Advertisement

- United States

- /

- Retail Distributors

- /

- NYSE:GPC

Does Genuine Parts (NYSE:GPC) Have A Healthy Balance Sheet?

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We can see that Genuine Parts Company (NYSE:GPC) does use debt in its business. But the real question is whether this debt is making the company risky.

Why Does Debt Bring Risk?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. When we think about a company's use of debt, we first look at cash and debt together.

Check out our latest analysis for Genuine Parts

What Is Genuine Parts's Debt?

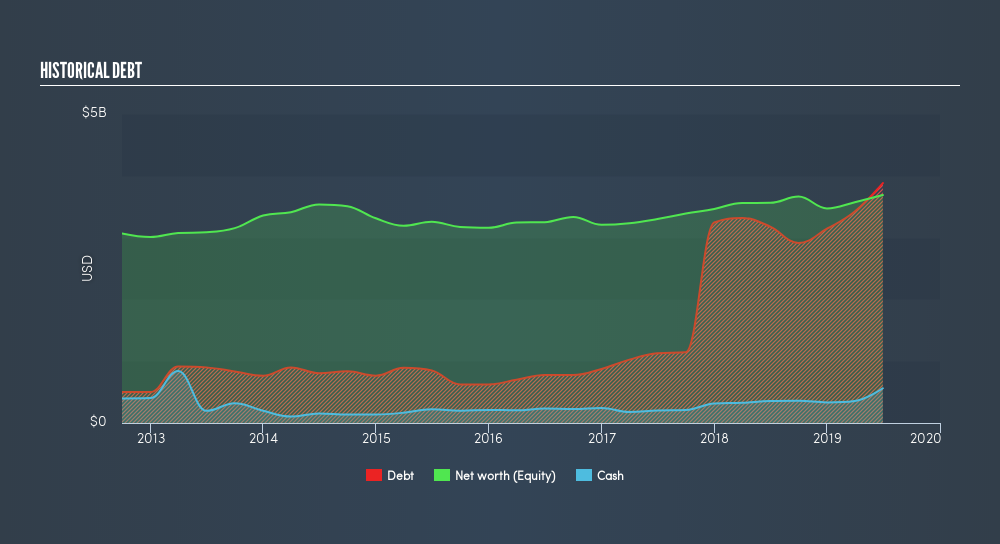

You can click the graphic below for the historical numbers, but it shows that as of June 2019 Genuine Parts had US$3.88b of debt, an increase on US$3.18b, over one year. However, it also had US$562.6m in cash, and so its net debt is US$3.32b.

A Look At Genuine Parts's Liabilities

According to the last reported balance sheet, Genuine Parts had liabilities of US$6.50b due within 12 months, and liabilities of US$4.45b due beyond 12 months. Offsetting these obligations, it had cash of US$562.6m as well as receivables valued at US$2.84b due within 12 months. So it has liabilities totalling US$7.55b more than its cash and near-term receivables, combined.

While this might seem like a lot, it is not so bad since Genuine Parts has a huge market capitalization of US$14.4b, and so it could probably strengthen its balance sheet by raising capital if it needed to. But it's clear that we should definitely closely examine whether it can manage its debt without dilution.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

We'd say that Genuine Parts's moderate net debt to EBITDA ratio ( being 2.3), indicates prudence when it comes to debt. And its commanding EBIT of 13.2 times its interest expense, implies the debt load is as light as a peacock feather. Genuine Parts grew its EBIT by 7.5% in the last year. Whilst that hardly knocks our socks off it is a positive when it comes to debt. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Genuine Parts's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So we always check how much of that EBIT is translated into free cash flow. Over the most recent three years, Genuine Parts recorded free cash flow worth 63% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This cold hard cash means it can reduce its debt when it wants to.

Our View

When it comes to the balance sheet, the standout positive for Genuine Parts was the fact that it seems able to cover its interest expense with its EBIT confidently. However, our other observations weren't so heartening. For example, its level of total liabilities makes us a little nervous about its debt. When we consider all the elements mentioned above, it seems to us that Genuine Parts is managing its debt quite well. Having said that, the load is sufficiently heavy that we would recommend any shareholders keep a close eye on it. Of course, we wouldn't say no to the extra confidence that we'd gain if we knew that Genuine Parts insiders have been buying shares: if you're on the same wavelength, you can find out if insiders are buying by clicking this link.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About NYSE:GPC

Adequate balance sheet average dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

Vita Life Sciences Set for a 12.72% Revenue Growth While Tackling Operational Challenges

Fair Value AU$2.42|9.1% undervalued

RO

Community Contributor

Vossloh rides a €500 billion wave to boost growth and earnings in the next decade

Fair Value €78.41|6.1% undervalued

CH

Community Contributor

Intuitive Surgical Will Transform Healthcare with 12% Revenue Growth

Fair Value US$325.55|57.3% overvalued

UN

Community Contributor