Advertisement

- United States

- /

- Semiconductors

- /

- NasdaqGS:NVMI

Nova Measuring Instruments Ltd. Just Beat EPS By 43%: Here's What Analysts Think Will Happen Next

Nova Measuring Instruments Ltd. (NASDAQ:NVMI) investors will be delighted, with the company turning in some strong numbers with its latest results. It was overall a positive result, with revenues beating expectations by 7.3% to hit US$61m. Nova Measuring Instruments also reported a statutory profit of US$0.41, which was an impressive 43% above what the analysts had forecast. The analysts typically update their forecasts at each earnings report, and we can judge from their estimates whether their view of the company has changed or if there are any new concerns to be aware of. With this in mind, we've gathered the latest statutory forecasts to see what the analysts are expecting for next year.

View our latest analysis for Nova Measuring Instruments

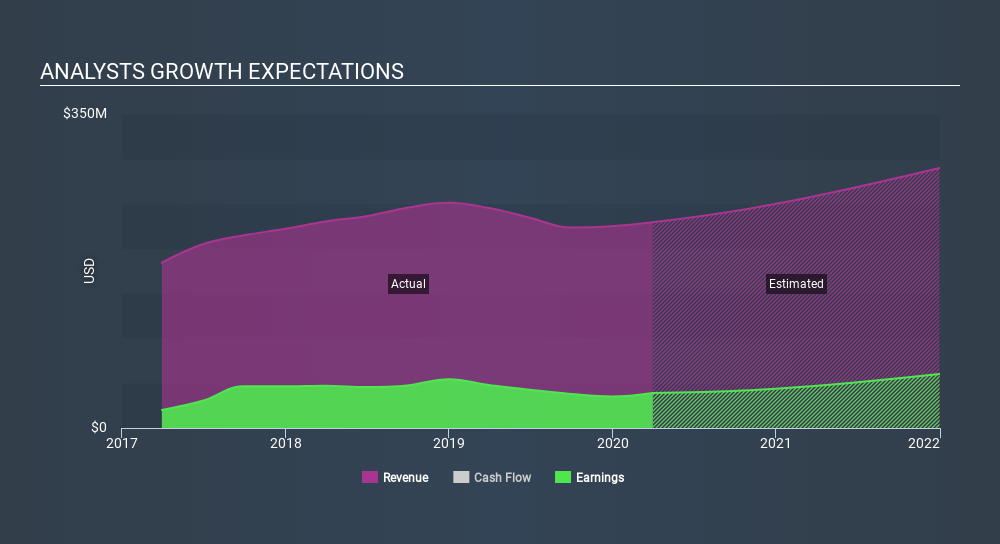

Taking into account the latest results, the current consensus from Nova Measuring Instruments' four analysts is for revenues of US$249.9m in 2020, which would reflect a solid 9.0% increase on its sales over the past 12 months. Per-share earnings are expected to accumulate 7.5% to US$1.51. Yet prior to the latest earnings, the analysts had been anticipated revenues of US$237.1m and earnings per share (EPS) of US$1.27 in 2020. So it seems there's been a definite increase in optimism about Nova Measuring Instruments' future following the latest results, with a substantial gain in the earnings per share forecasts in particular.

It will come as no surprise to learn that the analysts have increased their price target for Nova Measuring Instruments 7.7% to US$49.00 on the back of these upgrades. Fixating on a single price target can be unwise though, since the consensus target is effectively the average of analyst price targets. As a result, some investors like to look at the range of estimates to see if there are any diverging opinions on the company's valuation. The most optimistic Nova Measuring Instruments analyst has a price target of US$50.00 per share, while the most pessimistic values it at US$48.00. This is a very narrow spread of estimates, implying either that Nova Measuring Instruments is an easy company to value, or - more likely - the analysts are relying heavily on some key assumptions.

Looking at the bigger picture now, one of the ways we can make sense of these forecasts is to see how they measure up against both past performance and industry growth estimates. It's pretty clear that there is an expectation that Nova Measuring Instruments' revenue growth will slow down substantially, with revenues next year expected to grow 9.0%, compared to a historical growth rate of 14% over the past five years. Juxtapose this against the other companies in the industry with analyst coverage, which are forecast to grow their revenues (in aggregate) 9.1% next year. Factoring in the forecast slowdown in growth, it looks like Nova Measuring Instruments is forecast to grow at about the same rate as the wider industry.

The Bottom Line

The most important thing here is that the analysts upgraded their earnings per share estimates, suggesting that there has been a clear increase in optimism towards Nova Measuring Instruments following these results. They also upgraded their revenue forecasts, although the latest estimates suggest that Nova Measuring Instruments will grow in line with the overall industry. There was also a nice increase in the price target, with the analysts clearly feeling that the intrinsic value of the business is improving.

Keeping that in mind, we still think that the longer term trajectory of the business is much more important for investors to consider. At Simply Wall St, we have a full range of analyst estimates for Nova Measuring Instruments going out to 2021, and you can see them free on our platform here..

Don't forget that there may still be risks. For instance, we've identified 2 warning signs for Nova Measuring Instruments (1 shouldn't be ignored) you should be aware of.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About NasdaqGS:NVMI

Nova

Designs, develops, produces, and sells process control systems used in the manufacture of semiconductors in Israel, Taiwan, the United States, China, Korea, and internationally.

Outstanding track record with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|33.6% undervalued

JO

Community Contributor

Occidental Petroleum is set to achieve a 16% profit margin improvement

Fair Value US$55.05|18.5% undervalued

DZ

Community Contributor

Argan's Revenue Set to Soar with a 13.31% Growth in the Coming Decade

Fair Value US$284.68|21.2% undervalued

KE

Community Contributor

EU#1 - From German Startup to EU’s Biggest Company

Fair Value €248.62|5.8% overvalued

TO

Community Contributor