note has only looked at a single factor that sheds light on the nature of Wuxi Sunlit Science and Technology's profit. But there is always more to discover if you are capable of focussing your mind on minutiae. For example, many people consider a high return on equity as an indication of favorable business economics, while others like to 'follow the money' and search out stocks that insiders are buying. While it might take a little research on your behalf, you may find this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying to be useful.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About SEHK:1289

Wuxi Sunlit Science and Technology

Engages in the research and development, design, supply, installation, testing, repair, and maintenance of production lines for manufacturing steel wire products in the People’s Republic of China.

Flawless balance sheet with solid track record.

Market Insights

Advertisement

Community Narratives

Vita Life Sciences Set for a 12.72% Revenue Growth While Tackling Operational Challenges

Fair Value AU$2.42|9.1% undervalued

RO

Community Contributor

Vossloh rides a €500 billion wave to boost growth and earnings in the next decade

Fair Value €78.41|5.2% undervalued

CH

Community Contributor

Intuitive Surgical Will Transform Healthcare with 12% Revenue Growth

Fair Value US$325.55|57.3% overvalued

UN

Community Contributor