Advertisement

- Hong Kong

- /

- Real Estate

- /

- SEHK:2048

We Wouldn't Rely On E-House (China) Enterprise Holdings's (HKG:2048) Statutory Earnings As A Guide

It might be old fashioned, but we really like to invest in companies that make a profit, each and every year. Having said that, sometimes statutory profit levels are not a good guide to ongoing profitability, because some short term one-off factor has impacted profit levels. In this article, we'll look at how useful this year's statutory profit is, when analysing E-House (China) Enterprise Holdings (HKG:2048).

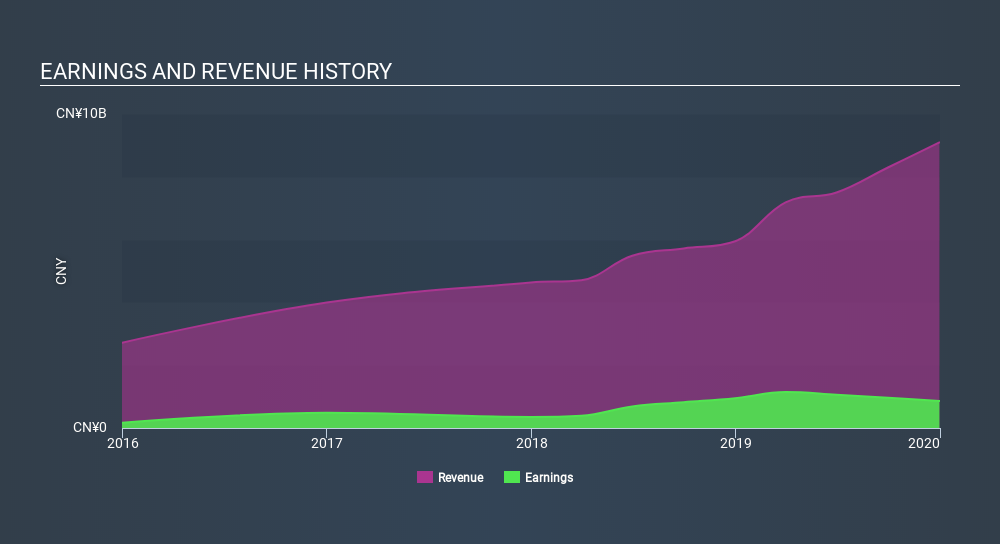

While E-House (China) Enterprise Holdings was able to generate revenue of CN¥9.09b in the last twelve months, we think its profit result of CN¥860.9m was more important. Happily, it has grown both its profit and revenue over the last three years (though we note its profit is down over the last year).

See our latest analysis for E-House (China) Enterprise Holdings

Of course, when it comes to statutory profit, the devil is often in the detail, and we can get a better sense for a company by diving deeper into the financial statements. So today we'll look at what E-House (China) Enterprise Holdings's cashflow and unusual items tell us about the quality of its earnings, as well as touching on how its recent share issues are impacting shareholders. That might leave you wondering what analysts are forecasting in terms of future profitability. Luckily, you can click here to see an interactive graph depicting future profitability, based on their estimates.

A Closer Look At E-House (China) Enterprise Holdings's Earnings

As finance nerds would already know, the accrual ratio from cashflow is a key measure for assessing how well a company's free cash flow (FCF) matches its profit. The accrual ratio subtracts the FCF from the profit for a given period, and divides the result by the average operating assets of the company over that time. The ratio shows us how much a company's profit exceeds its FCF.

As a result, a negative accrual ratio is a positive for the company, and a positive accrual ratio is a negative. While having an accrual ratio above zero is of little concern, we do think it's worth noting when a company has a relatively high accrual ratio. Notably, there is some academic evidence that suggests that a high accrual ratio is a bad sign for near-term profits, generally speaking.

E-House (China) Enterprise Holdings has an accrual ratio of 0.21 for the year to December 2019. We can therefore deduce that its free cash flow fell well short of covering its statutory profit. In the last twelve months it actually had negative free cash flow, with an outflow of CN¥825m despite its profit of CN¥860.9m, mentioned above. Coming off the back of negative free cash flow last year, we imagine some shareholders might wonder if its cash burn of CN¥825m, this year, indicates high risk. However, that's not the end of the story. We can look at how unusual items in the profit and loss statement impacted its accrual ratio, as well as explore how dilution is impacting shareholders negatively.

One essential aspect of assessing earnings quality is to look at how much a company is diluting shareholders. In fact, E-House (China) Enterprise Holdings increased the number of shares on issue by 21% over the last twelve months by issuing new shares. Therefore, each share now receives a smaller portion of profit. Per share metrics like EPS help us understand how much actual shareholders are benefitting from the company's profits, while the net income level gives us a better view of the company's absolute size. You can see a chart of E-House (China) Enterprise Holdings's EPS by clicking here.

A Look At The Impact Of E-House (China) Enterprise Holdings's Dilution on Its Earnings Per Share (EPS).

As you can see above, E-House (China) Enterprise Holdings has been growing its net income over the last few years, with an annualized gain of 77% over three years. In comparison, earnings per share only gained 14% over the same period. Net profit actually dropped by 9.4% in the last year. Unfortunately for shareholders, though, the earnings per share result was even worse, declining 25%. So you can see that the dilution has had a bit of an impact on shareholders. Therefore, the dilution is having a noteworthy influence on shareholder returns. And so, you can see quite clearly that dilution is influencing shareholder earnings.

If E-House (China) Enterprise Holdings's EPS can grow over time then that drastically improves the chances of the share price moving in the same direction. But on the other hand, we'd be far less excited to learn profit (but not EPS) was improving. For the ordinary retail shareholder, EPS is a great measure to check your hypothetical "share" of the company's profit.

How Do Unusual Items Influence Profit?

The fact that the company had unusual items boosting profit by CN¥151m, in the last year, probably goes some way to explain why its accrual ratio was so weak. While we like to see profit increases, we tend to be a little more cautious when unusual items have made a big contribution. When we crunched the numbers on thousands of publicly listed companies, we found that a boost from unusual items in a given year is often not repeated the next year. And, after all, that's exactly what the accounting terminology implies. Assuming those unusual items don't show up again in the current year, we'd thus expect profit to be weaker next year (in the absence of business growth, that is).

Our Take On E-House (China) Enterprise Holdings's Profit Performance

E-House (China) Enterprise Holdings didn't back up its earnings with free cashflow, but this isn't too surprising given profits were inflated by unusual items. Meanwhile, the new shares issued mean that shareholders now own less of the company, unless they tipped in more cash themselves. For the reasons mentioned above, we think that a perfunctory glance at E-House (China) Enterprise Holdings's statutory profits might make it look better than it really is on an underlying level. With this in mind, we wouldn't consider investing in a stock unless we had a thorough understanding of the risks. For example, we've found that E-House (China) Enterprise Holdings has 4 warning signs (2 are potentially serious!) that deserve your attention before going any further with your analysis.

Our examination of E-House (China) Enterprise Holdings has focussed on certain factors that can make its earnings look better than they are. And, on that basis, we are somewhat skeptical. But there is always more to discover if you are capable of focussing your mind on minutiae. Some people consider a high return on equity to be a good sign of a quality business. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About SEHK:2048

E-House (China) Enterprise Holdings

An investment holding company, provides real estate transaction services in China.

Low and slightly overvalued.

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|35.9% undervalued

JO

Community Contributor

Occidental Petroleum is set to achieve a 16% profit margin improvement

Fair Value US$55.05|15.6% undervalued

DZ

Community Contributor

Argan's Revenue Set to Soar with a 13.31% Growth in the Coming Decade

Fair Value US$284.68|23.4% undervalued

KE

Community Contributor

EU#1 - From German Startup to EU’s Biggest Company

Fair Value €248.62|2.5% overvalued

TO

Community Contributor