Stock Analysis

- Germany

- /

- Auto Components

- /

- XTRA:ZIL2

Why Investors Shouldn't Be Surprised By ElringKlinger AG's (ETR:ZIL2) 31% Share Price Surge

The ElringKlinger AG (ETR:ZIL2) share price has done very well over the last month, posting an excellent gain of 31%. Not all shareholders will be feeling jubilant, since the share price is still down a very disappointing 30% in the last twelve months.

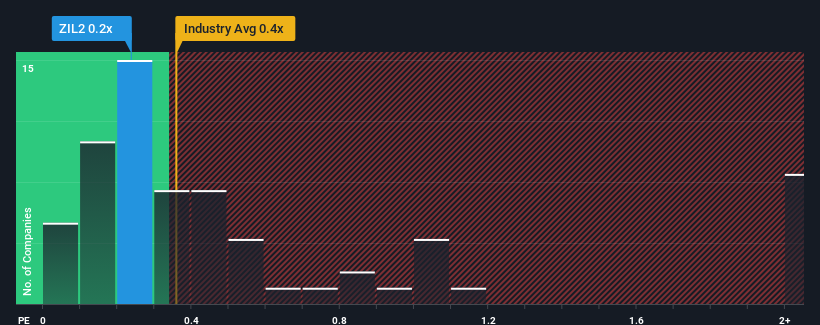

Even after such a large jump in price, there still wouldn't be many who think ElringKlinger's price-to-sales (or "P/S") ratio of 0.2x is worth a mention when the median P/S in Germany's Auto Components industry is similar at about 0.3x. Although, it's not wise to simply ignore the P/S without explanation as investors may be disregarding a distinct opportunity or a costly mistake.

View our latest analysis for ElringKlinger

How Has ElringKlinger Performed Recently?

Recent times haven't been great for ElringKlinger as its revenue has been rising slower than most other companies. It might be that many expect the uninspiring revenue performance to strengthen positively, which has kept the P/S ratio from falling. If not, then existing shareholders may be a little nervous about the viability of the share price.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on ElringKlinger.How Is ElringKlinger's Revenue Growth Trending?

ElringKlinger's P/S ratio would be typical for a company that's only expected to deliver moderate growth, and importantly, perform in line with the industry.

If we review the last year of revenue growth, the company posted a worthy increase of 2.7%. Revenue has also lifted 25% in aggregate from three years ago, partly thanks to the last 12 months of growth. Accordingly, shareholders would have probably been satisfied with the medium-term rates of revenue growth.

Looking ahead now, revenue is anticipated to climb by 5.9% each year during the coming three years according to the six analysts following the company. That's shaping up to be similar to the 4.8% per year growth forecast for the broader industry.

With this information, we can see why ElringKlinger is trading at a fairly similar P/S to the industry. Apparently shareholders are comfortable to simply hold on while the company is keeping a low profile.

The Final Word

ElringKlinger appears to be back in favour with a solid price jump bringing its P/S back in line with other companies in the industry It's argued the price-to-sales ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

We've seen that ElringKlinger maintains an adequate P/S seeing as its revenue growth figures match the rest of the industry. At this stage investors feel the potential for an improvement or deterioration in revenue isn't great enough to push P/S in a higher or lower direction. If all things remain constant, the possibility of a drastic share price movement remains fairly remote.

Don't forget that there may be other risks. For instance, we've identified 1 warning sign for ElringKlinger that you should be aware of.

It's important to make sure you look for a great company, not just the first idea you come across. So if growing profitability aligns with your idea of a great company, take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

Valuation is complex, but we're helping make it simple.

Find out whether ElringKlinger is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Simply Wall St

About XTRA:ZIL2

ElringKlinger

ElringKlinger AG develops, manufactures, and sells systems and components for the automotive industry in Germany, the Asia-Pacific, North America, rest of Europe, and internationally.

Flawless balance sheet and good value.