Advertisement

- Australia

- /

- Healthcare Services

- /

- ASX:PSQ

Should We Worry About Pacific Smiles Group Limited's (ASX:PSQ) P/E Ratio?

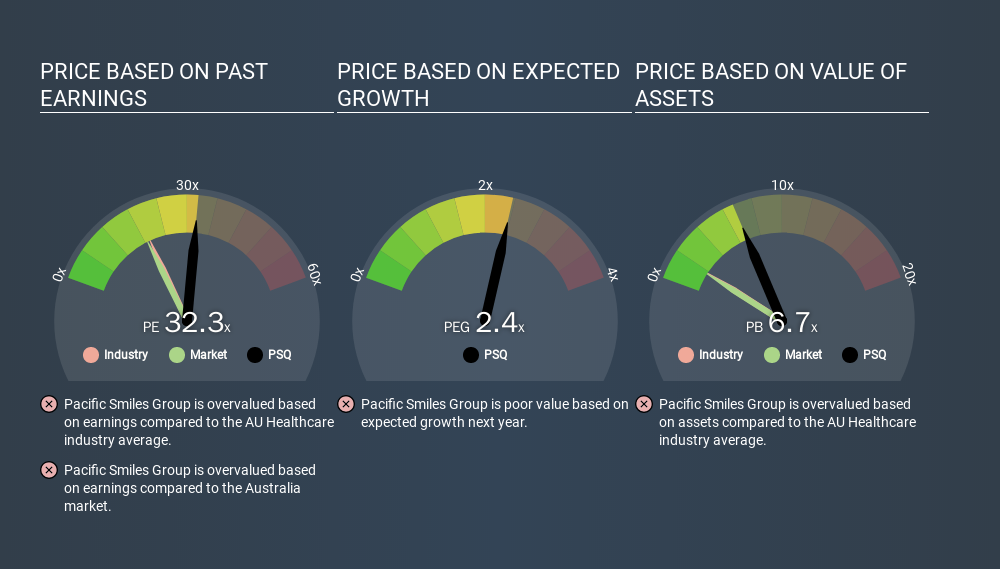

Today, we'll introduce the concept of the P/E ratio for those who are learning about investing. We'll look at Pacific Smiles Group Limited's (ASX:PSQ) P/E ratio and reflect on what it tells us about the company's share price. Looking at earnings over the last twelve months, Pacific Smiles Group has a P/E ratio of 32.27. That is equivalent to an earnings yield of about 3.1%.

View our latest analysis for Pacific Smiles Group

How Do I Calculate A Price To Earnings Ratio?

The formula for price to earnings is:

Price to Earnings Ratio = Share Price ÷ Earnings per Share (EPS)

Or for Pacific Smiles Group:

P/E of 32.27 = AUD1.82 ÷ AUD0.06 (Based on the trailing twelve months to June 2019.)

Is A High Price-to-Earnings Ratio Good?

A higher P/E ratio implies that investors pay a higher price for the earning power of the business. That isn't necessarily good or bad, but a high P/E implies relatively high expectations of what a company can achieve in the future.

Does Pacific Smiles Group Have A Relatively High Or Low P/E For Its Industry?

We can get an indication of market expectations by looking at the P/E ratio. The image below shows that Pacific Smiles Group has a higher P/E than the average (19.2) P/E for companies in the healthcare industry.

Pacific Smiles Group's P/E tells us that market participants think the company will perform better than its industry peers, going forward. Clearly the market expects growth, but it isn't guaranteed. So further research is always essential. I often monitor director buying and selling.

How Growth Rates Impact P/E Ratios

If earnings fall then in the future the 'E' will be lower. Therefore, even if you pay a low multiple of earnings now, that multiple will become higher in the future. So while a stock may look cheap based on past earnings, it could be expensive based on future earnings.

Pacific Smiles Group increased earnings per share by a whopping 30% last year. But earnings per share are down 4.7% per year over the last three years.

A Limitation: P/E Ratios Ignore Debt and Cash In The Bank

The 'Price' in P/E reflects the market capitalization of the company. In other words, it does not consider any debt or cash that the company may have on the balance sheet. In theory, a company can lower its future P/E ratio by using cash or debt to invest in growth.

While growth expenditure doesn't always pay off, the point is that it is a good option to have; but one that the P/E ratio ignores.

Is Debt Impacting Pacific Smiles Group's P/E?

Net debt totals just 3.6% of Pacific Smiles Group's market cap. The market might award it a higher P/E ratio if it had net cash, but its unlikely this low level of net borrowing is having a big impact on the P/E multiple.

The Bottom Line On Pacific Smiles Group's P/E Ratio

Pacific Smiles Group's P/E is 32.3 which is above average (18.6) in its market. The company is not overly constrained by its modest debt levels, and its recent EPS growth very solid. So on this analysis it seems reasonable that its P/E ratio is above average.

When the market is wrong about a stock, it gives savvy investors an opportunity. As value investor Benjamin Graham famously said, 'In the short run, the market is a voting machine but in the long run, it is a weighing machine. So this free visualization of the analyst consensus on future earnings could help you make the right decision about whether to buy, sell, or hold.

Of course, you might find a fantastic investment by looking at a few good candidates. So take a peek at this free list of companies with modest (or no) debt, trading on a P/E below 20.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About ASX:PSQ

Pacific Smiles Group

Owns and operates dental centers under the Pacific Smiles Dental Centres and Nib Dental Care Centres names in Australia.

High growth potential with adequate balance sheet.

Market Insights

Advertisement

Community Narratives

Vita Life Sciences Set for a 12.72% Revenue Growth While Tackling Operational Challenges

Fair Value AU$2.42|9.1% undervalued

RO

Community Contributor

Vossloh rides a €500 billion wave to boost growth and earnings in the next decade

Fair Value €78.41|6.1% undervalued

CH

Community Contributor

Intuitive Surgical Will Transform Healthcare with 12% Revenue Growth

Fair Value US$325.55|57.3% overvalued

UN

Community Contributor