Advertisement

- Canada

- /

- Construction

- /

- TSX:BDT

Is It Time To Consider Buying Bird Construction Inc. (TSE:BDT)?

Bird Construction Inc. (TSE:BDT), which is in the construction business, and is based in Canada, received a lot of attention from a substantial price increase on the TSX over the last few months. With many analysts covering the stock, we may expect any price-sensitive announcements have already been factored into the stock’s share price. However, could the stock still be trading at a relatively cheap price? Let’s examine Bird Construction’s valuation and outlook in more detail to determine if there’s still a bargain opportunity.

See our latest analysis for Bird Construction

What is Bird Construction worth?

Bird Construction appears to be overvalued according to my relative valuation model. I’ve used the price-to-earnings ratio in this instance because there’s not enough visibility to forecast its cash flows. The stock’s ratio of 36.11x is currently well-above the industry average of 17.1x, meaning that it is trading at a more expensive price relative to its peers. But, is there another opportunity to buy low in the future? Given that Bird Construction’s share is fairly volatile (i.e. its price movements are magnified relative to the rest of the market) this could mean the price can sink lower, giving us another chance to buy in the future. This is based on its high beta, which is a good indicator for share price volatility.

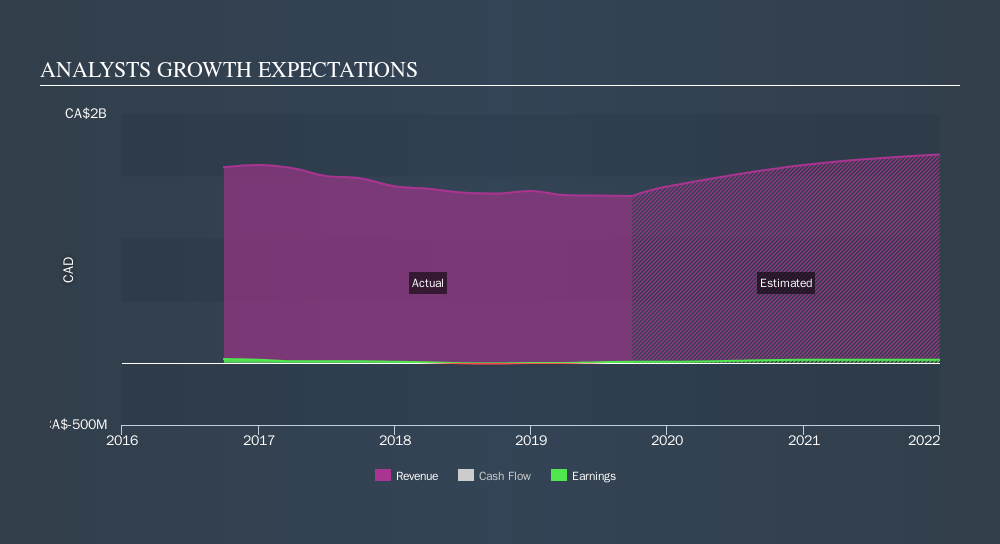

What kind of growth will Bird Construction generate?

Investors looking for growth in their portfolio may want to consider the prospects of a company before buying its shares. Although value investors would argue that it’s the intrinsic value relative to the price that matter the most, a more compelling investment thesis would be high growth potential at a cheap price. Bird Construction’s earnings over the next few years are expected to double, indicating a very optimistic future ahead. This should lead to stronger cash flows, feeding into a higher share value.

What this means for you:

Are you a shareholder? BDT’s optimistic future growth appears to have been factored into the current share price, with shares trading above its fair value. At this current price, shareholders may be asking a different question – should I sell? If you believe BDT should trade below its current price, selling high and buying it back up again when its price falls towards its real value can be profitable. But before you make this decision, take a look at whether its fundamentals have changed.

Are you a potential investor? If you’ve been keeping an eye on BDT for a while, now may not be the best time to enter into the stock. The price has surpassed its industry peers, which means it is likely that there is no more upside from mispricing. However, the optimistic prospect is encouraging for BDT, which means it’s worth diving deeper into other factors in order to take advantage of the next price drop.

Price is just the tip of the iceberg. Dig deeper into what truly matters – the fundamentals – before you make a decision on Bird Construction. You can find everything you need to know about Bird Construction in the latest infographic research report. If you are no longer interested in Bird Construction, you can use our free platform to see my list of over 50 other stocks with a high growth potential.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About TSX:BDT

Bird Construction

Provides construction services in Canada.

Reasonable growth potential with adequate balance sheet.

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Eva Live ·

This small cap is building the AI workforce of the future

Fair Value:US$7.4352.0% undervalued

75 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

TR

tripledub on lululemon athletica ·

Lululemon Got Boring Right About the Time It Got Cheap. That's Usually the Point

Fair Value:US$22042.4% undervalued

25 followersusers have followed this narrative

6 commentsusers have commented on this narrative

26 likesusers have liked this narrative

WO

woodworthfund on Kraft Heinz ·

Kraft Heinz (KHC): Less Drama, More Ketchup

Fair Value:US$3532.7% undervalued

8 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

CA

Canderous on PetroTal ·

Beyond 2026, Beyond a Double

Fair Value:CA$1.8168.5% undervalued

27 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

Recently Updated Narratives

DE

DeathSmiIes on New Horizon Aircraft ·

HORIZON AIRCRAFT (HOVR) Institutional Investor Package August 1, 2025 — Confidential Review Draft

Fair Value:US$2087.6% undervalued

5 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

CO

Coward_Nutlick on Elicio Therapeutics ·

Very Bullish

Fair Value:US$10090.1% undervalued

20 followersusers have followed this narrative

3 commentsusers have commented on this narrative

2 likesusers have liked this narrative

KA

kapirey on KKR ·

Incluso con un colapso brutal del crédito KKR mantendría beneficios relevantes

Fair Value:US$84.4512.2% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8590.1% undervalued

114 followersusers have followed this narrative

2 commentsusers have commented on this narrative

31 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$268.6118.3% undervalued

1193 followersusers have followed this narrative

7 commentsusers have commented on this narrative

34 likesusers have liked this narrative

TR

tripledub on lululemon athletica ·

Lululemon Got Boring Right About the Time It Got Cheap. That's Usually the Point

Fair Value:US$22042.4% undervalued

25 followersusers have followed this narrative

6 commentsusers have commented on this narrative

26 likesusers have liked this narrative