Advertisement

- India

- /

- Oil and Gas

- /

- NSEI:BPCL

A Sliding Share Price Has Us Looking At Bharat Petroleum Corporation Limited's (NSE:BPCL) P/E Ratio

To the annoyance of some shareholders, Bharat Petroleum (NSE:BPCL) shares are down a considerable 43% in the last month. Even longer term holders have taken a real hit with the stock declining 30% in the last year.

All else being equal, a share price drop should make a stock more attractive to potential investors. While the market sentiment towards a stock is very changeable, in the long run, the share price will tend to move in the same direction as earnings per share. The implication here is that long term investors have an opportunity when expectations of a company are too low. One way to gauge market expectations of a stock is to look at its Price to Earnings Ratio (PE Ratio). A high P/E implies that investors have high expectations of what a company can achieve compared to a company with a low P/E ratio.

Check out our latest analysis for Bharat Petroleum

How Does Bharat Petroleum's P/E Ratio Compare To Its Peers?

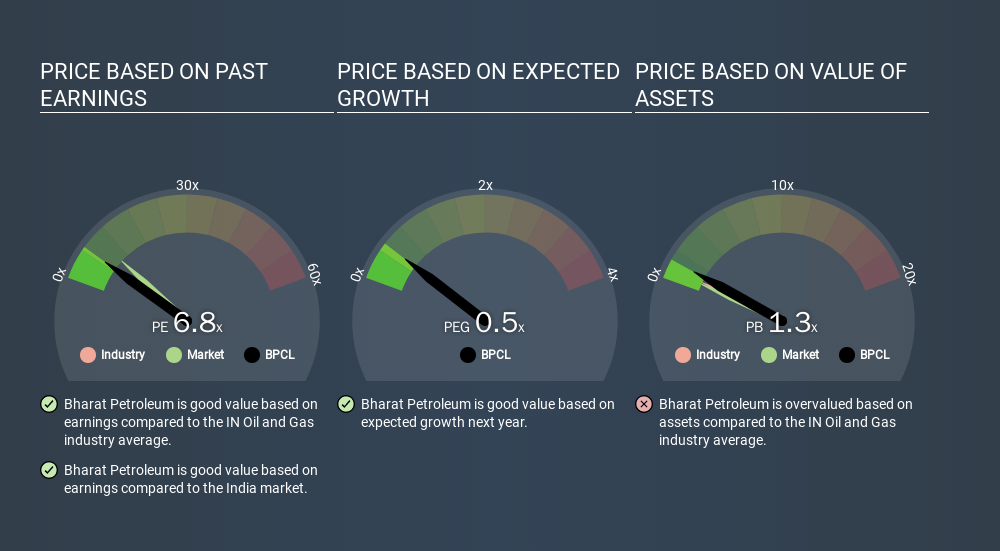

Bharat Petroleum's P/E is 6.78. You can see in the image below that the average P/E (6.9) for companies in the oil and gas industry is roughly the same as Bharat Petroleum's P/E.

Its P/E ratio suggests that Bharat Petroleum shareholders think that in the future it will perform about the same as other companies in its industry classification. The company could surprise by performing better than average, in the future. I would further inform my view by checking insider buying and selling., among other things.

How Growth Rates Impact P/E Ratios

When earnings fall, the 'E' decreases, over time. That means unless the share price falls, the P/E will increase in a few years. A higher P/E should indicate the stock is expensive relative to others -- and that may encourage shareholders to sell.

Bharat Petroleum's earnings per share fell by 3.5% in the last twelve months. But EPS is up 12% over the last 5 years. And it has shrunk its earnings per share by 3.6% per year over the last three years. This growth rate might warrant a low P/E ratio. So we might expect a relatively low P/E.

A Limitation: P/E Ratios Ignore Debt and Cash In The Bank

Don't forget that the P/E ratio considers market capitalization. In other words, it does not consider any debt or cash that the company may have on the balance sheet. In theory, a company can lower its future P/E ratio by using cash or debt to invest in growth.

Spending on growth might be good or bad a few years later, but the point is that the P/E ratio does not account for the option (or lack thereof).

How Does Bharat Petroleum's Debt Impact Its P/E Ratio?

Bharat Petroleum's net debt equates to 49% of its market capitalization. You'd want to be aware of this fact, but it doesn't bother us.

The Verdict On Bharat Petroleum's P/E Ratio

Bharat Petroleum has a P/E of 6.8. That's below the average in the IN market, which is 9.7. The debt levels are not a major concern, but the lack of EPS growth is likely weighing on sentiment. Given Bharat Petroleum's P/E ratio has declined from 11.9 to 6.8 in the last month, we know for sure that the market is more worried about the business today, than it was back then. For those who prefer to invest with the flow of momentum, that might be a bad sign, but for deep value investors this stock might justify some research.

When the market is wrong about a stock, it gives savvy investors an opportunity. If it is underestimating a company, investors can make money by buying and holding the shares until the market corrects itself. So this free visualization of the analyst consensus on future earnings could help you make the right decision about whether to buy, sell, or hold.

You might be able to find a better buy than Bharat Petroleum. If you want a selection of possible winners, check out this free list of interesting companies that trade on a P/E below 20 (but have proven they can grow earnings).

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About NSEI:BPCL

Bharat Petroleum

Primarily engages in refining crude oil and marketing petroleum products in India and internationally.

Established dividend payer with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|36.2% undervalued

JO

Community Contributor

Occidental Petroleum is set to achieve a 16% profit margin improvement

Fair Value US$55.05|18.7% undervalued

DZ

Community Contributor

Argan's Revenue Set to Soar with a 13.31% Growth in the Coming Decade

Fair Value US$284.68|22.0% undervalued

KE

Community Contributor

EU#1 - From German Startup to EU’s Biggest Company

Fair Value €248.62|5.0% overvalued

TO

Community Contributor