Last Update 02 Jun 26

Fair value Decreased 0.65%ALO: Large Contract Pipeline And Margin Gains Should Support Higher Future P/E

Alstom's analyst price targets have edged lower, with one major bank trimming its view by €1 to €27 and others cutting targets by as much as €6.30, as analysts factor in slightly softer revenue growth assumptions, modestly higher margin expectations, and a reduced discount rate.

Analyst Commentary

Bullish Takeaways

- Bullish analysts point to recent target raises, such as the €2 increase from Morgan Stanley, as a signal that they see room for upside if Alstom can execute on its plans and meet internal milestones.

- Higher margin expectations in some models suggest confidence that management can improve profitability, which would support current valuations even if revenue growth assumptions remain more cautious.

- Upgrades from research houses that now see the stock more favorably indicate that, for some, the risk and reward profile looks more balanced, especially with a lower discount rate being used in valuations.

- Price targets that still stand above current trading levels, even after reductions such as JPMorgan’s move to €27, signal that bullish analysts continue to view the long term growth story as intact, provided execution stays on track.

Bearish Takeaways

- Bearish analysts highlight repeated target cuts, including reductions of up to €6.30 and €3, as a sign that expectations for future value creation are being recalibrated lower.

- Resumptions at Hold and fresh downgrades reflect caution around execution risk, with some analysts preferring to wait for clearer evidence that margins and cash generation can consistently support current valuations.

- The combination of softer revenue growth assumptions and a more conservative view on the stock suggests that bearish analysts see limited room for disappointment without putting further pressure on price targets.

- Recent downgrades frame the stock as one where the balance of risks is still uncertain, with analysts flagging that any slip in delivery or order momentum could weigh on already trimmed valuation models.

What's in the News

- Alstom has a board meeting scheduled for May 12, 2026, with an agenda to review the management report and consolidated financial statements. (Source: Company event filing)

- The company signed a €295 million contract with Transports publics de la région lausannoise to modernise Lausanne’s m2 metro line, including a new CBTC signalling system and mid life train fleet upgrades, with work phased to limit service disruption. (Source: Client announcement)

- Alstom recorded a signalling contract in Europe worth approximately €295 million in its fourth quarter of fiscal 2025/2026. (Source: Client announcement)

- As part of a consortium in the AMECA region, Alstom agreed a new systems contract with a total project value of US$2.75b, with Alstom’s share at about 30%, or roughly €700 million, booked in the fourth quarter of fiscal 2025/2026. (Source: Client announcement)

- The company secured several large transport contracts, including a €915 million turnkey deal for Belgrade Metro Line 1 and a €380 million contract to upgrade and operate Houston Airport’s Skyway APM system for 15 years. It also signed long term O&M agreements in Canada and the UK, as well as a €1,030 million train supply contract in Portugal linked to a new manufacturing site and job creation. (Source: Client and product announcements)

Valuation Changes

- Fair Value: €22.04 to €21.89, a small move lower of about 0.6%.

- Discount Rate: 9.22% to 8.90%, a modest reduction of roughly 0.3 percentage points.

- Revenue Growth: 5.52% to 5.25%, a slight trim of about 0.27 percentage points in projected growth.

- Profit Margin: 3.71% to 3.86%, a small uplift of around 0.15 percentage points in expected profitability.

- Future P/E: 15.93x to 15.15x, a decrease of around 4.9% in the valuation multiple used.

Key Takeaways

- Focus on high-quality, margin-accretive orders in Services and Signaling is expected to boost revenue growth and future margins.

- Industrial restructuring and supply chain management improve operational efficiency, enhancing net margins and financial performance.

- Supply chain challenges, low-margin legacy contracts, and immature technology reliance strain Alstom's profitability, cash flows, and future revenue growth prospects.

Catalysts

About Alstom- Provides solutions for rail transport industry in Europe, the Americas, Asia and Pacific, the Middle East, Central Asia, and Africa.

- Alstom's strategy of focusing on high-quality, margin-accretive orders, especially in Services and Signaling, is expected to improve revenue growth and increase future gross margins.

- The company is conducting industrial restructuring to optimize its manufacturing setup, which aims to enhance operational efficiency and potentially improve net margins and earnings.

- Significant future opportunities lie in Alstom's strong order pipeline, especially in Europe, the Middle East, and Asia Pacific, with €200 billion expected in orders over the next three years, which could enhance revenue.

- Alstom's ongoing focus on project execution and mitigating supply chain challenges should lead to more efficient delivery volumes, which may improve both earnings and net margins as production stabilizes.

- Continuous improvement in gross margins in rolling stock and enhanced contract management could lead to better financial performance and higher profitability, enhancing adjusted EBIT and overall earnings.

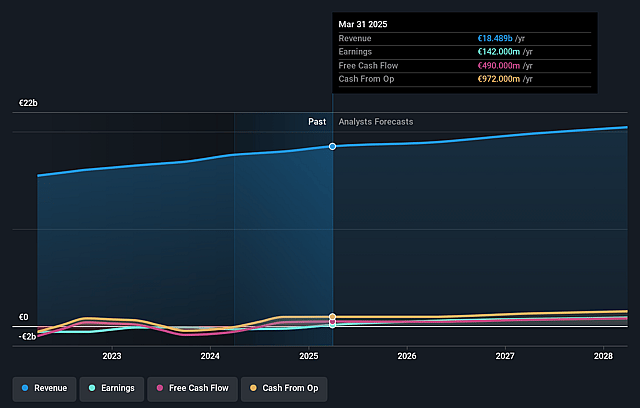

Alstom Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Alstom's revenue will grow by 5.2% annually over the next 3 years.

- Analysts assume that profit margins will increase from 1.5% today to 3.9% in 3 years time.

- Analysts expect earnings to reach €862.2 million (and earnings per share of €1.88) by about June 2029, up from €279.0 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 15.2x on those 2029 earnings, down from 28.6x today. This future PE is lower than the current PE for the GB Machinery industry at 27.3x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.9%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Supply chain challenges are causing significant delays in rolling stock production, impacting Alstom's ability to meet contractual deadlines and potentially leading to penalties, affecting future revenue and margins.

- A large portion of the current backlog consists of legacy contracts, which continue to weigh on Alstom’s profitability due to lower margins, impacting net earnings growth.

- The increased inventory levels due to production delays signify potential working capital challenges, which can strain cash flows and impact free cash flow targets.

- The reliance on new technologies with less mature supply chains, such as batteries and fuel cells, poses risks to seamless execution and could affect overall project costs, impacting gross margins.

- Weaker-than-expected market conditions in the Americas and green mobility sectors introduce revenue risks if similar trends persist, potentially affecting future revenue growth.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of €21.89 for Alstom based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of €28.0, and the most bearish reporting a price target of just €10.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be €22.4 billion, earnings will come to €862.2 million, and it would be trading on a PE ratio of 15.2x, assuming you use a discount rate of 8.9%.

- Given the current share price of €17.27, the analyst price target of €21.89 is 21.1% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Alstom?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.