Advertisement

- Greece

- /

- Oil and Gas

- /

- ATSE:MOH

Need To Know: Analysts Are Much More Bullish On Motor Oil (Hellas) Corinth Refineries S.A. (ATH:MOH)

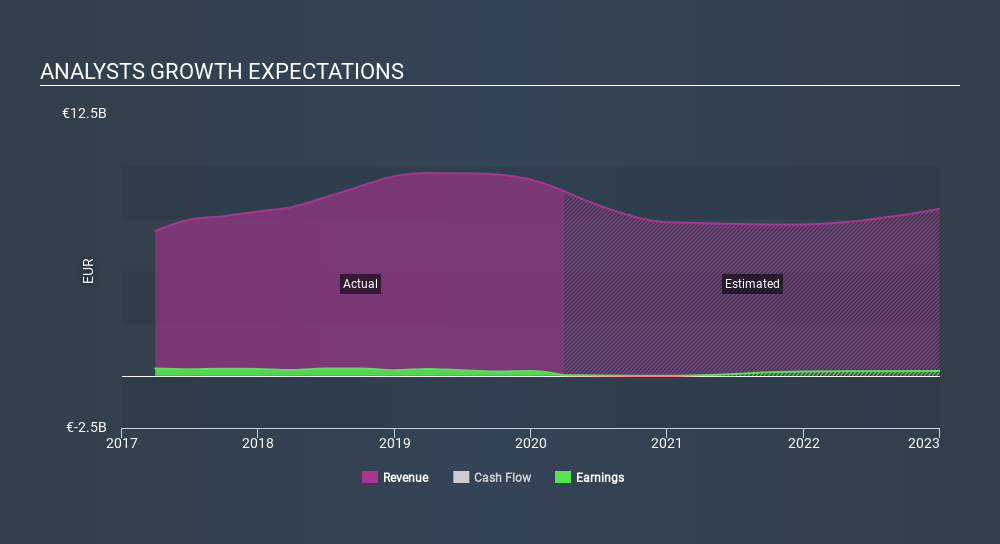

Celebrations may be in order for Motor Oil (Hellas) Corinth Refineries S.A. (ATH:MOH) shareholders, with the analysts delivering a significant upgrade to their statutory estimates for the company. Consensus estimates suggest investors could expect greatly increased statutory revenues and earnings per share, with analysts modelling a real improvement in business performance.

Following the latest upgrade, the current consensus, from the five analysts covering Motor Oil (Hellas) Corinth Refineries, is for revenues of €7.3b in 2020, which would reflect an uncomfortable 17% reduction in Motor Oil (Hellas) Corinth Refineries' sales over the past 12 months. After this upgrade, the company is anticipated to report a loss of €0.019 in 2020, a sharp decline from a profit over the last year. Yet before this consensus update, the analysts had been forecasting revenues of €6.4b and losses of €1.86 per share in 2020. So there's been quite a change-up of views after the recent consensus updates, with the analysts making a sizeable increase to their revenue forecasts while also reducing the estimated loss as the business grows towards breakeven.

Check out our latest analysis for Motor Oil (Hellas) Corinth Refineries

Despite these upgrades, the analysts have not made any major changes to their price target of €18.57, implying that their latest estimates don't have a long term impact on what they think the stock is worth. There's another way to think about price targets though, and that's to look at the range of price targets put forward by analysts, because a wide range of estimates could suggest a diverse view on possible outcomes for the business. Currently, the most bullish analyst values Motor Oil (Hellas) Corinth Refineries at €29.00 per share, while the most bearish prices it at €11.00. Note the wide gap in analyst price targets? This implies to us that there is a fairly broad range of possible scenarios for the underlying business.

Taking a look at the bigger picture now, one of the ways we can understand these forecasts is to see how they compare to both past performance and industry growth estimates. These estimates imply that sales are expected to slow, with a forecast revenue decline of 17%, a significant reduction from annual growth of 6.8% over the last five years. By contrast, our data suggests that other companies (with analyst coverage) in the same industry are forecast to see their revenue grow 11% annually for the foreseeable future. It's pretty clear that Motor Oil (Hellas) Corinth Refineries' revenues are expected to perform substantially worse than the wider industry.

The Bottom Line

The highlight for us was that the consensus reduced its estimated losses this year, perhaps suggesting Motor Oil (Hellas) Corinth Refineries is moving incrementally towards profitability. Pleasantly, analysts also upgraded their revenue estimates, and their forecasts suggest the business is expected to grow slower than the wider market. Some investors might be disappointed to see that the price target is unchanged, but we feel that improving fundamentals are usually a positive - assuming these forecasts are met! So Motor Oil (Hellas) Corinth Refineries could be a good candidate for more research.

Analysts are definitely bullish on Motor Oil (Hellas) Corinth Refineries, but no company is perfect. Indeed, you should know that there are several potential concerns to be aware of, including its declining profit margins. For more information, you can click through to our platform to learn more about this and the 3 other flags we've identified .

Another way to search for interesting companies that could be reaching an inflection point is to track whether management are buying or selling, with our free list of growing companies that insiders are buying.

Love or hate this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned. Thank you for reading.

About ATSE:MOH

Motor Oil (Hellas) Corinth Refineries

Motor Oil (Hellas) Corinth Refineries S.A.

Average dividend payer with mediocre balance sheet.

Market Insights

Advertisement

Community Narratives

Vita Life Sciences Set for a 12.72% Revenue Growth While Tackling Operational Challenges

Fair Value AU$2.42|9.1% undervalued

RO

Community Contributor

Vossloh rides a €500 billion wave to boost growth and earnings in the next decade

Fair Value €78.41|6.1% undervalued

CH

Community Contributor

Intuitive Surgical Will Transform Healthcare with 12% Revenue Growth

Fair Value US$325.55|57.3% overvalued

UN

Community Contributor