Last Update 22 Jun 26

BTS B: Split 2026 Dividend And Stable Forecasts Will Support Fair Value

Analysts have kept their SEK 177.50 price target for BTS Group unchanged, with only minor tweaks to the discount rate, revenue growth, profit margin and future P/E inputs. These reflect small adjustments to their valuation framework rather than a shift in overall conviction.

What’s in the News for BTS Group

- BTS Group AB (publ) shareholders approved a dividend of SEK 4.40 per share at the Annual General Meeting, according to company disclosures.

- The dividend is split into two payments of SEK 2.20 per share each, as set out in the AGM resolution.

- The record date for the first SEK 2.20 dividend payment was set to Monday, May 25, 2026, with payment expected on Thursday, May 28, 2026.

- The record date for the second SEK 2.20 dividend payment was set to Monday, November 9, 2026, with payment expected on Thursday, November 12, 2026.

- Company filings describe this AGM decision as part of a Dividend Decreases event type, based on the classification in the key developments source.

Valuation Changes for BTS Group

- Fair Value: SEK 177.50 is unchanged, indicating a stable central valuation estimate for BTS Group.

- Discount Rate: slipped slightly from 5.93% to 5.89%, a small adjustment to the risk and return assumption used in the model.

- Revenue Growth: kept effectively unchanged at around 6.00%, with only a marginal recalculation in the model inputs.

- Net Profit Margin: maintained at approximately 8.45%, with only a very small numerical refinement in the forecast.

- Future P/E: adjusted slightly from about 15.0x to 15.0x, reflecting a minor tweak to the longer term earnings multiple assumption.

Key Takeaways

- Structural shifts toward AI, remote learning, and micro-mobility threaten traditional consulting services, risking lower client demand and pressured long-term growth.

- Higher inflation, operating costs, and increased leverage constrain profitability, while operational setbacks and acquisition risks add to lingering earnings uncertainty.

- Strong European momentum, surging AI services, efficiency gains, and resilient recurring revenues position the group for growth and margin expansion amid effective management adaptiveness.

Catalysts

About BTS Group- Operates as a professional services firm.

- The proliferation of smart mobility platforms and increased adoption of AI-powered self-service tools are intensifying competition and enabling clients to handle training, coaching, and simulation internally, which may erode BTS Group's future revenue growth and result in lower win rates in core markets.

- Heightened macroeconomic uncertainty, including persistent inflation and higher interest rates, could substantially increase BTS's financing and operating costs, putting sustained pressure on net margins and limiting the positive earnings impact from any cost-saving initiatives.

- Rising client demand for alternative learning and talent development solutions-such as micro-mobility, remote training, and telecommuting-may reduce reliance on traditional in-person consulting and leadership development, posing structural risks to BTS's core business model and potentially depressing long-term revenue growth.

- Ongoing operational setbacks in North America, especially lower sales efficiency and delays in client decision-making, suggest that the expected return to double-digit growth may take longer than anticipated, resulting in prolonged earnings weakness and negatively affecting both revenue and margins.

- Strategic acquisitions and continued investments in digital and AI capabilities have increased the company's leverage and debt burden; if revenue growth does not accelerate as expected, elevated interest expenses could further compress net margins and reduce overall profitability.

BTS Group Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

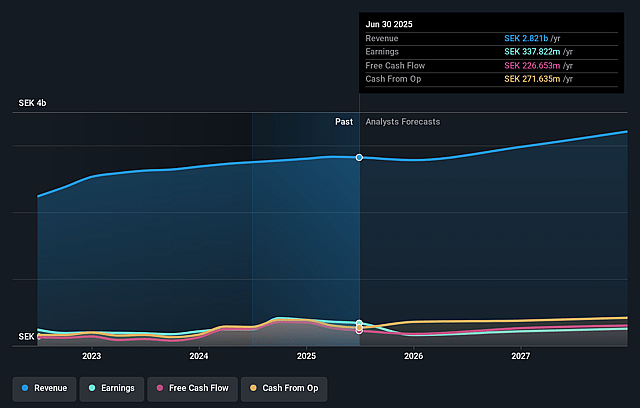

- Analysts are assuming BTS Group's revenue will grow by 6.0% annually over the next 3 years.

- Analysts assume that profit margins will increase from 5.1% today to 8.4% in 3 years time.

- Analysts expect earnings to reach SEK 267.3 million (and earnings per share of SEK 12.25) by about June 2029, up from SEK 135.5 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 15.3x on those 2029 earnings, down from 24.0x today. This future PE is lower than the current PE for the GB Professional Services industry at 17.3x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 5.89%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Strong momentum in Europe and Other markets-with double-digit growth resuming, high win rates (60%+ on large deals in Europe), favorable business mix, and ongoing expansion in regions like the Middle East and Brazil-indicates diversified and resilient revenue streams that can offset weakness in one geography, supporting long-term revenue and earnings growth.

- Rapid growth in AI-related services and technology platforms (AI adoption services revenue up 425% year-on-year, subscription AI platform bookings doubling QoQ) points to a high-margin and scalable new business line, which, if sustained, could lift group net margins and drive overall earnings upward through both direct sales and ingrained digital adoption.

- AI-driven and automation cost-saving initiatives-including a reduction of 7% in core headcount and a $5 million cost-saving phase-are expected to improve operational efficiency and boost net margins. These ongoing productivity improvements provide a structural tailwind for profitability and earnings resilience over the long term.

- The coaching business is experiencing robust organic profit growth (EBITDA up 34% in Q2) with record-high renewal rates, indicating growing demand and client stickiness. This recurring and expanding revenue base can strengthen group earnings stability and improve margins through repeat business.

- Management's historical track record in successfully turning around underperforming regions-illustrated by prior double-digit growth rebound in North America and current rapid implementation of best practices and AI integration-suggests an ability to adapt and restore growth and profit, raising the potential for revenue and earnings recovery in the group's largest market.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of SEK177.5 for BTS Group based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be SEK3.2 billion, earnings will come to SEK267.3 million, and it would be trading on a PE ratio of 15.3x, assuming you use a discount rate of 5.9%.

- Given the current share price of SEK168.0, the analyst price target of SEK177.5 is 5.4% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on BTS Group?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.