Stock Analysis

- United Arab Emirates

- /

- Basic Materials

- /

- ADX:EMSTEEL

Risks To Shareholder Returns Are Elevated At These Prices For Ensteel Building Materials PJSC (ADX:EMSTEEL)

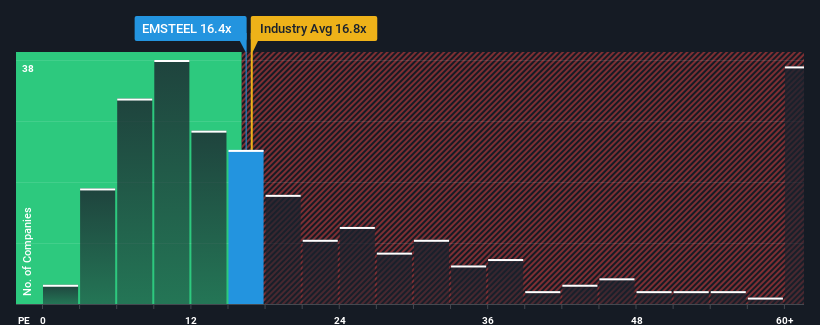

Ensteel Building Materials PJSC's (ADX:EMSTEEL) price-to-earnings (or "P/E") ratio of 16.4x might make it look like a sell right now compared to the market in the United Arab Emirates, where around half of the companies have P/E ratios below 14x and even P/E's below 8x are quite common. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the elevated P/E.

The earnings growth achieved at Ensteel Building Materials PJSC over the last year would be more than acceptable for most companies. It might be that many expect the respectable earnings performance to beat most other companies over the coming period, which has increased investors’ willingness to pay up for the stock. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

See our latest analysis for Ensteel Building Materials PJSC

Is There Enough Growth For Ensteel Building Materials PJSC?

Ensteel Building Materials PJSC's P/E ratio would be typical for a company that's expected to deliver solid growth, and importantly, perform better than the market.

If we review the last year of earnings growth, the company posted a terrific increase of 18%. Still, EPS has barely risen at all from three years ago in total, which is not ideal. So it appears to us that the company has had a mixed result in terms of growing earnings over that time.

It's interesting to note that the rest of the market is similarly expected to grow by 1.6% over the next year, which is fairly even with the company's recent medium-term annualised growth rates.

With this information, we find it interesting that Ensteel Building Materials PJSC is trading at a high P/E compared to the market. It seems most investors are ignoring the fairly average recent growth rates and are willing to pay up for exposure to the stock. Nevertheless, they may be setting themselves up for future disappointment if the P/E falls to levels more in line with recent growth rates.

The Bottom Line On Ensteel Building Materials PJSC's P/E

We'd say the price-to-earnings ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

We've established that Ensteel Building Materials PJSC currently trades on a higher than expected P/E since its recent three-year growth is only in line with the wider market forecast. Right now we are uncomfortable with the high P/E as this earnings performance isn't likely to support such positive sentiment for long. Unless the recent medium-term conditions improve, it's challenging to accept these prices as being reasonable.

A lot of potential risks can sit within a company's balance sheet. Take a look at our free balance sheet analysis for Ensteel Building Materials PJSC with six simple checks on some of these key factors.

If P/E ratios interest you, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

Valuation is complex, but we're helping make it simple.

Find out whether Ensteel Building Materials PJSC is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Simply Wall St

About ADX:EMSTEEL

Ensteel Building Materials PJSC

Ensteel Building Materials PJSC engages in the operation, trading, and investment in industrial projects and commercial business involved in the building materials and steel sectors primarily in the United Arab Emirates.

Flawless balance sheet and good value.