Advertisement

Constellation Software (TSE:CSU) Seems To Use Debt Rather Sparingly

Want to participate in a short research study? Help shape the future of investing tools and you could win a $250 gift card!

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. As with many other companies. Constellation Software Inc. (TSE:CSU) makes use of debt. But is this debt a concern to shareholders?

What Risk Does Debt Bring?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

View our latest analysis for Constellation Software

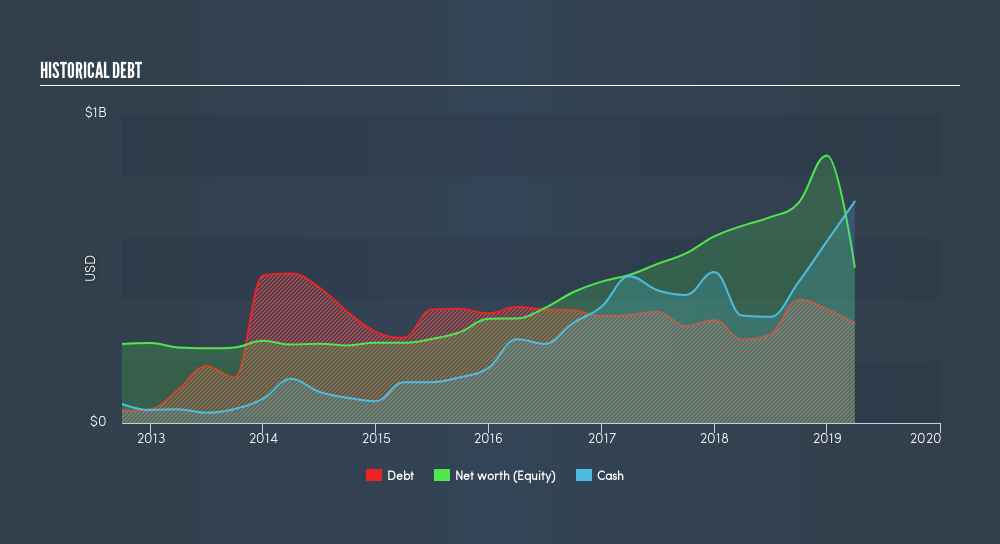

How Much Debt Does Constellation Software Carry?

The image below, which you can click on for greater detail, shows that at March 2019 Constellation Software had debt of US$323.0m, up from US$270.4m in one year. But on the other hand it also has US$717.0m in cash, leading to a US$394.0m net cash position.

A Look At Constellation Software's Liabilities

According to the last reported balance sheet, Constellation Software had liabilities of US$1.93b due within 12 months, and liabilities of US$888.0m due beyond 12 months. Offsetting these obligations, it had cash of US$717.0m as well as receivables valued at US$536.0m due within 12 months. So it has liabilities totalling US$1.57b more than its cash and near-term receivables, combined.

Since publicly traded Constellation Software shares are worth a very impressive total of US$20.2b, it seems unlikely that this level of liabilities would be a major threat. However, we do think it is worth keeping an eye on its balance sheet strength, as it may change over time. Constellation Software boasts net cash, so it's fair to say it does not have a heavy debt load!

Also positive, Constellation Software grew its EBIT by 26% in the last year, and that should make it easier to pay down debt, going forward. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if Constellation Software can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. Constellation Software may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. Happily for any shareholders, Constellation Software actually produced more free cash flow than EBIT over the last three years. That sort of strong cash conversion gets us excited like the crowd when the beat drops at a Daft Punk concert.

Summing up

While it is always sensible to look at a company's total liabilities, it is very reassuring that Constellation Software has US$394m in net cash. The cherry on top was that in converted 140% of that EBIT to free cash flow, bringing in US$660m. So is Constellation Software's debt a risk? It doesn't seem so to us. We'd be very excited to see if Constellation Software insiders have been snapping up shares. If you are too, then click on this link right now to take a (free) peek at our list of reported insider transactions.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About TSX:CSU

Constellation Software

Acquires, builds, and manages vertical market software businesses to develop mission-critical software solutions for public and private sector markets.

High growth potential with solid track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

Vita Life Sciences Set for a 12.72% Revenue Growth While Tackling Operational Challenges

Fair Value AU$2.42|12.0% undervalued

RO

Community Contributor

Vossloh rides a €500 billion wave to boost growth and earnings in the next decade

Fair Value €78.41|5.2% undervalued

CH

Community Contributor

Intuitive Surgical Will Transform Healthcare with 12% Revenue Growth

Fair Value US$325.55|57.3% overvalued

UN

Community Contributor