Advertisement

- United States

- /

- Chemicals

- /

- NYSEAM:FSI

Flexible Solutions International Inc.'s (NYSEMKT:FSI) Analyst Just Slashed Next Year's Estimates

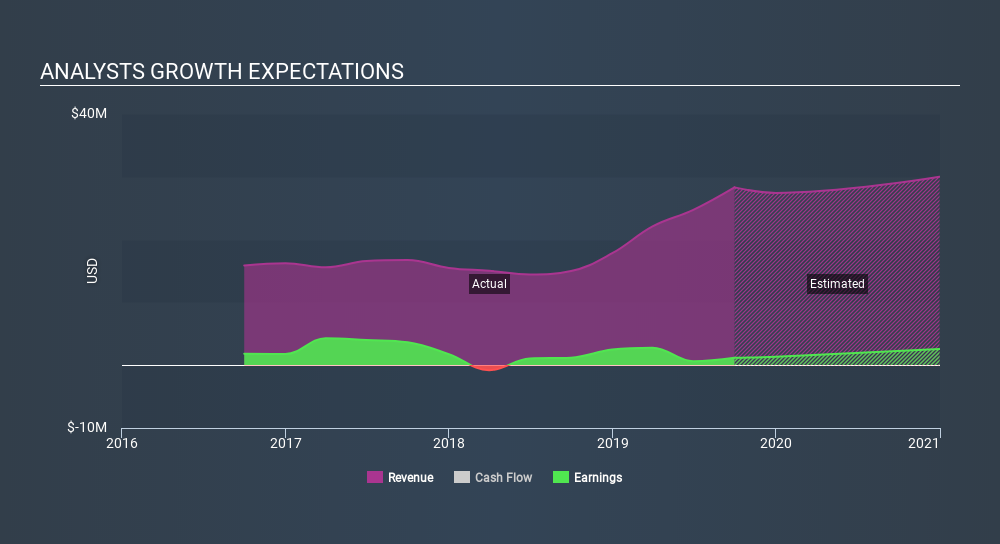

Today is shaping up negative for Flexible Solutions International Inc. (NYSEMKT:FSI) shareholders, with the covering analyst delivering a substantial negative revision to next year's forecasts. Both revenue and earnings per share (EPS) forecasts went under the knife, suggesting the analyst has soured majorly on the business.

After the downgrade, the solitary analyst covering Flexible Solutions International is now predicting revenues of US$30m in 2020. If met, this would reflect a modest 6.0% improvement in sales compared to the last 12 months. Statutory earnings per share are presumed to leap 98% to US$0.20. Previously, the analyst had been modelling revenues of US$34m and earnings per share (EPS) of US$0.27 in 2020. It looks like analyst sentiment has declined substantially, with a substantial drop in revenue estimates and a large cut to earnings per share numbers as well.

View our latest analysis for Flexible Solutions International

It'll come as no surprise then, to learn that the analyst has cut their price target 23% to US$2.50.

Another way we can view these estimates is in the context of the bigger picture, such as how the forecasts stack up against past performance, and whether forecasts are more or less bullish relative to other companies in the industry. We can infer from the latest estimates that forecasts expect a continuation of Flexible Solutions International's historical trends, as next year's 6.0% revenue growth is roughly in line with 7.2% annual revenue growth over the past five years. Compare this with the wider industry, which analyst estimates (in aggregate) suggest will see revenues grow 3.6% next year. So it's pretty clear that Flexible Solutions International is forecast to grow substantially faster than its industry.

The Bottom Line

The biggest issue in the new estimates is that the analyst has reduced their earnings per share estimates, suggesting business headwinds lay ahead for Flexible Solutions International. While the analyst did downgrade their revenue estimates, these forecasts still imply revenues will perform better than the wider market. After such a stark change in sentiment from the analyst, we'd understand if readers now felt a bit wary of Flexible Solutions International.

Even so, the longer term trajectory of the business is much more important for the value creation of shareholders. At least one analyst has provided forecasts out to 2020, which can be seen for free on our platform here.

Of course, seeing company management invest large sums of money in a stock can be just as useful as knowing whether analysts are downgrading their estimates. So you may also wish to search this free list of stocks that insiders are buying.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About NYSEAM:FSI

Flexible Solutions International

Develops, manufactures, and markets specialty chemicals that slow the evaporation of water in Canada, the United States, and internationally.

Flawless balance sheet with high growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

Vita Life Sciences Set for a 12.72% Revenue Growth While Tackling Operational Challenges

Fair Value AU$2.42|9.5% undervalued

RO

Community Contributor

Vossloh rides a €500 billion wave to boost growth and earnings in the next decade

Fair Value €78.41|6.1% undervalued

CH

Community Contributor

Intuitive Surgical Will Transform Healthcare with 12% Revenue Growth

Fair Value US$325.55|56.5% overvalued

UN

Community Contributor