Advertisement

- United States

- /

- Trade Distributors

- /

- NYSE:WSO

Read This Before Considering Watsco, Inc. (NYSE:WSO) For Its Upcoming 1.0% Dividend

Want to participate in a short research study? Help shape the future of investing tools and you could win a $250 gift card!

Watsco, Inc. (NYSE:WSO) stock is about to trade ex-dividend in 2 days time. Investors can purchase shares before the 15th of July in order to be eligible for this dividend, which will be paid on the 31st of July.

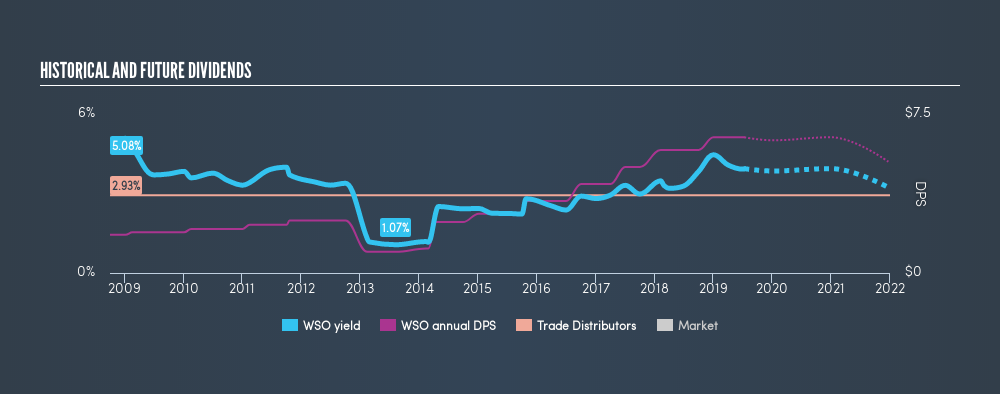

Watsco's next dividend payment will be US$1.60 per share, and in the last 12 months, the company paid a total of US$6.40 per share. Based on the last year's worth of payments, Watsco stock has a trailing yield of around 3.9% on the current share price of $162.58. If you buy this business for its dividend, you should have an idea of whether Watsco's dividend is reliable and sustainable. As a result, readers should always check whether Watsco has been able to grow its dividends, or if the dividend might be cut.

See our latest analysis for Watsco

Dividends are typically paid from company earnings. If a company pays more in dividends than it earned in profit, then the dividend could be unsustainable. Last year Watsco paid out 92% of its profits as dividends to shareholders, suggesting the dividend is not well covered by earnings. Yet cash flow is typically more important than profit for assessing dividend sustainability, so we should always check if the company generated enough cash to afford its dividend. The company paid out 90% of its free cash flow over the last year, which we think is outside the ideal range for most businesses. Companies usually need cash more than they need earnings - expenses don't pay themselves - so it's not great to see it paying out so much of its cash flow.

Cash is slightly more important than profit from a dividend perspective, but given Watsco's payouts were not well covered by either earnings or cash flow, we would be concerned about the sustainability of this dividend.

Click here to see the company's payout ratio, plus analyst estimates of its future dividends.

Have Earnings And Dividends Been Growing?

Companies with consistently growing earnings per share generally make the best dividend stocks, as they usually find it easier to grow dividends per share. If earnings fall far enough, the company could be forced to cut its dividend. For this reason, we're glad to see Watsco's earnings per share have risen 12% per annum over the last five years.

We're a bit put out by the fact that Watsco paid out virtually all of its earnings and cashflow as dividends over the last year. Earnings are growing at a decent clip, so this payout ratio may prove sustainable, but it's not great to see.

The main way most investors will assess a company's dividend prospects is by checking the historical rate of dividend growth. In the past 10 years, Watsco has increased its dividend at approximately 14% a year on average. Both per-share earnings and dividends have both been growing rapidly in recent times, which is great to see.

The Bottom Line

Has Watsco got what it takes to maintain its dividend payments? Earnings per share have been growing, despite the company paying out a concerningly high percentage of its earnings and cashflow. We struggle to see how a company paying out so much of its earnings and cash flow will be able to sustain its dividend in a downturn, or reinvest enough into its business to continue growing earnings without borrowing heavily. It's not that we think Watsco is a bad company, but these characteristics don't generally lead to outstanding dividend performance.

Curious what other investors think of Watsco? See what analysts are forecasting, with this visualisation of its historical and future estimated earnings and cash flow .

A common investment mistake is buying the first interesting stock you see. Here you can find a list of promising dividend stocks with a greater than 2% yield and an upcoming dividend.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About NYSE:WSO

Watsco

Engages in the distribution of air conditioning, heating, and refrigeration equipment, and related parts and supplies in the United States, Canada, Latin America, and the Caribbean.

Flawless balance sheet with proven track record and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|43.0% undervalued

JO

Community Contributor

Occidental Petroleum is set to achieve a 16% profit margin improvement

Fair Value US$55.05|21.5% undervalued

DZ

Community Contributor

Argan's Revenue Set to Soar with a 13.31% Growth in the Coming Decade

Fair Value US$284.68|23.4% undervalued

KE

Community Contributor

EU#1 - From German Startup to EU’s Biggest Company

Fair Value €248.62|6.9% overvalued

TO

Community Contributor