Stock Analysis

- Hong Kong

- /

- Construction

- /

- SEHK:1546

Further Upside For Thelloy Development Group Limited (HKG:1546) Shares Could Introduce Price Risks After 28% Bounce

Thelloy Development Group Limited (HKG:1546) shares have had a really impressive month, gaining 28% after a shaky period beforehand. But the last month did very little to improve the 53% share price decline over the last year.

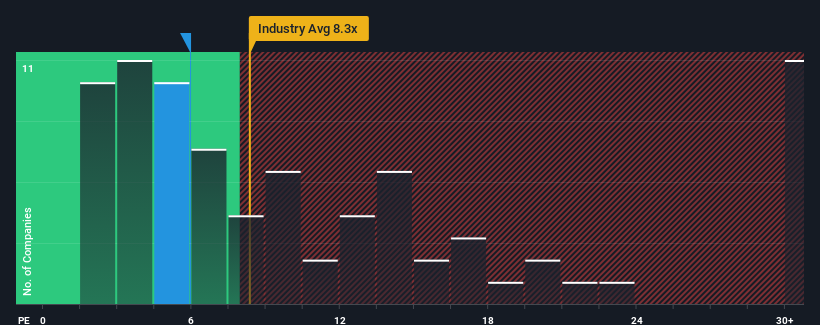

Even after such a large jump in price, Thelloy Development Group may still be sending bullish signals at the moment with its price-to-earnings (or "P/E") ratio of 5.9x, since almost half of all companies in Hong Kong have P/E ratios greater than 10x and even P/E's higher than 18x are not unusual. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's limited.

For example, consider that Thelloy Development Group's financial performance has been poor lately as its earnings have been in decline. One possibility is that the P/E is low because investors think the company won't do enough to avoid underperforming the broader market in the near future. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's out of favour.

Check out our latest analysis for Thelloy Development Group

How Is Thelloy Development Group's Growth Trending?

Thelloy Development Group's P/E ratio would be typical for a company that's only expected to deliver limited growth, and importantly, perform worse than the market.

If we review the last year of earnings, dishearteningly the company's profits fell to the tune of 34%. Still, the latest three year period has seen an excellent 172% overall rise in EPS, in spite of its unsatisfying short-term performance. Accordingly, while they would have preferred to keep the run going, shareholders would probably welcome the medium-term rates of earnings growth.

Comparing that to the market, which is only predicted to deliver 21% growth in the next 12 months, the company's momentum is stronger based on recent medium-term annualised earnings results.

In light of this, it's peculiar that Thelloy Development Group's P/E sits below the majority of other companies. Apparently some shareholders believe the recent performance has exceeded its limits and have been accepting significantly lower selling prices.

The Key Takeaway

Despite Thelloy Development Group's shares building up a head of steam, its P/E still lags most other companies. Typically, we'd caution against reading too much into price-to-earnings ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

We've established that Thelloy Development Group currently trades on a much lower than expected P/E since its recent three-year growth is higher than the wider market forecast. When we see strong earnings with faster-than-market growth, we assume potential risks are what might be placing significant pressure on the P/E ratio. At least price risks look to be very low if recent medium-term earnings trends continue, but investors seem to think future earnings could see a lot of volatility.

Plus, you should also learn about these 4 warning signs we've spotted with Thelloy Development Group (including 3 which are significant).

If these risks are making you reconsider your opinion on Thelloy Development Group, explore our interactive list of high quality stocks to get an idea of what else is out there.

Valuation is complex, but we're helping make it simple.

Find out whether Thelloy Development Group is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:1546

Thelloy Development Group

Thelloy Development Group Limited, an investment holding company, provides building construction services primarily in Hong Kong.

Good value with adequate balance sheet.