Stock Analysis

ICICI Lombard General Insurance Company Limited Just Missed Earnings And Its Revenue Numbers Were Weaker Than Expected

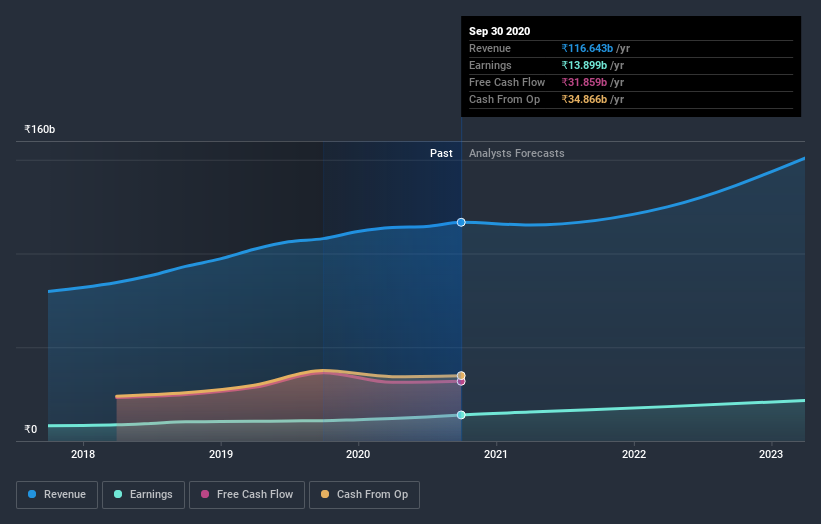

As you might know, ICICI Lombard General Insurance Company Limited (NSE:ICICIGI) recently reported its quarterly numbers. Revenues were ₹29b, 14% below analyst expectations, although losses didn't appear to worsen significantly, with a per-share statutory loss of ₹26.19 being in line with what the analysts forecast. Following the result, the analysts have updated their earnings model, and it would be good to know whether they think there's been a strong change in the company's prospects, or if it's business as usual. So we gathered the latest post-earnings forecasts to see what estimates suggest is in store for next year.

Check out our latest analysis for ICICI Lombard General Insurance

Taking into account the latest results, ICICI Lombard General Insurance's 14 analysts currently expect revenues in 2021 to be ₹115.2b, approximately in line with the last 12 months. Per-share earnings are expected to ascend 11% to ₹33.89. Before this earnings report, the analysts had been forecasting revenues of ₹110.8b and earnings per share (EPS) of ₹32.04 in 2021. So there seems to have been a moderate uplift in sentiment following the latest results, given the upgrades to both revenue and earnings per share forecasts for next year.

Despite these upgrades,the analysts have not made any major changes to their price target of ₹1,393, suggesting that the higher estimates are not likely to have a long term impact on what the stock is worth. The consensus price target is just an average of individual analyst targets, so - it could be handy to see how wide the range of underlying estimates is. The most optimistic ICICI Lombard General Insurance analyst has a price target of ₹1,619 per share, while the most pessimistic values it at ₹895. This shows there is still a bit of diversity in estimates, but analysts don't appear to be totally split on the stock as though it might be a success or failure situation.

Of course, another way to look at these forecasts is to place them into context against the industry itself. We would highlight that sales are expected to reverse, with the forecast 1.2% revenue decline a notable change from historical growth of 15% over the last five years. By contrast, our data suggests that other companies (with analyst coverage) in the same industry are forecast to see their revenue grow 5.7% annually for the foreseeable future. It's pretty clear that ICICI Lombard General Insurance's revenues are expected to perform substantially worse than the wider industry.

The Bottom Line

The most important thing here is that the analysts upgraded their earnings per share estimates, suggesting that there has been a clear increase in optimism towards ICICI Lombard General Insurance following these results. Fortunately, they also upgraded their revenue estimates, although our data indicates sales are expected to perform worse than the wider industry. The consensus price target held steady at ₹1,393, with the latest estimates not enough to have an impact on their price targets.

With that in mind, we wouldn't be too quick to come to a conclusion on ICICI Lombard General Insurance. Long-term earnings power is much more important than next year's profits. We have estimates - from multiple ICICI Lombard General Insurance analysts - going out to 2023, and you can see them free on our platform here.

You still need to take note of risks, for example - ICICI Lombard General Insurance has 1 warning sign we think you should be aware of.

If you decide to trade ICICI Lombard General Insurance, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Valuation is complex, but we're helping make it simple.

Find out whether ICICI Lombard General Insurance is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About NSEI:ICICIGI

ICICI Lombard General Insurance

Provides various general insurance products and services in India.

Excellent balance sheet with proven track record.