Stock Analysis

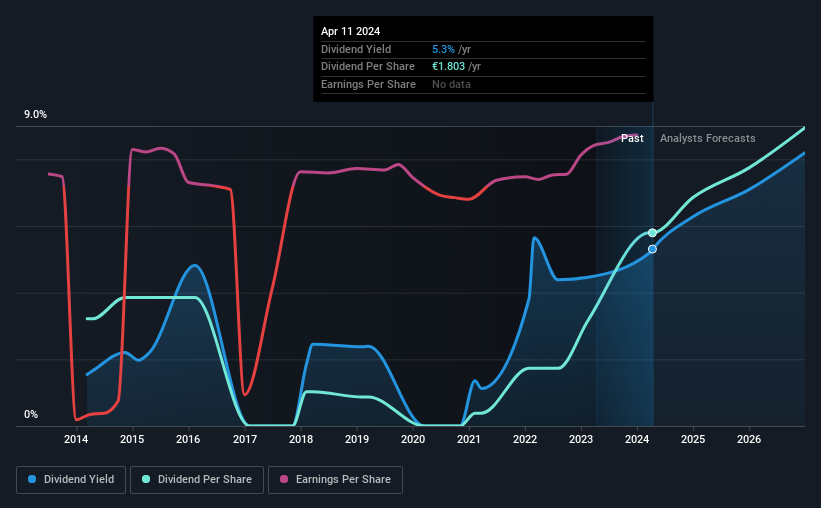

UniCredit S.p.A. (BIT:UCG) will increase its dividend from last year's comparable payment on the 24th of April to €1.8. Based on this payment, the dividend yield for the company will be 5.3%, which is fairly typical for the industry.

While the dividend yield is important for income investors, it is also important to consider any large share price moves, as this will generally outweigh any gains from distributions. Investors will be pleased to see that UniCredit's stock price has increased by 32% in the last 3 months, which is good for shareholders and can also explain a decrease in the dividend yield.

View our latest analysis for UniCredit

UniCredit's Dividend Forecasted To Be Well Covered By Earnings

Unless the payments are sustainable, the dividend yield doesn't mean too much.

UniCredit has established itself as a dividend paying company with over 10 years history of distributing earnings to shareholders. Past distributions do not necessarily guarantee future ones, but UniCredit's payout ratio of 35% is a good sign as this means that earnings decently cover dividends.

The next 3 years are set to see EPS grow by 14.4%. The future payout ratio could be 49% over that time period, according to analyst estimates, which is a good look for the future of the dividend.

Dividend Volatility

The company has a long dividend track record, but it doesn't look great with cuts in the past. Since 2014, the dividend has gone from €1.00 total annually to €1.8. This means that it has been growing its distributions at 6.1% per annum over that time. A reasonable rate of dividend growth is good to see, but we're wary that the dividend history is not as solid as we'd like, having been cut at least once.

The Dividend Looks Likely To Grow

Given that the dividend has been cut in the past, we need to check if earnings are growing and if that might lead to stronger dividends in the future. UniCredit has seen EPS rising for the last five years, at 26% per annum. Rapid earnings growth and a low payout ratio suggest this company has been effectively reinvesting in its business. Should that continue, this company could have a bright future.

UniCredit Looks Like A Great Dividend Stock

In summary, it is always positive to see the dividend being increased, and we are particularly pleased with its overall sustainability. Distributions are quite easily covered by earnings, which are also being converted to cash flows. All in all, this checks a lot of the boxes we look for when choosing an income stock.

Investors generally tend to favour companies with a consistent, stable dividend policy as opposed to those operating an irregular one. Still, investors need to consider a host of other factors, apart from dividend payments, when analysing a company. Just as an example, we've come across 2 warning signs for UniCredit you should be aware of, and 1 of them is potentially serious. Is UniCredit not quite the opportunity you were looking for? Why not check out our selection of top dividend stocks.

Valuation is complex, but we're helping make it simple.

Find out whether UniCredit is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Simply Wall St

About BIT:UCG

UniCredit

UniCredit S.p.A. provides commercial banking services in Italy, Germany, Central Europe, and Eastern Europe.

Undervalued with proven track record and pays a dividend.