Stock Analysis

- Canada

- /

- Oil and Gas

- /

- TSX:PPL

Getting In Cheap On Pembina Pipeline Corporation (TSE:PPL) Is Unlikely

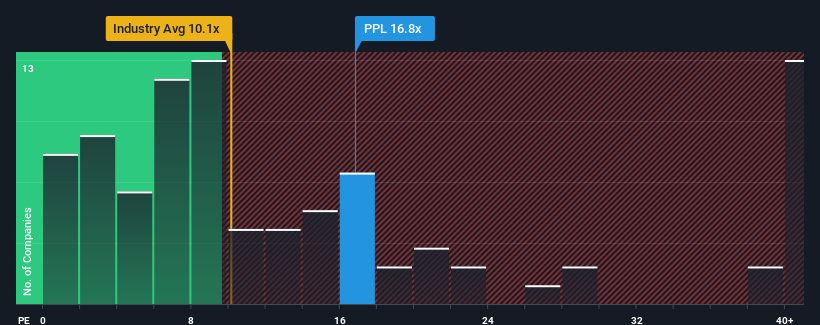

When close to half the companies in Canada have price-to-earnings ratios (or "P/E's") below 14x, you may consider Pembina Pipeline Corporation (TSE:PPL) as a stock to potentially avoid with its 16.8x P/E ratio. However, the P/E might be high for a reason and it requires further investigation to determine if it's justified.

Recent times haven't been advantageous for Pembina Pipeline as its earnings have been falling quicker than most other companies. It might be that many expect the dismal earnings performance to recover substantially, which has kept the P/E from collapsing. If not, then existing shareholders may be very nervous about the viability of the share price.

See our latest analysis for Pembina Pipeline

Is There Enough Growth For Pembina Pipeline?

Pembina Pipeline's P/E ratio would be typical for a company that's expected to deliver solid growth, and importantly, perform better than the market.

If we review the last year of earnings, dishearteningly the company's profits fell to the tune of 42%. This has erased any of its gains during the last three years, with practically no change in EPS being achieved in total. Accordingly, shareholders probably wouldn't have been overly satisfied with the unstable medium-term growth rates.

Shifting to the future, estimates from the eight analysts covering the company suggest earnings should grow by 6.5% each year over the next three years. Meanwhile, the rest of the market is forecast to expand by 8.6% per annum, which is noticeably more attractive.

With this information, we find it concerning that Pembina Pipeline is trading at a P/E higher than the market. It seems most investors are hoping for a turnaround in the company's business prospects, but the analyst cohort is not so confident this will happen. Only the boldest would assume these prices are sustainable as this level of earnings growth is likely to weigh heavily on the share price eventually.

The Final Word

Generally, our preference is to limit the use of the price-to-earnings ratio to establishing what the market thinks about the overall health of a company.

Our examination of Pembina Pipeline's analyst forecasts revealed that its inferior earnings outlook isn't impacting its high P/E anywhere near as much as we would have predicted. When we see a weak earnings outlook with slower than market growth, we suspect the share price is at risk of declining, sending the high P/E lower. Unless these conditions improve markedly, it's very challenging to accept these prices as being reasonable.

You always need to take note of risks, for example - Pembina Pipeline has 2 warning signs we think you should be aware of.

Of course, you might also be able to find a better stock than Pembina Pipeline. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Valuation is complex, but we're helping make it simple.

Find out whether Pembina Pipeline is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Simply Wall St

About TSX:PPL

Pembina Pipeline

Pembina Pipeline Corporation provides energy transportation and midstream services.

Established dividend payer and fair value.