Stock Analysis

- South Korea

- /

- Interactive Media and Services

- /

- KOSE:A035420

We Think NAVER (KRX:035420) Can Stay On Top Of Its Debt

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We note that NAVER Corporation (KRX:035420) does have debt on its balance sheet. But should shareholders be worried about its use of debt?

What Risk Does Debt Bring?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we think about a company's use of debt, we first look at cash and debt together.

View our latest analysis for NAVER

What Is NAVER's Debt?

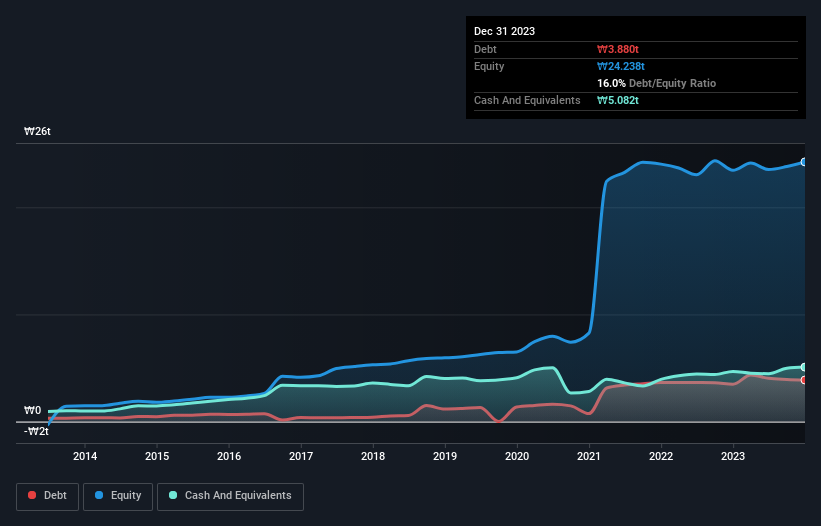

As you can see below, at the end of December 2023, NAVER had ₩3.88t of debt, up from ₩3.49t a year ago. Click the image for more detail. But on the other hand it also has ₩5.08t in cash, leading to a ₩1.20t net cash position.

A Look At NAVER's Liabilities

Zooming in on the latest balance sheet data, we can see that NAVER had liabilities of ₩6.31t due within 12 months and liabilities of ₩5.19t due beyond that. Offsetting these obligations, it had cash of ₩5.08t as well as receivables valued at ₩1.72t due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by ₩4.70t.

Of course, NAVER has a titanic market capitalization of ₩28t, so these liabilities are probably manageable. Having said that, it's clear that we should continue to monitor its balance sheet, lest it change for the worse. While it does have liabilities worth noting, NAVER also has more cash than debt, so we're pretty confident it can manage its debt safely.

Also good is that NAVER grew its EBIT at 14% over the last year, further increasing its ability to manage debt. There's no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine NAVER's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. NAVER may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. During the last three years, NAVER produced sturdy free cash flow equating to 63% of its EBIT, about what we'd expect. This cold hard cash means it can reduce its debt when it wants to.

Summing Up

While NAVER does have more liabilities than liquid assets, it also has net cash of ₩1.20t. So we don't think NAVER's use of debt is risky. Over time, share prices tend to follow earnings per share, so if you're interested in NAVER, you may well want to click here to check an interactive graph of its earnings per share history.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

Valuation is complex, but we're helping make it simple.

Find out whether NAVER is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Simply Wall St

About KOSE:A035420

NAVER

NAVER Corporation, together with its subsidiaries, provides internet and online search portal, and mobile messenger platform services in South Korea, Japan, and internationally.

Flawless balance sheet with solid track record.