Stock Analysis

- Brazil

- /

- Paper and Forestry Products

- /

- BOVESPA:DXCO3

Slowing Rates Of Return At Dexco (BVMF:DXCO3) Leave Little Room For Excitement

If you're not sure where to start when looking for the next multi-bagger, there are a few key trends you should keep an eye out for. Firstly, we'd want to identify a growing return on capital employed (ROCE) and then alongside that, an ever-increasing base of capital employed. This shows us that it's a compounding machine, able to continually reinvest its earnings back into the business and generate higher returns. However, after briefly looking over the numbers, we don't think Dexco (BVMF:DXCO3) has the makings of a multi-bagger going forward, but let's have a look at why that may be.

Understanding Return On Capital Employed (ROCE)

Just to clarify if you're unsure, ROCE is a metric for evaluating how much pre-tax income (in percentage terms) a company earns on the capital invested in its business. Analysts use this formula to calculate it for Dexco:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

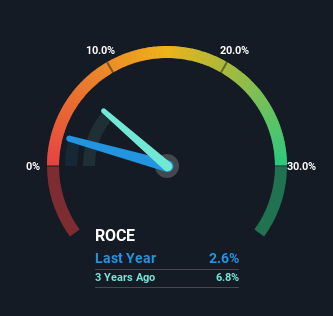

0.026 = R$373m ÷ (R$18b - R$3.6b) (Based on the trailing twelve months to December 2023).

Thus, Dexco has an ROCE of 2.6%. Ultimately, that's a low return and it under-performs the Forestry industry average of 8.4%.

Check out our latest analysis for Dexco

In the above chart we have measured Dexco's prior ROCE against its prior performance, but the future is arguably more important. If you're interested, you can view the analysts predictions in our free analyst report for Dexco .

How Are Returns Trending?

In terms of Dexco's historical ROCE trend, it doesn't exactly demand attention. The company has employed 93% more capital in the last five years, and the returns on that capital have remained stable at 2.6%. Given the company has increased the amount of capital employed, it appears the investments that have been made simply don't provide a high return on capital.

In Conclusion...

As we've seen above, Dexco's returns on capital haven't increased but it is reinvesting in the business. And with the stock having returned a mere 8.7% in the last five years to shareholders, you could argue that they're aware of these lackluster trends. As a result, if you're hunting for a multi-bagger, we think you'd have more luck elsewhere.

If you'd like to know more about Dexco, we've spotted 4 warning signs, and 1 of them is significant.

If you want to search for solid companies with great earnings, check out this free list of companies with good balance sheets and impressive returns on equity.

Valuation is complex, but we're helping make it simple.

Find out whether Dexco is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About BOVESPA:DXCO3

Dexco

Dexco S.A., together with its subsidiaries, produces and sells wood panels in Brazil and internationally.

Acceptable track record and slightly overvalued.