Stock Analysis

- India

- /

- Electrical

- /

- NSEI:PITTIENG

Should You Be Impressed By Pitti Engineering's (NSE:PITTIENG) Returns on Capital?

There are a few key trends to look for if we want to identify the next multi-bagger. Ideally, a business will show two trends; firstly a growing return on capital employed (ROCE) and secondly, an increasing amount of capital employed. Ultimately, this demonstrates that it's a business that is reinvesting profits at increasing rates of return. That's why when we briefly looked at Pitti Engineering's (NSE:PITTIENG) ROCE trend, we were pretty happy with what we saw.

What is Return On Capital Employed (ROCE)?

For those who don't know, ROCE is a measure of a company's yearly pre-tax profit (its return), relative to the capital employed in the business. The formula for this calculation on Pitti Engineering is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

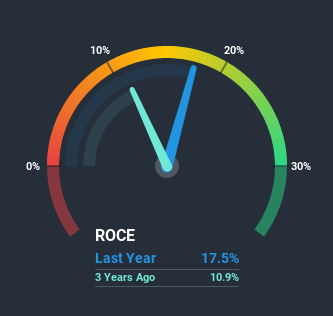

0.18 = ₹540m ÷ (₹6.0b - ₹2.9b) (Based on the trailing twelve months to March 2020).

Thus, Pitti Engineering has an ROCE of 18%. On its own, that's a standard return, however it's much better than the 12% generated by the Electrical industry.

View our latest analysis for Pitti Engineering

While the past is not representative of the future, it can be helpful to know how a company has performed historically, which is why we have this chart above. If you're interested in investigating Pitti Engineering's past further, check out this free graph of past earnings, revenue and cash flow.

The Trend Of ROCE

While the returns on capital are good, they haven't moved much. The company has employed 105% more capital in the last five years, and the returns on that capital have remained stable at 18%. 18% is a pretty standard return, and it provides some comfort knowing that Pitti Engineering has consistently earned this amount. Stable returns in this ballpark can be unexciting, but if they can be maintained over the long run, they often provide nice rewards to shareholders.

On a side note, Pitti Engineering has done well to reduce current liabilities to 48% of total assets over the last five years. This can eliminate some of the risks inherent in the operations because the business has less outstanding obligations to their suppliers and or short-term creditors than they did previously. We'd like to see this trend continue though because as it stands today, thats still a pretty high level.The Bottom Line On Pitti Engineering's ROCE

The main thing to remember is that Pitti Engineering has proven its ability to continually reinvest at respectable rates of return. Yet over the last five years the stock has declined 56%, so the decline might provide an opening. For that reason, savvy investors might want to look further into this company in case it's a prime investment.

One more thing: We've identified 3 warning signs with Pitti Engineering (at least 1 which is concerning) , and understanding these would certainly be useful.

While Pitti Engineering isn't earning the highest return, check out this free list of companies that are earning high returns on equity with solid balance sheets.

If you decide to trade Pitti Engineering, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Valuation is complex, but we're helping make it simple.

Find out whether Pitti Engineering is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About NSEI:PITTIENG

Pitti Engineering

Manufactures and sells iron and steel engineering products in India.

Exceptional growth potential with proven track record.