Stock Analysis

- India

- /

- Construction

- /

- NSEI:ASHOKA

Is There More Growth In Store For Ashoka Buildcon's (NSE:ASHOKA) Returns On Capital?

What are the early trends we should look for to identify a stock that could multiply in value over the long term? One common approach is to try and find a company with returns on capital employed (ROCE) that are increasing, in conjunction with a growing amount of capital employed. Basically this means that a company has profitable initiatives that it can continue to reinvest in, which is a trait of a compounding machine. So on that note, Ashoka Buildcon (NSE:ASHOKA) looks quite promising in regards to its trends of return on capital.

Return On Capital Employed (ROCE): What is it?

For those who don't know, ROCE is a measure of a company's yearly pre-tax profit (its return), relative to the capital employed in the business. To calculate this metric for Ashoka Buildcon, this is the formula:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.13 = ₹12b ÷ (₹136b - ₹44b) (Based on the trailing twelve months to June 2020).

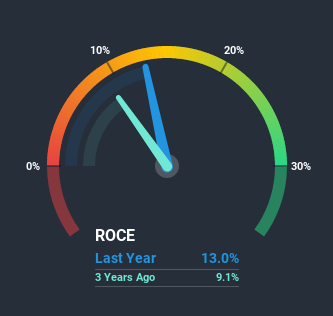

So, Ashoka Buildcon has an ROCE of 13%. On its own, that's a standard return, however it's much better than the 8.6% generated by the Construction industry.

View our latest analysis for Ashoka Buildcon

Above you can see how the current ROCE for Ashoka Buildcon compares to its prior returns on capital, but there's only so much you can tell from the past. If you'd like to see what analysts are forecasting going forward, you should check out our free report for Ashoka Buildcon.

The Trend Of ROCE

Ashoka Buildcon has not disappointed in regards to ROCE growth. The figures show that over the last five years, returns on capital have grown by 345%. That's not bad because this tells for every dollar invested (capital employed), the company is increasing the amount earned from that dollar. Interestingly, the business may be becoming more efficient because it's applying 31% less capital than it was five years ago. A business that's shrinking its asset base like this isn't usually typical of a soon to be multi-bagger company.

On a side note, we noticed that the improvement in ROCE appears to be partly fueled by an increase in current liabilities. The current liabilities has increased to 33% of total assets, so the business is now more funded by the likes of its suppliers or short-term creditors. Keep an eye out for future increases because when the ratio of current liabilities to total assets gets particularly high, this can introduce some new risks for the business.In Conclusion...

In a nutshell, we're pleased to see that Ashoka Buildcon has been able to generate higher returns from less capital. Astute investors may have an opportunity here because the stock has declined 43% in the last five years. So researching this company further and determining whether or not these trends will continue seems justified.

If you want to know some of the risks facing Ashoka Buildcon we've found 3 warning signs (2 are significant!) that you should be aware of before investing here.

For those who like to invest in solid companies, check out this free list of companies with solid balance sheets and high returns on equity.

If you’re looking to trade Ashoka Buildcon, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're helping make it simple.

Find out whether Ashoka Buildcon is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About NSEI:ASHOKA

Ashoka Buildcon

Engages in the infrastructure development business in India.

Proven track record and fair value.