Advertisement

- Brazil

- /

- Healthcare Services

- /

- BOVESPA:AALR3

Is Centro de Imagem Diagnósticos (BVMF:AALR3) Likely To Turn Things Around?

There are a few key trends to look for if we want to identify the next multi-bagger. Ideally, a business will show two trends; firstly a growing return on capital employed (ROCE) and secondly, an increasing amount of capital employed. Basically this means that a company has profitable initiatives that it can continue to reinvest in, which is a trait of a compounding machine. However, after briefly looking over the numbers, we don't think Centro de Imagem Diagnósticos (BVMF:AALR3) has the makings of a multi-bagger going forward, but let's have a look at why that may be.

Understanding Return On Capital Employed (ROCE)

For those who don't know, ROCE is a measure of a company's yearly pre-tax profit (its return), relative to the capital employed in the business. Analysts use this formula to calculate it for Centro de Imagem Diagnósticos:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.044 = R$88m ÷ (R$2.6b - R$634m) (Based on the trailing twelve months to March 2020).

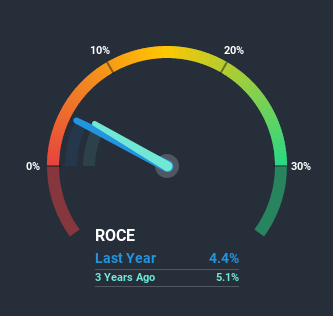

Thus, Centro de Imagem Diagnósticos has an ROCE of 4.4%. Ultimately, that's a low return and it under-performs the Healthcare industry average of 13%.

See our latest analysis for Centro de Imagem Diagnósticos

Above you can the how the current ROCE for Centro de Imagem Diagnósticos' compares to it's prior returns on capital, but you can only tell so much from the past. If you'd like to see what analysts are forecasting going forward, you should check out our free report for Centro de Imagem Diagnósticos.

How Are Returns Trending?

The returns on capital haven't changed much for Centro de Imagem Diagnósticos in recent years. The company has employed 54% more capital in the last five years, and the returns on that capital have remained stable at 4.4%. This poor ROCE doesn't inspire confidence right now, and with the increase in capital employed, it's evident that the business isn't deploying the funds into high return investments.

On another note, while the change in ROCE trend might not scream for attention, it's interesting that the current liabilities have actually gone up over the last five years. This is intriguing because if current liabilities hadn't increased to 24% of total assets, this reported ROCE would probably be less than4.4% because total capital employed would be higher.The 4.4% ROCE could be even lower if current liabilities weren't 24% of total assets, because the the formula would show a larger base of total capital employed. So while current liabilities isn't high right now, keep an eye out in case it increases further, because this can introduce some elements of risk.The Bottom Line On Centro de Imagem Diagnósticos' ROCE

Long story short, while Centro de Imagem Diagnósticos has been reinvesting its capital, the returns that it's generating haven't increased. And in the last three years, the stock has given away 40% so the market doesn't look too hopeful on these trends strengthening any time soon. On the whole, we aren't too inspired by the underlying trends and we think there may be better chances of finding a multi-bagger elsewhere.

On a final note, we found 3 warning signs for Centro de Imagem Diagnósticos (1 can't be ignored) you should be aware of.

While Centro de Imagem Diagnósticos isn't earning the highest return, check out this free list of companies that are earning high returns on equity with solid balance sheets.

If you’re looking to trade Centro de Imagem Diagnósticos, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account.Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About BOVESPA:AALR3

Alliança Saúde e Participações

Provides diagnostic imaging and medicine services in Brazil.

Excellent balance sheet with slight risk.

Market Insights

Advertisement

Weekly Picks

ST

stuart_roberts on Upside Gold ·

An Undervalued 3.3Moz Gold Project in Canada

Fair Value:CA$5.0768.0% undervalued

285 followersusers have followed this narrative

1 commentusers have commented on this narrative

42 likesusers have liked this narrative

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8591.3% undervalued

95 followersusers have followed this narrative

2 commentsusers have commented on this narrative

26 likesusers have liked this narrative

TO

Tokyo on Anheuser-Busch InBev ·

EU#8 - Anheuser-Busch InBev: Courage, Capital, and the Discipline to Build an Empire

Fair Value:€89.4524.2% undervalued

8 followersusers have followed this narrative

3 commentsusers have commented on this narrative

3 likesusers have liked this narrative

OS

oscargarcia on Amazon.com ·

The capitalist colossus that makes your parcels magically appear, powers half the internet, and knows your shopping habits.

Fair Value:US$2803.2% undervalued

62 followersusers have followed this narrative

1 commentusers have commented on this narrative

2 likesusers have liked this narrative

Recently Updated Narratives

ES

Esteban on Verisk Analytics ·

VRSK 05-2026

Fair Value:US$69.7150.6% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

ZT

ZThunderBRL on iShares - iShares MSCI Brazil ETF ·

Long earnings, cautious on multiple

Fair Value:US$1.622.3k% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1932.5% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8591.3% undervalued

95 followersusers have followed this narrative

2 commentsusers have commented on this narrative

26 likesusers have liked this narrative

KI

Kingman1152 on NVIDIA ·

NVIDIA will see a profit margin surge of 55% in the next 5 years

Fair Value:US$305.230.7% undervalued

68 followersusers have followed this narrative

2 commentsusers have commented on this narrative

24 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$561.9325.1% undervalued

1398 followersusers have followed this narrative

2 commentsusers have commented on this narrative

12 likesusers have liked this narrative