Stock Analysis

- India

- /

- Electrical

- /

- NSEI:RAMRAT

Investors Still Aren't Entirely Convinced By Ram Ratna Wires Limited's (NSE:RAMRAT) Earnings Despite 30% Price Jump

Ram Ratna Wires Limited (NSE:RAMRAT) shares have had a really impressive month, gaining 30% after a shaky period beforehand. The last 30 days bring the annual gain to a very sharp 69%.

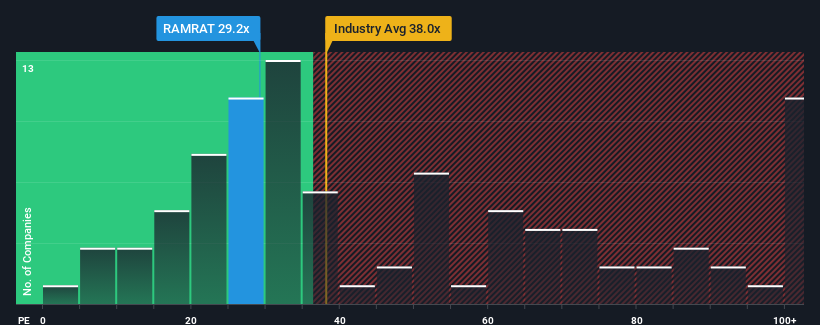

In spite of the firm bounce in price, there still wouldn't be many who think Ram Ratna Wires' price-to-earnings (or "P/E") ratio of 29.2x is worth a mention when the median P/E in India is similar at about 31x. While this might not raise any eyebrows, if the P/E ratio is not justified investors could be missing out on a potential opportunity or ignoring looming disappointment.

Ram Ratna Wires has been doing a decent job lately as it's been growing earnings at a reasonable pace. One possibility is that the P/E is moderate because investors think this good earnings growth might only be parallel to the broader market in the near future. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's not quite in favour.

Check out our latest analysis for Ram Ratna Wires

Is There Some Growth For Ram Ratna Wires?

There's an inherent assumption that a company should be matching the market for P/E ratios like Ram Ratna Wires' to be considered reasonable.

Taking a look back first, we see that the company managed to grow earnings per share by a handy 7.3% last year. Pleasingly, EPS has also lifted 628% in aggregate from three years ago, partly thanks to the last 12 months of growth. Accordingly, shareholders would have probably welcomed those medium-term rates of earnings growth.

Comparing that to the market, which is only predicted to deliver 24% growth in the next 12 months, the company's momentum is stronger based on recent medium-term annualised earnings results.

With this information, we find it interesting that Ram Ratna Wires is trading at a fairly similar P/E to the market. Apparently some shareholders believe the recent performance is at its limits and have been accepting lower selling prices.

The Bottom Line On Ram Ratna Wires' P/E

Ram Ratna Wires appears to be back in favour with a solid price jump getting its P/E back in line with most other companies. It's argued the price-to-earnings ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

We've established that Ram Ratna Wires currently trades on a lower than expected P/E since its recent three-year growth is higher than the wider market forecast. When we see strong earnings with faster-than-market growth, we assume potential risks are what might be placing pressure on the P/E ratio. At least the risk of a price drop looks to be subdued if recent medium-term earnings trends continue, but investors seem to think future earnings could see some volatility.

Before you take the next step, you should know about the 1 warning sign for Ram Ratna Wires that we have uncovered.

Of course, you might also be able to find a better stock than Ram Ratna Wires. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Valuation is complex, but we're helping make it simple.

Find out whether Ram Ratna Wires is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:RAMRAT

Ram Ratna Wires

Ram Ratna Wires Limited manufactures and sells winding wires and related insulated products for original equipment manufacturers in India.

Excellent balance sheet average dividend payer.