Stock Analysis

- Sweden

- /

- Trade Distributors

- /

- OM:OEM B

We Think OEM International (STO:OEM B) Can Stay On Top Of Its Debt

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We note that OEM International AB (publ) (STO:OEM B) does have debt on its balance sheet. But is this debt a concern to shareholders?

Why Does Debt Bring Risk?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first step when considering a company's debt levels is to consider its cash and debt together.

See our latest analysis for OEM International

What Is OEM International's Debt?

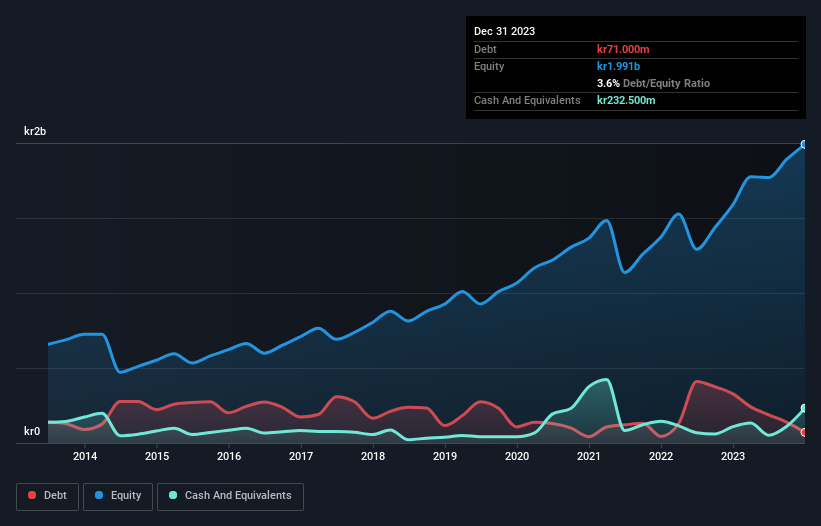

The image below, which you can click on for greater detail, shows that OEM International had debt of kr71.0m at the end of December 2023, a reduction from kr327.5m over a year. However, it does have kr232.5m in cash offsetting this, leading to net cash of kr161.5m.

How Strong Is OEM International's Balance Sheet?

We can see from the most recent balance sheet that OEM International had liabilities of kr679.7m falling due within a year, and liabilities of kr261.1m due beyond that. Offsetting these obligations, it had cash of kr232.5m as well as receivables valued at kr769.4m due within 12 months. So it can boast kr61.1m more liquid assets than total liabilities.

This state of affairs indicates that OEM International's balance sheet looks quite solid, as its total liabilities are just about equal to its liquid assets. So while it's hard to imagine that the kr14.0b company is struggling for cash, we still think it's worth monitoring its balance sheet. Succinctly put, OEM International boasts net cash, so it's fair to say it does not have a heavy debt load!

Fortunately, OEM International grew its EBIT by 6.4% in the last year, making that debt load look even more manageable. The balance sheet is clearly the area to focus on when you are analysing debt. But you can't view debt in total isolation; since OEM International will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. OEM International may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. Over the most recent three years, OEM International recorded free cash flow worth 59% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This cold hard cash means it can reduce its debt when it wants to.

Summing Up

While it is always sensible to investigate a company's debt, in this case OEM International has kr161.5m in net cash and a decent-looking balance sheet. So is OEM International's debt a risk? It doesn't seem so to us. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. These risks can be hard to spot. Every company has them, and we've spotted 1 warning sign for OEM International you should know about.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

Valuation is complex, but we're helping make it simple.

Find out whether OEM International is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Simply Wall St

About OM:OEM B

OEM International

OEM International AB (publ), together with its subsidiaries, provides products and systems for industrial applications.

Flawless balance sheet average dividend payer.