Advertisement

- United States

- /

- Commercial Services

- /

- NYSE:BCO

The Brink's Company Earnings Missed Analyst Estimates: Here's What Analysts Are Forecasting Now

Last week saw the newest full-year earnings release from The Brink's Company (NYSE:BCO), an important milestone in the company's journey to build a stronger business. It looks like a pretty bad result, all things considered. Although revenues of US$3.7b were in line with analyst predictions, statutory earnings fell badly short, missing estimates by 57% to hit US$0.55 per share. This is an important time for investors, as they can track a company's performance in its report, look at what top analysts are forecasting for next year, and see if there has been any change to expectations for the business. So we collected the latest post-earnings statutory consensus estimates to see what could be in store for next year.

View our latest analysis for Brink's

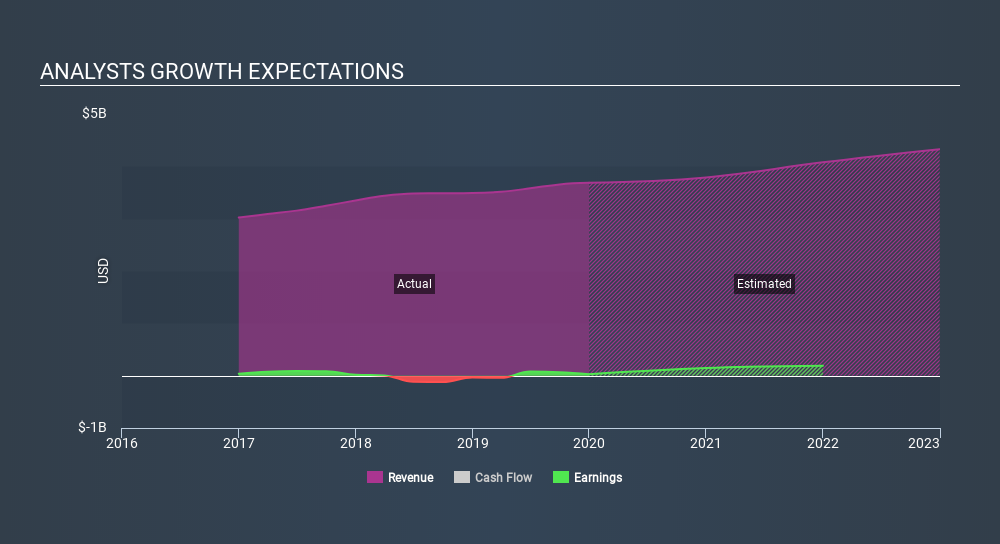

Taking into account the latest results, the latest consensus from Brink's's five analysts is for revenues of US$3.79b in 2020, which would reflect an okay 2.8% improvement in sales compared to the last 12 months. Statutory earnings per share are expected to jump 615% to US$3.92. Before this earnings report, analysts had been forecasting revenues of US$3.90b and earnings per share (EPS) of US$4.52 in 2020. From this we can that analyst sentiment has definitely become more bearish after the latest results, leading to lower revenue forecasts and a real cut to earnings per share estimates.

Despite the cuts to forecast earnings, there was no real change to the US$108 price target, showing that analysts don't think the changes have a meaningful impact on the stock's intrinsic value. There's another way to think about price targets though, and that's to look at the range of price targets put forward by analysts, because a wide range of estimates could suggest a diverse view on possible outcomes for the business. Currently, the most bullish analyst values Brink's at US$116 per share, while the most bearish prices it at US$100.00. The narrow spread of estimates could suggest that the business' future is relatively easy to value, or that analysts have a clear view on its prospects.

One way to get more context on these forecasts is to look at how they compare to both past performance, and how other companies in the same industry are performing. Next year brings more of the same, according to analysts, with revenue forecast to grow 2.8%, in line with its 2.7% annual growth over the past five years. By contrast, our data suggests that other companies (with analyst coverage) in a similar industry are forecast to see their revenues grow 5.2% per year. So it's pretty clear that Brink's is expected to grow slower than similar companies in the same market.

The Bottom Line

The most important thing to take away is that analysts downgraded their earnings per share estimates, showing that there has been a clear decline in sentiment following these results. Unfortunately, analysts also downgraded their revenue estimates, and our data indicates revenues are expected to perform worse than the wider market. Even so, earnings per share are more important to the intrinsic value of the business. There was no real change to the consensus price target, suggesting that the intrinsic value of the business has not undergone any major changes with the latest estimates.

With that in mind, we wouldn't be too quick to come to a conclusion on Brink's. Long-term earnings power is much more important than next year's profits. We have forecasts for Brink's going out to 2022, and you can see them free on our platform here.

You can also view our analysis of Brink's's balance sheet, and whether we think Brink's is carrying too much debt, for free on our platform here.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About NYSE:BCO

Brink's

Provides cash and valuables management, digital retail solutions, and automated teller machines (ATM) managed services in North America, Latin America, Europe, and internationally.

Solid track record average dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

Vita Life Sciences Set for a 12.72% Revenue Growth While Tackling Operational Challenges

Fair Value AU$2.42|9.5% undervalued

RO

Community Contributor

Vossloh rides a €500 billion wave to boost growth and earnings in the next decade

Fair Value €78.41|6.1% undervalued

CH

Community Contributor

Intuitive Surgical Will Transform Healthcare with 12% Revenue Growth

Fair Value US$325.55|56.5% overvalued

UN

Community Contributor