Advertisement

A Rising Share Price Has Us Looking Closely At Irani Papel e Embalagem S.A.'s (BVMF:RANI3) P/E Ratio

It's really great to see that even after a strong run, Irani Papel e Embalagem (BVMF:RANI3) shares have been powering on, with a gain of 59% in the last thirty days. Zooming out, the annual gain of 106% knocks our socks off.

Assuming no other changes, a sharply higher share price makes a stock less attractive to potential buyers. While the market sentiment towards a stock is very changeable, in the long run, the share price will tend to move in the same direction as earnings per share. The implication here is that deep value investors might steer clear when expectations of a company are too high. Perhaps the simplest way to get a read on investors' expectations of a business is to look at its Price to Earnings Ratio (PE Ratio). Investors have optimistic expectations of companies with higher P/E ratios, compared to companies with lower P/E ratios.

See our latest analysis for Irani Papel e Embalagem

How Does Irani Papel e Embalagem's P/E Ratio Compare To Its Peers?

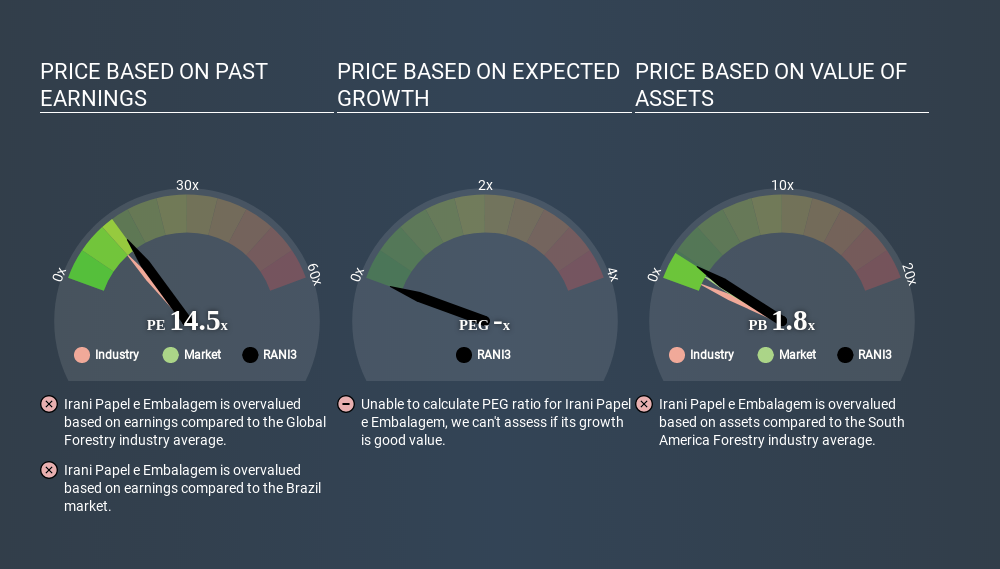

We can tell from its P/E ratio of 19.33 that there is some investor optimism about Irani Papel e Embalagem. The image below shows that Irani Papel e Embalagem has a higher P/E than the average (12.7) P/E for companies in the forestry industry.

Irani Papel e Embalagem's P/E tells us that market participants think the company will perform better than its industry peers, going forward. The market is optimistic about the future, but that doesn't guarantee future growth. So investors should always consider the P/E ratio alongside other factors, such as whether company directors have been buying shares.

How Growth Rates Impact P/E Ratios

Probably the most important factor in determining what P/E a company trades on is the earnings growth. If earnings are growing quickly, then the 'E' in the equation will increase faster than it would otherwise. Therefore, even if you pay a high multiple of earnings now, that multiple will become lower in the future. So while a stock may look expensive based on past earnings, it could be cheap based on future earnings.

Notably, Irani Papel e Embalagem grew EPS by a whopping 37% in the last year. Unfortunately, earnings per share are down 6.8% a year, over 5 years.

Don't Forget: The P/E Does Not Account For Debt or Bank Deposits

One drawback of using a P/E ratio is that it considers market capitalization, but not the balance sheet. That means it doesn't take debt or cash into account. Hypothetically, a company could reduce its future P/E ratio by spending its cash (or taking on debt) to achieve higher earnings.

Such spending might be good or bad, overall, but the key point here is that you need to look at debt to understand the P/E ratio in context.

Irani Papel e Embalagem's Balance Sheet

Irani Papel e Embalagem has net debt worth 86% of its market capitalization. If you want to compare its P/E ratio to other companies, you should absolutely keep in mind it has significant borrowings.

The Verdict On Irani Papel e Embalagem's P/E Ratio

Irani Papel e Embalagem's P/E is 19.3 which is above average (14.5) in its market. While its debt levels are rather high, at least its EPS is growing quickly. So it seems likely the market is overlooking the debt because of the fast earnings growth. What we know for sure is that investors have become much more excited about Irani Papel e Embalagem recently, since they have pushed its P/E ratio from 12.2 to 19.3 over the last month. For those who prefer to invest with the flow of momentum, that might mean it's time to put the stock on a watchlist, or research it. But the contrarian may see it as a missed opportunity.

When the market is wrong about a stock, it gives savvy investors an opportunity. If the reality for a company is better than it expects, you can make money by buying and holding for the long term. We don't have analyst forecasts, but shareholders might want to examine this detailed historical graph of earnings, revenue and cash flow.

You might be able to find a better buy than Irani Papel e Embalagem. If you want a selection of possible winners, check out this free list of interesting companies that trade on a P/E below 20 (but have proven they can grow earnings).

Love or hate this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned. Thank you for reading.

About BOVESPA:RANI3

Irani Papel e Embalagem

Manufactures and sells corrugated cardboard and packaging papers in Brazil and internationally.

Very undervalued with proven track record and pays a dividend.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor