Advertisement

- United States

- /

- Machinery

- /

- NYSE:JBTM

Earnings Beat: John Bean Technologies Corporation Just Beat Analyst Forecasts, And Analysts Have Been Updating Their Models

A week ago, John Bean Technologies Corporation (NYSE:JBT) came out with a strong set of quarterly numbers that could potentially lead to a re-rate of the stock. The company beat both earnings and revenue forecasts, with revenue of US$458m, some 6.1% above estimates, and statutory earnings per share (EPS) coming in at US$0.90, 26% ahead of expectations. Following the result, the analysts have updated their earnings model, and it would be good to know whether they think there's been a strong change in the company's prospects, or if it's business as usual. So we gathered the latest post-earnings forecasts to see what estimates suggest is in store for next year.

Check out our latest analysis for John Bean Technologies

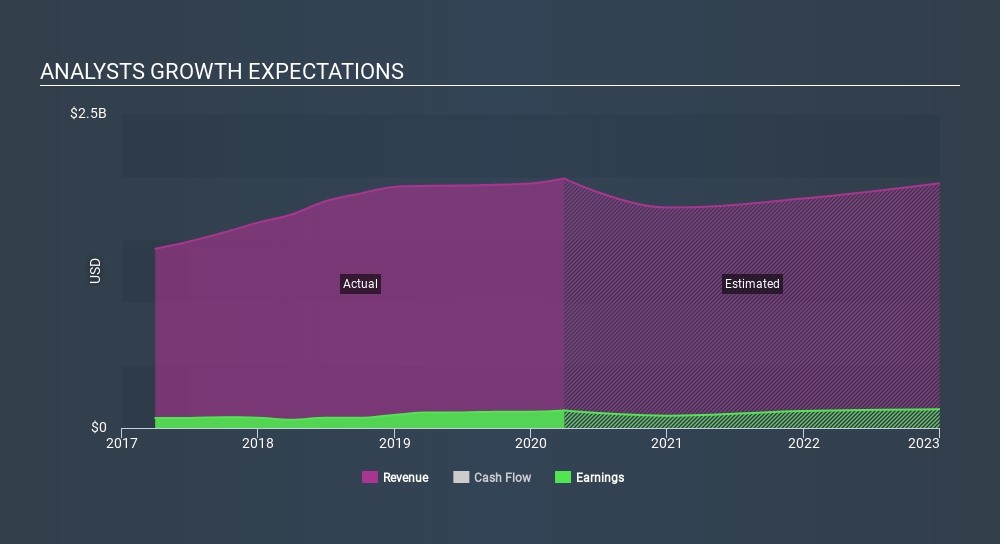

After the latest results, the consensus from John Bean Technologies' eight analysts is for revenues of US$1.76b in 2020, which would reflect a chunky 12% decline in sales compared to the last year of performance. Statutory earnings per share are forecast to dive 25% to US$3.27 in the same period. Before this earnings report, the analysts had been forecasting revenues of US$1.77b and earnings per share (EPS) of US$3.75 in 2020. So there's definitely been a decline in sentiment after the latest results, noting the real cut to new EPS forecasts.

It might be a surprise to learn that the consensus price target was broadly unchanged at US$84.13, with the analysts clearly implying that the forecast decline in earnings is not expected to have much of an impact on valuation. The consensus price target is just an average of individual analyst targets, so - it could be handy to see how wide the range of underlying estimates is. Currently, the most bullish analyst values John Bean Technologies at US$100.00 per share, while the most bearish prices it at US$64.00. There are definitely some different views on the stock, but the range of estimates is not wide enough as to imply that the situation is unforecastable, in our view.

Of course, another way to look at these forecasts is to place them into context against the industry itself. We would highlight that sales are expected to reverse, with the forecast 12% revenue decline a notable change from historical growth of 15% over the last five years. By contrast, our data suggests that other companies (with analyst coverage) in the same industry are forecast to see their revenue grow 3.8% annually for the foreseeable future. It's pretty clear that John Bean Technologies' revenues are expected to perform substantially worse than the wider industry.

The Bottom Line

The biggest concern is that the analysts reduced their earnings per share estimates, suggesting business headwinds could lay ahead for John Bean Technologies. Fortunately, the analysts also reconfirmed their revenue estimates, suggesting sales are tracking in line with expectations - although our data does suggest that John Bean Technologies' revenues are expected to perform worse than the wider industry. The consensus price target held steady at US$84.13, with the latest estimates not enough to have an impact on their price targets.

With that in mind, we wouldn't be too quick to come to a conclusion on John Bean Technologies. Long-term earnings power is much more important than next year's profits. We have estimates - from multiple John Bean Technologies analysts - going out to 2022, and you can see them free on our platform here.

You still need to take note of risks, for example - John Bean Technologies has 2 warning signs (and 1 which shouldn't be ignored) we think you should know about.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About NYSE:JBTM

JBT Marel

Provides technology solutions to food and beverage industry in North America, Europe, the Middle East, Africa, the Asia Pacific, and Central and South America.

High growth potential and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

Vita Life Sciences Set for a 12.72% Revenue Growth While Tackling Operational Challenges

Fair Value AU$2.42|12.0% undervalued

RO

Community Contributor

Vossloh rides a €500 billion wave to boost growth and earnings in the next decade

Fair Value €78.41|4.0% undervalued

CH

Community Contributor

Intuitive Surgical Will Transform Healthcare with 12% Revenue Growth

Fair Value US$325.55|59.4% overvalued

UN

Community Contributor