Advertisement

- Japan

- /

- Metals and Mining

- /

- TSE:9964

Does Itec Corporation's (TYO:9964) P/E Ratio Signal A Buying Opportunity?

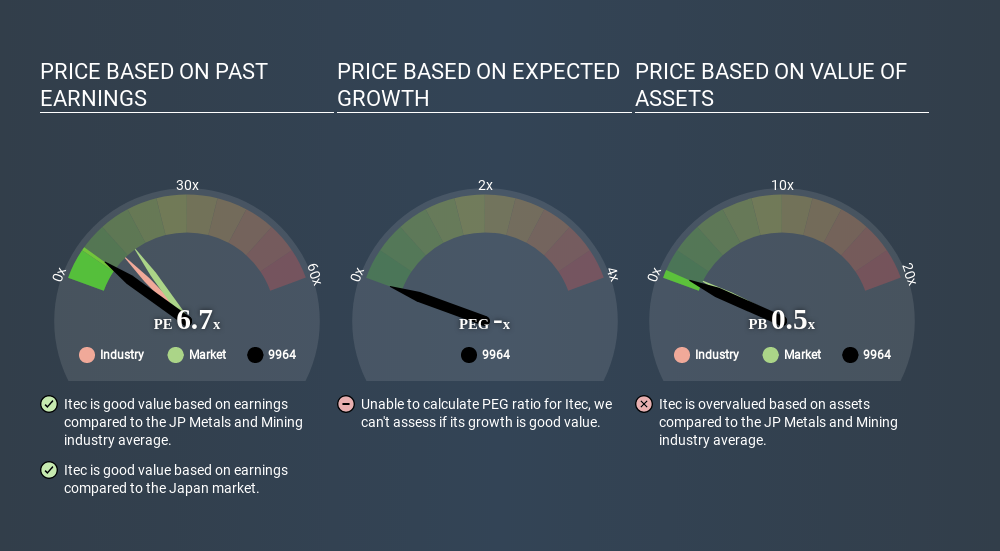

This article is written for those who want to get better at using price to earnings ratios (P/E ratios). We'll show how you can use Itec Corporation's (TYO:9964) P/E ratio to inform your assessment of the investment opportunity. Itec has a P/E ratio of 6.61, based on the last twelve months. That means that at current prices, buyers pay ¥6.61 for every ¥1 in trailing yearly profits.

View our latest analysis for Itec

How Do I Calculate Itec's Price To Earnings Ratio?

The formula for price to earnings is:

Price to Earnings Ratio = Price per Share ÷ Earnings per Share (EPS)

Or for Itec:

P/E of 6.61 = ¥1643.000 ÷ ¥248.563 (Based on the trailing twelve months to March 2020.)

(Note: the above calculation results may not be precise due to rounding.)

Is A High Price-to-Earnings Ratio Good?

A higher P/E ratio implies that investors pay a higher price for the earning power of the business. All else being equal, it's better to pay a low price -- but as Warren Buffett said, 'It's far better to buy a wonderful company at a fair price than a fair company at a wonderful price'.

Does Itec Have A Relatively High Or Low P/E For Its Industry?

One good way to get a quick read on what market participants expect of a company is to look at its P/E ratio. The image below shows that Itec has a lower P/E than the average (11.5) P/E for companies in the metals and mining industry.

This suggests that market participants think Itec will underperform other companies in its industry. While current expectations are low, the stock could be undervalued if the situation is better than the market assumes. You should delve deeper. I like to check if company insiders have been buying or selling.

How Growth Rates Impact P/E Ratios

When earnings fall, the 'E' decreases, over time. Therefore, even if you pay a low multiple of earnings now, that multiple will become higher in the future. Then, a higher P/E might scare off shareholders, pushing the share price down.

Itec's earnings per share fell by 29% in the last twelve months. But it has grown its earnings per share by 15% per year over the last five years. And over the longer term (3 years) earnings per share have decreased 5.0% annually. This could justify a low P/E.

A Limitation: P/E Ratios Ignore Debt and Cash In The Bank

One drawback of using a P/E ratio is that it considers market capitalization, but not the balance sheet. Thus, the metric does not reflect cash or debt held by the company. The exact same company would hypothetically deserve a higher P/E ratio if it had a strong balance sheet, than if it had a weak one with lots of debt, because a cashed up company can spend on growth.

Such expenditure might be good or bad, in the long term, but the point here is that the balance sheet is not reflected by this ratio.

How Does Itec's Debt Impact Its P/E Ratio?

Net debt totals 52% of Itec's market cap. This is enough debt that you'd have to make some adjustments before using the P/E ratio to compare it to a company with net cash.

The Verdict On Itec's P/E Ratio

Itec trades on a P/E ratio of 6.6, which is below the JP market average of 15.1. When you consider that the company has significant debt, and didn't grow EPS last year, it isn't surprising that the market has muted expectations.

Investors have an opportunity when market expectations about a stock are wrong. If it is underestimating a company, investors can make money by buying and holding the shares until the market corrects itself. We don't have analyst forecasts, but shareholders might want to examine this detailed historical graph of earnings, revenue and cash flow.

Of course, you might find a fantastic investment by looking at a few good candidates. So take a peek at this free list of companies with modest (or no) debt, trading on a P/E below 20.

Love or hate this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned. Thank you for reading.

About TSE:9964

Itec

Itec Corporation processes, manufactures, and trades in steel products in Japan.

Slight with mediocre balance sheet.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|6.2% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.0% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.7% overvalued

LI

Community Contributor