Last Update 15 Jun 26

Fair value Decreased 4.91%TFG: Dividend And Earnings Reset Will Still Support Future Upside Potential

Analysts have trimmed their ZAR price target for Foschini Group by ZAR4.00 to ZAR77.46. This reflects updated views on slightly softer revenue growth, a marginally lower profit margin profile and a reduced forward P/E assumption.

What's in the News

- Directors declared a final ordinary gross cash dividend of ZAR1.40 per share, or ZAR1.12 per share net of 20% dividend withholding tax, for the period ended 31 March 2026, sourced from income reserves.

- The dividend applies to 331,027,300 ordinary shares in issue at the declaration date, with the last day to trade to receive the dividend on 14 July 2026 and shares trading ex dividend from 15 July 2026.

- The record date for the dividend is 17 July 2026, with payment scheduled for 20 July 2026.

- The company issued earnings guidance for the year ended 31 March 2026, indicating expected earnings per share in a range of 343.2 cents to 441.3 cents.

- The guided earnings per share range reflects an anticipated decline of 65% to 55% compared with the prior period, according to the company’s update.

Valuation Changes

- Fair Value: Trimmed from ZAR81.46 to ZAR77.46, a reduction of about 4.9% in the modelled estimate.

- Discount Rate: Adjusted from 24.10% to 22.86%, indicating a slightly lower required return in the latest assumptions.

- Revenue Growth: Revised from 5.46% to 4.29%, reflecting a more cautious outlook for ZAR revenue expansion.

- Net Profit Margin: Tweaked from 4.30% to 4.15%, pointing to a modestly leaner profitability assumption.

- Future P/E: Reset from 16.24x to 14.07x, implying a lower valuation multiple applied to forward earnings in the updated model.

Key Takeaways

- Strategic investments and acquisitions are expected to increase market share, revenue, and profitability across multiple regions and product categories.

- Supply chain optimization and local manufacturing efficiencies are anticipated to enhance net margins and improve overall operating performance.

- Challenging economic conditions and reliance on cost optimization pose risks to Foschini Group's revenue growth and profitability across its major markets.

Catalysts

About Foschini Group- Operates retail stores in South Africa and internationally.

- The Foschini Group is expected to gain market share in current retail verticals and adjacent categories due to recent investments in TFG Africa, potentially boosting future revenue growth.

- Gross margin recovery in TFG Africa, along with strengthened local manufacturing and efficiencies from new distribution centers, is expected to enhance net margins and earnings.

- The acquisition of White Stuff in the U.K. is anticipated to boost TFG's revenue and profitability due to its casual lifestyle products and international expansion opportunities.

- Continued expansion of Tapestry's brands and Jet's successful revamp program indicate strong future revenue growth, with potential improvements in net margins due to locally manufactured products.

- The company's strategic focus on optimizing its supply chain and leveraging technology, including the Bash platform, is likely to improve operating efficiencies, positively impacting earnings.

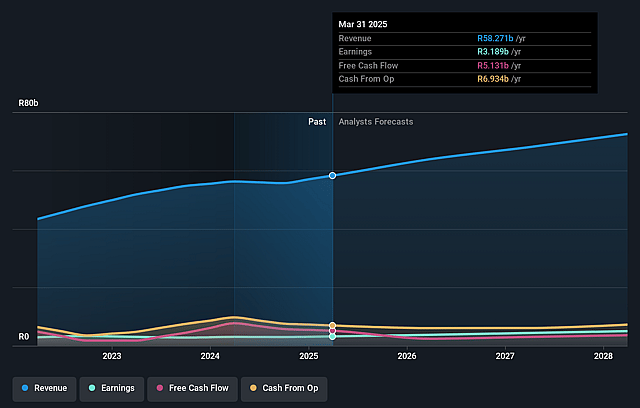

Foschini Group Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Foschini Group's revenue will grow by 4.3% annually over the next 3 years.

- Analysts assume that profit margins will increase from 2.1% today to 4.2% in 3 years time.

- Analysts expect earnings to reach ZAR 2.9 billion (and earnings per share of ZAR 8.62) by about June 2029, up from ZAR 1.3 billion today. However, there is some disagreement amongst the analysts with the more bullish ones expecting earnings as high as ZAR3.6 billion.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 14.1x on those 2029 earnings, down from 15.3x today. This future PE is greater than the current PE for the ZA Specialty Retail industry at 11.7x.

- Analysts expect the number of shares outstanding to decline by 2.87% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 22.86%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- The overall economic environment in TFG's major geographies has been challenging, with low consumer confidence, elevated inflation, and interest rates, which could impact future revenue growth.

- TFG Africa's revenue was flat, and this is partly attributed to an artificially high sales base from the prior year and a challenging operating environment, indicating a risk in maintaining revenue growth.

- The international business segments in the U.K. and Australia have experienced revenue contraction despite improvements in margins, posing a risk to overall earnings stabilization.

- Tapestry and Jet, despite recent improvements, are still navigating through rightsizing and store portfolio adjustments. Any missteps could lead to volatile revenue streams or increased costs.

- There is a reliance on optimizing costs to maintain profitability amid shrinking or flat revenues, which inherently carries the risk of future cost cutting impacting business capabilities or growth potential, potentially affecting net margins negatively.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of ZAR77.46 for Foschini Group based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of ZAR100.0, and the most bearish reporting a price target of just ZAR65.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be ZAR70.8 billion, earnings will come to ZAR2.9 billion, and it would be trading on a PE ratio of 14.1x, assuming you use a discount rate of 22.9%.

- Given the current share price of ZAR63.97, the analyst price target of ZAR77.46 is 17.4% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Foschini Group?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.