Stock Analysis

- Taiwan

- /

- Infrastructure

- /

- TWSE:2607

Here's Why Evergreen International Storage & Transport (TWSE:2607) Can Manage Its Debt Responsibly

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We note that Evergreen International Storage & Transport Corporation (TWSE:2607) does have debt on its balance sheet. But should shareholders be worried about its use of debt?

When Is Debt Dangerous?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we examine debt levels, we first consider both cash and debt levels, together.

Check out our latest analysis for Evergreen International Storage & Transport

How Much Debt Does Evergreen International Storage & Transport Carry?

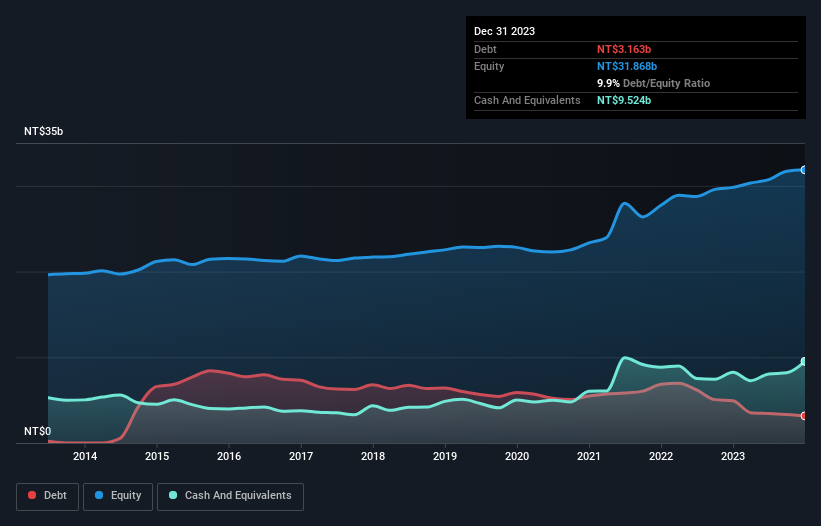

You can click the graphic below for the historical numbers, but it shows that Evergreen International Storage & Transport had NT$3.16b of debt in December 2023, down from NT$4.92b, one year before. But it also has NT$9.52b in cash to offset that, meaning it has NT$6.36b net cash.

How Strong Is Evergreen International Storage & Transport's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Evergreen International Storage & Transport had liabilities of NT$3.67b due within 12 months and liabilities of NT$7.88b due beyond that. On the other hand, it had cash of NT$9.52b and NT$5.18b worth of receivables due within a year. So it can boast NT$3.16b more liquid assets than total liabilities.

This short term liquidity is a sign that Evergreen International Storage & Transport could probably pay off its debt with ease, as its balance sheet is far from stretched. Succinctly put, Evergreen International Storage & Transport boasts net cash, so it's fair to say it does not have a heavy debt load!

On the other hand, Evergreen International Storage & Transport's EBIT dived 19%, over the last year. If that rate of decline in earnings continues, the company could find itself in a tight spot. When analysing debt levels, the balance sheet is the obvious place to start. But you can't view debt in total isolation; since Evergreen International Storage & Transport will need earnings to service that debt. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. While Evergreen International Storage & Transport has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. Happily for any shareholders, Evergreen International Storage & Transport actually produced more free cash flow than EBIT over the last three years. That sort of strong cash conversion gets us as excited as the crowd when the beat drops at a Daft Punk concert.

Summing Up

While it is always sensible to investigate a company's debt, in this case Evergreen International Storage & Transport has NT$6.36b in net cash and a decent-looking balance sheet. The cherry on top was that in converted 182% of that EBIT to free cash flow, bringing in NT$4.5b. So we don't think Evergreen International Storage & Transport's use of debt is risky. Another positive for shareholders is that it pays dividends. So if you like receiving those dividend payments, check Evergreen International Storage & Transport's dividend history, without delay!

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

Valuation is complex, but we're helping make it simple.

Find out whether Evergreen International Storage & Transport is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TWSE:2607

Evergreen International Storage & Transport

Evergreen International Storage & Transport Corporation provides inland haulage, marine terminal stevedoring and chartering, and passenger transportation services.

Flawless balance sheet established dividend payer.