- United States

- /

- Diversified Financial

- /

- NasdaqGS:PYPL

PayPal Holdings (NasdaqGS:PYPL) Launches Physical Card For Flexible Payments Everywhere

Reviewed by Simply Wall St

PayPal Holdings (NasdaqGS:PYPL) saw a share price increase of 5% over the past month, a performance that stood out as the market overall rose by 2% during the same timeframe. The introduction of PayPal's new physical Credit card, announced on June 3, potentially bolstered this upward momentum by expanding customer payment options. Additionally, the launch of PayPal Complete Payments in Singapore supported the company’s global expansion strategy. While the broader market trends suggest overall growth opportunities, these product launches would have added further weight to PayPal's favorable share price movements.

Find companies with promising cash flow potential yet trading below their fair value.

PayPal Holdings' recent announcements, such as the launch of a new credit card and the rollout of Complete Payments in Singapore, could significantly influence its transformation into a commerce platform as outlined in the narrative. These developments expand PayPal's customer payment options and global footprint, potentially bolstering revenue and strengthening merchant relationships. The focus on personalized consumer experiences and smart wallet services aligns with PayPal's aim to enhance revenue streams beyond traditional payment processing, which is crucial given the competitive and regulatory challenges identified in the broader analysis.

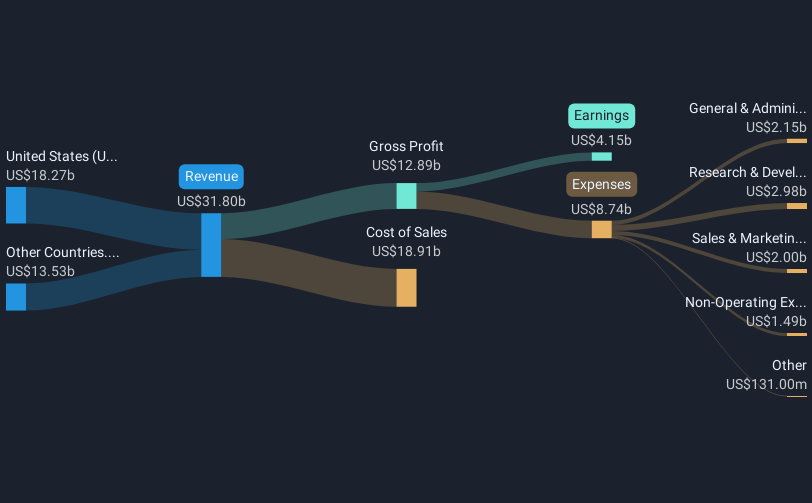

Over the past year, PayPal recorded a total return of 12%, including share price movements and dividends. This performance aligns with the general trends in the market, matching the US market's 11.9% rise but trailing the US Diversified Financial industry's 22% gain during the same period. Comparatively, PayPal's stock price remains below the consensus price target of US$82.32, indicating a 17.3% potential upside from the current price of US$68.05.

These new initiatives may influence future revenue and earnings forecasts, especially if PayPal continues to expand its transaction volume and improve margins through enhancements such as the Buy Now, Pay Later service and other value-added offerings. Analysts project revenue growth at 5.2% per year, lower than the broader market's expected growth. Earnings are forecasted to rise to US$5.5 billion by 2028, with a profit margin increase to 14.5%. As PayPal continues implementing these changes, its relevance to the overall market expectations will remain closely watched. Nonetheless, PayPal's current stock valuation offers potential opportunities for investors to consider, provided the strategic initiatives deliver the anticipated benefits.

Learn about PayPal Holdings' future growth trajectory here.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:PYPL

PayPal Holdings

Operates a technology platform that enables digital payments for merchants and consumers worldwide.

Outstanding track record and undervalued.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Airbnb Stock: Platform Growth in a World of Saturation and Scrutiny

Adobe Stock: AI-Fueled ARR Growth Pushes Guidance Higher, But Cost Pressures Loom

Thomson Reuters Stock: When Legal Intelligence Becomes Mission-Critical Infrastructure

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

The AI Infrastructure Giant Grows Into Its Valuation

Trending Discussion