Advertisement

- Singapore

- /

- Consumer Services

- /

- SGX:NR7

Here's What Raffles Education Corporation Limited's (SGX:NR7) P/E Ratio Is Telling Us

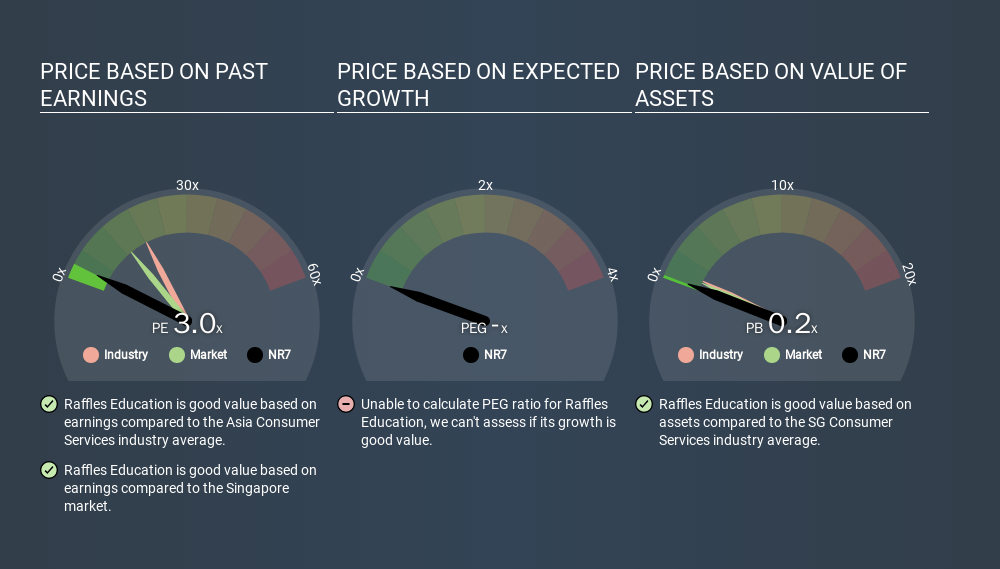

Today, we'll introduce the concept of the P/E ratio for those who are learning about investing. To keep it practical, we'll show how Raffles Education Corporation Limited's (SGX:NR7) P/E ratio could help you assess the value on offer. Raffles Education has a price to earnings ratio of 2.99, based on the last twelve months. In other words, at today's prices, investors are paying SGD2.99 for every SGD1 in prior year profit.

Check out our latest analysis for Raffles Education

How Do You Calculate A P/E Ratio?

The formula for P/E is:

Price to Earnings Ratio = Share Price ÷ Earnings per Share (EPS)

Or for Raffles Education:

P/E of 2.99 = SGD0.09 ÷ SGD0.03 (Based on the year to September 2019.)

Is A High Price-to-Earnings Ratio Good?

The higher the P/E ratio, the higher the price tag of a business, relative to its trailing earnings. That isn't a good or a bad thing on its own, but a high P/E means that buyers have a higher opinion of the business's prospects, relative to stocks with a lower P/E.

Does Raffles Education Have A Relatively High Or Low P/E For Its Industry?

One good way to get a quick read on what market participants expect of a company is to look at its P/E ratio. If you look at the image below, you can see Raffles Education has a lower P/E than the average (18.3) in the consumer services industry classification.

Its relatively low P/E ratio indicates that Raffles Education shareholders think it will struggle to do as well as other companies in its industry classification. Many investors like to buy stocks when the market is pessimistic about their prospects. It is arguably worth checking if insiders are buying shares, because that might imply they believe the stock is undervalued.

How Growth Rates Impact P/E Ratios

P/E ratios primarily reflect market expectations around earnings growth rates. When earnings grow, the 'E' increases, over time. Therefore, even if you pay a high multiple of earnings now, that multiple will become lower in the future. Then, a lower P/E should attract more buyers, pushing the share price up.

In the last year, Raffles Education grew EPS like Taylor Swift grew her fan base back in 2010; the 147% gain was both fast and well deserved. Even better, EPS is up 30% per year over three years. So you might say it really deserves to have an above-average P/E ratio. Regrettably, the longer term performance is poor, with EPS down 12% per year over 5 years.

A Limitation: P/E Ratios Ignore Debt and Cash In The Bank

The 'Price' in P/E reflects the market capitalization of the company. So it won't reflect the advantage of cash, or disadvantage of debt. The exact same company would hypothetically deserve a higher P/E ratio if it had a strong balance sheet, than if it had a weak one with lots of debt, because a cashed up company can spend on growth.

Such spending might be good or bad, overall, but the key point here is that you need to look at debt to understand the P/E ratio in context.

Is Debt Impacting Raffles Education's P/E?

Raffles Education's net debt is considerable, at 251% of its market cap. This is a relatively high level of debt, so the stock probably deserves a relatively low P/E ratio. Keep that in mind when comparing it to other companies.

The Verdict On Raffles Education's P/E Ratio

Raffles Education trades on a P/E ratio of 3.0, which is below the SG market average of 13.3. While the EPS growth last year was strong, the significant debt levels reduce the number of options available to management. If the company can continue to grow earnings, then the current P/E may be unjustifiably low.

When the market is wrong about a stock, it gives savvy investors an opportunity. If the reality for a company is not as bad as the P/E ratio indicates, then the share price should increase as the market realizes this. We don't have analyst forecasts, but you might want to assess this data-rich visualization of earnings, revenue and cash flow.

Of course you might be able to find a better stock than Raffles Education. So you may wish to see this free collection of other companies that have grown earnings strongly.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About SGX:NR7

Raffles Education

An investment holding company, provides education and related services in the regions of ASEAN, North Asia, South Asia, Australasia, and Europe.

Slightly overvalued with imperfect balance sheet.

Market Insights

Advertisement

Community Narratives

Vita Life Sciences Set for a 12.72% Revenue Growth While Tackling Operational Challenges

Fair Value AU$2.42|9.5% undervalued

RO

Community Contributor

Vossloh rides a €500 billion wave to boost growth and earnings in the next decade

Fair Value €78.41|7.2% undervalued

CH

Community Contributor

Intuitive Surgical Will Transform Healthcare with 12% Revenue Growth

Fair Value US$325.55|56.5% overvalued

UN

Community Contributor