Stock Analysis

- South Korea

- /

- Auto Components

- /

- KOSDAQ:A123410

There's No Escaping Korea Fuel-Tech Corporation's (KOSDAQ:123410) Muted Earnings Despite A 26% Share Price Rise

Korea Fuel-Tech Corporation (KOSDAQ:123410) shares have continued their recent momentum with a 26% gain in the last month alone. The annual gain comes to 111% following the latest surge, making investors sit up and take notice.

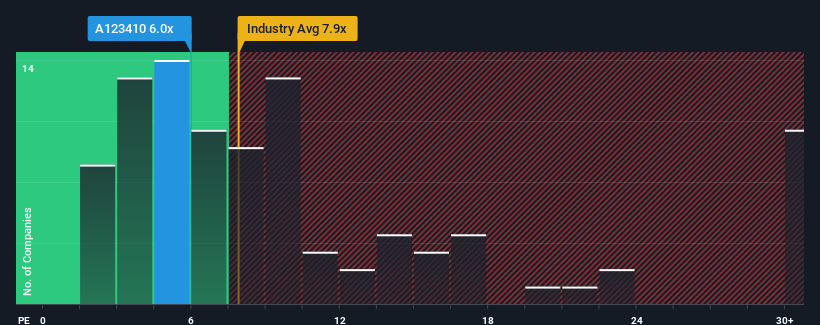

Although its price has surged higher, Korea Fuel-Tech's price-to-earnings (or "P/E") ratio of 6x might still make it look like a strong buy right now compared to the market in Korea, where around half of the companies have P/E ratios above 13x and even P/E's above 27x are quite common. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's so limited.

With its earnings growth in positive territory compared to the declining earnings of most other companies, Korea Fuel-Tech has been doing quite well of late. One possibility is that the P/E is low because investors think the company's earnings are going to fall away like everyone else's soon. If not, then existing shareholders have reason to be quite optimistic about the future direction of the share price.

Check out our latest analysis for Korea Fuel-Tech

What Are Growth Metrics Telling Us About The Low P/E?

The only time you'd be truly comfortable seeing a P/E as depressed as Korea Fuel-Tech's is when the company's growth is on track to lag the market decidedly.

If we review the last year of earnings growth, the company posted a terrific increase of 227%. Pleasingly, EPS has also lifted 730% in aggregate from three years ago, thanks to the last 12 months of growth. So we can start by confirming that the company has done a great job of growing earnings over that time.

Shifting to the future, estimates from the two analysts covering the company suggest earnings growth is heading into negative territory, declining 0.9% over the next year. Meanwhile, the broader market is forecast to expand by 27%, which paints a poor picture.

With this information, we are not surprised that Korea Fuel-Tech is trading at a P/E lower than the market. However, shrinking earnings are unlikely to lead to a stable P/E over the longer term. There's potential for the P/E to fall to even lower levels if the company doesn't improve its profitability.

What We Can Learn From Korea Fuel-Tech's P/E?

Shares in Korea Fuel-Tech are going to need a lot more upward momentum to get the company's P/E out of its slump. While the price-to-earnings ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of earnings expectations.

As we suspected, our examination of Korea Fuel-Tech's analyst forecasts revealed that its outlook for shrinking earnings is contributing to its low P/E. Right now shareholders are accepting the low P/E as they concede future earnings probably won't provide any pleasant surprises. Unless these conditions improve, they will continue to form a barrier for the share price around these levels.

We don't want to rain on the parade too much, but we did also find 2 warning signs for Korea Fuel-Tech that you need to be mindful of.

If you're unsure about the strength of Korea Fuel-Tech's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Valuation is complex, but we're helping make it simple.

Find out whether Korea Fuel-Tech is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Simply Wall St

About KOSDAQ:A123410

Korea Fuel-Tech

Korea Fuel-Tech Corporation manufactures and sells automotive fuel systems and components in South Korea and internationally.

Flawless balance sheet with solid track record.