Stock Analysis

Y.Z. Queenco Ltd. (TLV:QNCO) recently posted some strong earnings, and the market responded positively. We did some digging and found some further encouraging factors that investors will like.

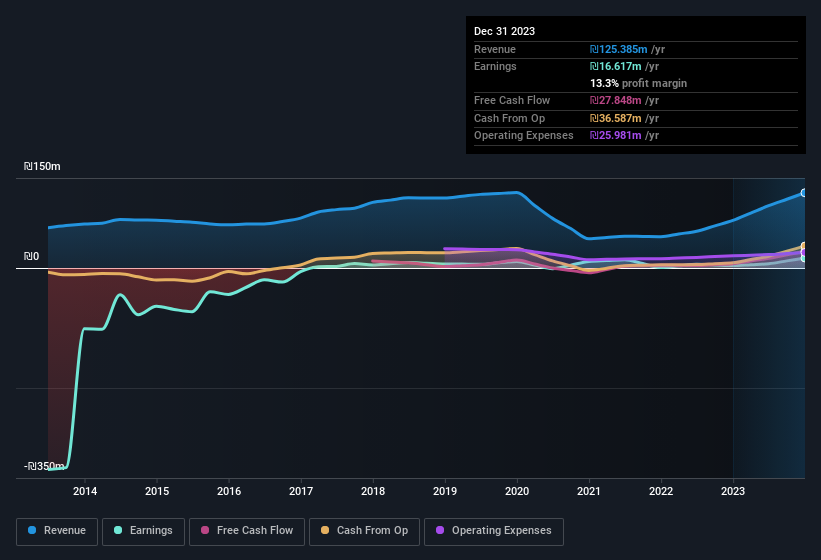

Check out our latest analysis for Y.Z. Queenco

A Closer Look At Y.Z. Queenco's Earnings

Many investors haven't heard of the accrual ratio from cashflow, but it is actually a useful measure of how well a company's profit is backed up by free cash flow (FCF) during a given period. The accrual ratio subtracts the FCF from the profit for a given period, and divides the result by the average operating assets of the company over that time. This ratio tells us how much of a company's profit is not backed by free cashflow.

As a result, a negative accrual ratio is a positive for the company, and a positive accrual ratio is a negative. While it's not a problem to have a positive accrual ratio, indicating a certain level of non-cash profits, a high accrual ratio is arguably a bad thing, because it indicates paper profits are not matched by cash flow. Notably, there is some academic evidence that suggests that a high accrual ratio is a bad sign for near-term profits, generally speaking.

Over the twelve months to December 2023, Y.Z. Queenco recorded an accrual ratio of -0.11. That indicates that its free cash flow was a fair bit more than its statutory profit. In fact, it had free cash flow of ₪28m in the last year, which was a lot more than its statutory profit of ₪16.6m. Y.Z. Queenco shareholders are no doubt pleased that free cash flow improved over the last twelve months.

Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of Y.Z. Queenco.

Our Take On Y.Z. Queenco's Profit Performance

Y.Z. Queenco's accrual ratio is solid, and indicates strong free cash flow, as we discussed, above. Because of this, we think Y.Z. Queenco's earnings potential is at least as good as it seems, and maybe even better! Furthermore, it has done a great job growing EPS over the last year. At the end of the day, it's essential to consider more than just the factors above, if you want to understand the company properly. If you'd like to know more about Y.Z. Queenco as a business, it's important to be aware of any risks it's facing. Every company has risks, and we've spotted 2 warning signs for Y.Z. Queenco (of which 1 is a bit unpleasant!) you should know about.

This note has only looked at a single factor that sheds light on the nature of Y.Z. Queenco's profit. But there is always more to discover if you are capable of focussing your mind on minutiae. For example, many people consider a high return on equity as an indication of favorable business economics, while others like to 'follow the money' and search out stocks that insiders are buying. While it might take a little research on your behalf, you may find this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying to be useful.

Valuation is complex, but we're helping make it simple.

Find out whether Y.Z. Queenco is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TASE:QNCO

Solid track record with excellent balance sheet.