Catalysts

About Vitesse Energy

Vitesse Energy acquires and develops oil and gas interests with a focus on high return, low leverage production growth and reliable shareholder distributions.

What are the underlying business or industry changes driving this perspective?

- Migration of drilling activity into Vitesse's previously noncore Bakken acreage, supported by over 2 million net lateral feet of remaining development and more than 200 net 2 mile equivalent wells, provides a long runway for production growth and higher revenue visibility as these locations are converted into cash flowing assets.

- Rapid adoption of 3 and 4 mile extended laterals by operating partners, which meaningfully lowers drilling and completion cost per lateral foot while maintaining strong well performance, should lift capital efficiency and expand net margins as more of the program shifts to these longer laterals.

- Successful integration of the Lucero acquisition, including 2 wells that came on more than 15 percent under budget and above initial production expectations plus roughly 15 net undeveloped operated locations, creates a platform for a 2026 and 2027 operated program that can accelerate earnings growth while supporting the dividend.

- Low leverage with net debt to adjusted annualized EBITDA of 0.65 times, combined with disciplined hedging at attractive oil and gas prices, positions Vitesse to stay active and potentially opportunistic on acquisitions through commodity and credit cycles, smoothing cash flows and supporting more stable earnings and dividend capacity.

- Robust acquisition pipeline in a strong AFE market and a wide lens on both oil weighted Bakken assets and gas opportunities, underpinned by well funded operators and ongoing basin consolidation, enhances Vitesse's ability to add high return inventory and scale production, driving higher long term revenue and cash flow per share.

Assumptions

This narrative explores a more optimistic perspective on Vitesse Energy compared to the consensus, based on a Fair Value that aligns with the bullish cohort of analysts. How have these above catalysts been quantified?

- The bullish analysts are assuming Vitesse Energy's revenue will grow by 4.1% annually over the next 3 years.

- The bullish analysts assume that profit margins will shrink from 8.4% today to 0.1% in 3 years time.

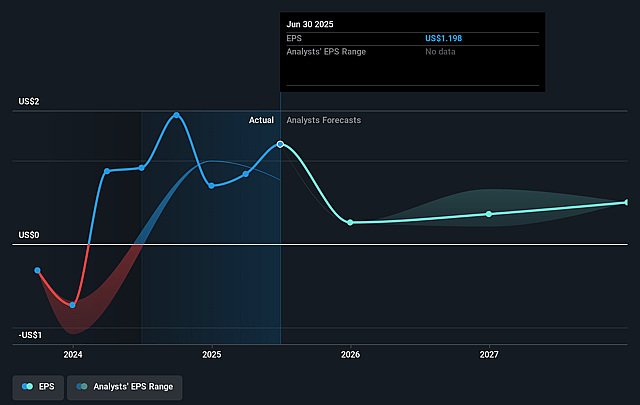

- The bullish analysts expect earnings to reach $201.1 thousand (and earnings per share of $0.43) by about December 2028, down from $20.9 million today. However, there is some disagreement amongst the analysts with the more bearish ones expecting earnings as low as $36.6 thousand.

- In order for the above numbers to justify the price target of the more bullish analyst cohort, the company would need to trade at a PE ratio of 7585.2x on those 2028 earnings, up from 40.2x today. This future PE is greater than the current PE for the US Oil and Gas industry at 13.3x.

- The bullish analysts expect the number of shares outstanding to grow by 0.25% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.96%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?

- The company remains heavily exposed to the highly cyclical oil and gas industry, so a prolonged period of weaker commodity prices beyond current hedging horizons could erode the economics of its remaining 2 million net lateral feet of development and over 200 net 2 mile equivalent wells, pressuring long term revenue and compressing net margins and earnings.

- Despite solid adjusted EBITDA, the most recent quarter produced a GAAP net loss of $1.3 million while funding $31.8 million of CapEx from operating cash flows, and if well performance or cost control deteriorates over time, the need to sustain elevated CapEx to grow production could structurally weaken profitability and constrain earnings growth.

- The strategy depends on continued high drilling activity and capital spending by well funded Bakken operators, yet ongoing industry consolidation and shifting 2026 and 2027 budgets could redirect rigs away from Vitesse acreage or slow development pace, reducing the conversion of inventory into producing wells and limiting revenue and EBITDA expansion.

- The company is increasingly active in a very competitive acquisition and AFE market, and as the M&A environment remains frenetic across oil and gas, the pressure to secure deals may eventually force Vitesse to accept lower return opportunities or misjudge gas assets, which would dilute return on invested capital and weigh on net margins and future earnings.

- The commitment to a substantial dividend at an annual rate of $2.25 per share in the face of cyclical prices, rising guidance for annual CapEx between $110 million and $125 million, and ongoing leverage of $108 million in net debt with a 0.65 times net debt to adjusted annualized EBITDA ratio could become unsustainable in a downturn, increasing the risk of dividend cuts or balance sheet stress that negatively impacts earnings and cash flow based valuation.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The assumed bullish price target for Vitesse Energy is $32.0, which represents up to two standard deviations above the consensus price target of $25.0. This valuation is based on what can be assumed as the expectations of Vitesse Energy's future earnings growth, profit margins and other risk factors from analysts on the bullish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $32.0, and the most bearish reporting a price target of just $20.0.

- In order for you to agree with the more bullish analyst cohort, you'd need to believe that by 2028, revenues will be $280.2 million, earnings will come to $201.1 thousand, and it would be trading on a PE ratio of 7585.2x, assuming you use a discount rate of 7.0%.

- Given the current share price of $21.71, the analyst price target of $32.0 is 32.2% higher. Despite analysts expecting the underlying business to decline, they seem to believe it's more valuable than what the market thinks.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Vitesse Energy?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystHighTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystHighTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystHighTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.