Stock Analysis

- Brazil

- /

- Food and Staples Retail

- /

- BOVESPA:CRFB3

Does Atacadão (BVMF:CRFB3) Have A Healthy Balance Sheet?

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. Importantly, Atacadão S.A. (BVMF:CRFB3) does carry debt. But should shareholders be worried about its use of debt?

When Is Debt Dangerous?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

Check out our latest analysis for Atacadão

How Much Debt Does Atacadão Carry?

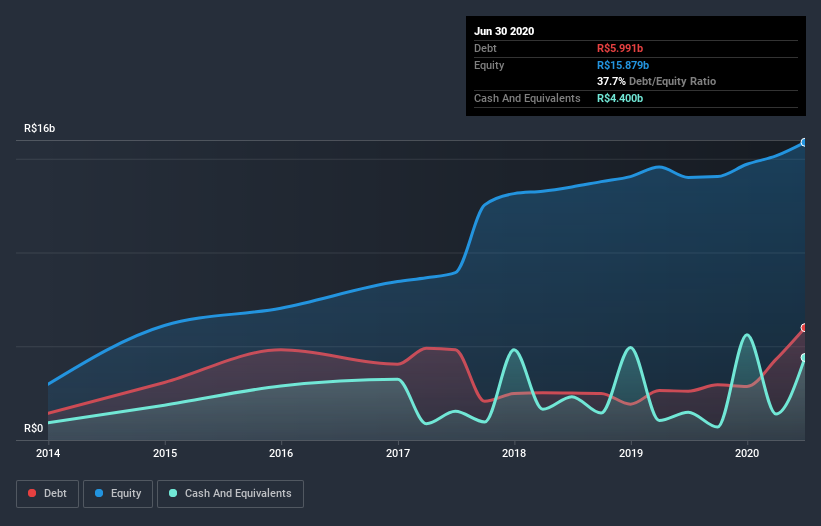

The image below, which you can click on for greater detail, shows that at June 2020 Atacadão had debt of R$5.99b, up from R$2.61b in one year. However, it also had R$4.40b in cash, and so its net debt is R$1.59b.

How Healthy Is Atacadão's Balance Sheet?

The latest balance sheet data shows that Atacadão had liabilities of R$19.1b due within a year, and liabilities of R$10.3b falling due after that. On the other hand, it had cash of R$4.40b and R$2.53b worth of receivables due within a year. So its liabilities total R$22.4b more than the combination of its cash and short-term receivables.

This deficit isn't so bad because Atacadão is worth R$38.4b, and thus could probably raise enough capital to shore up its balance sheet, if the need arose. However, it is still worthwhile taking a close look at its ability to pay off debt.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

With net debt sitting at just 0.34 times EBITDA, Atacadão is arguably pretty conservatively geared. And this view is supported by the solid interest coverage, with EBIT coming in at 9.1 times the interest expense over the last year. Also good is that Atacadão grew its EBIT at 10% over the last year, further increasing its ability to manage debt. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if Atacadão can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. Over the last three years, Atacadão reported free cash flow worth 6.3% of its EBIT, which is really quite low. That limp level of cash conversion undermines its ability to manage and pay down debt.

Our View

Atacadão's net debt to EBITDA was a real positive on this analysis, as was its interest cover. On the other hand, its conversion of EBIT to free cash flow makes us a little less comfortable about its debt. When we consider all the factors mentioned above, we do feel a bit cautious about Atacadão's use of debt. While debt does have its upside in higher potential returns, we think shareholders should definitely consider how debt levels might make the stock more risky. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. Consider for instance, the ever-present spectre of investment risk. We've identified 1 warning sign with Atacadão , and understanding them should be part of your investment process.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

If you decide to trade Atacadão, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Valuation is complex, but we're helping make it simple.

Find out whether Atacadão is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About BOVESPA:CRFB3

Atacadão

Engages in the wholesale and retail of food, clothing, home appliances, electronics, and other products in Brazil.

Very undervalued with moderate growth potential.