Advertisement

- United States

- /

- Pharma

- /

- NasdaqGM:ETON

We Think Eton Pharmaceuticals (NASDAQ:ETON) Needs To Drive Business Growth Carefully

We can readily understand why investors are attracted to unprofitable companies. For example, although Amazon.com made losses for many years after listing, if you had bought and held the shares since 1999, you would have made a fortune. Having said that, unprofitable companies are risky because they could potentially burn through all their cash and become distressed.

So, the natural question for Eton Pharmaceuticals (NASDAQ:ETON) shareholders is whether they should be concerned by its rate of cash burn. In this report, we will consider the company's annual negative free cash flow, henceforth referring to it as the 'cash burn'. First, we'll determine its cash runway by comparing its cash burn with its cash reserves.

See our latest analysis for Eton Pharmaceuticals

Does Eton Pharmaceuticals Have A Long Cash Runway?

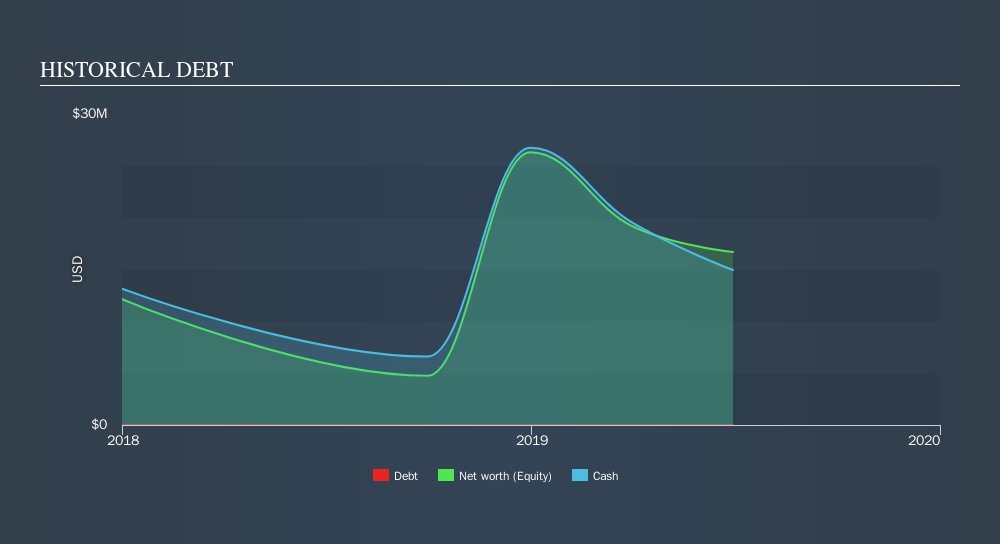

A company's cash runway is the amount of time it would take to burn through its cash reserves at its current cash burn rate. When Eton Pharmaceuticals last reported its balance sheet in June 2019, it had zero debt and cash worth US$15m. Looking at the last year, the company burnt through US$16m. That means it had a cash runway of around 11 months as of June 2019. Notably, analysts forecast that Eton Pharmaceuticals will break even (at a free cash flow level) in about 3 years. That means unless the company reduces its cash burn quickly, it may well look to raise more cash. Depicted below, you can see how its cash holdings have changed over time.

How Is Eton Pharmaceuticals's Cash Burn Changing Over Time?

Whilst it's great to see that Eton Pharmaceuticals has already begun generating revenue from operations, last year it only produced US$500k, so we don't think it is generating significant revenue, at this point. Therefore, for the purposes of this analysis we'll focus on how the cash burn is tracking. During the last twelve months, its cash burn actually ramped up 77%. While this spending increase is no doubt intended to drive growth, if the trend continues the company's cash runway will shrink very quickly. Clearly, however, the crucial factor is whether the company will grow its business going forward. So you might want to take a peek at how much the company is expected to grow in the next few years.

Can Eton Pharmaceuticals Raise More Cash Easily?

Since its cash burn is moving in the wrong direction, Eton Pharmaceuticals shareholders may wish to think ahead to when the company may need to raise more cash. Companies can raise capital through either debt or equity. Commonly, a business will sell new shares in itself to raise cash to drive growth. By comparing a company's annual cash burn to its total market capitalisation, we can estimate roughly how many shares it would have to issue in order to run the company for another year (at the same burn rate).

Eton Pharmaceuticals's cash burn of US$16m is about 14% of its US$112m market capitalisation. As a result, we'd venture that the company could raise more cash for growth without much trouble, albeit at the cost of some dilution.

Is Eton Pharmaceuticals's Cash Burn A Worry?

On this analysis of Eton Pharmaceuticals's cash burn, we think its cash burn relative to its market cap was reassuring, while its increasing cash burn has us a bit worried. Shareholders can take heart from the fact that analysts are forecasting it will reach breakeven. Summing up, we think the Eton Pharmaceuticals's cash burn is a risk, based on the factors we mentioned in this article. When you don't have traditional metrics like earnings per share and free cash flow to value a company, many are extra motivated to consider qualitative factors such as whether insiders are buying or selling shares. Please Note: Eton Pharmaceuticals insiders have been trading shares, according to our data. Click here to check whether insiders have been buying or selling.

Of course, you might find a fantastic investment by looking elsewhere. So take a peek at this free list of companies insiders are buying, and this list of stocks growth stocks (according to analyst forecasts)

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About NasdaqGM:ETON

Eton Pharmaceuticals

A pharmaceutical company, focuses on developing and commercializing treatments for rare diseases.

High growth potential and fair value.

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|36.2% undervalued

JO

Community Contributor

Occidental Petroleum is set to achieve a 16% profit margin improvement

Fair Value US$55.05|17.7% undervalued

DZ

Community Contributor

Argan's Revenue Set to Soar with a 13.31% Growth in the Coming Decade

Fair Value US$284.68|23.2% undervalued

KE

Community Contributor

EU#1 - From German Startup to EU’s Biggest Company

Fair Value €248.62|3.6% overvalued

TO

Community Contributor