Last Update 21 Jul 26

Fair value Increased 2.57%EDPR: U.S. Exposure And 2026 Stock Split Will Shape Future Returns

Analysts have nudged their fair value estimate for EDP Renewables higher, lifting the implied price target from about €14.36 to roughly €14.73. They cite stronger conviction in the company’s U.S. renewables exposure and updated Street research that includes recent upgrades and higher external targets around €17.50.

Analyst Commentary

Recent research on EDP Renewables focuses heavily on how its U.S. portfolio, pricing assumptions and sector return expectations flow through to valuation. Here is how the Street is framing the opportunity and the risks.

Bullish Takeaways

- Bullish analysts highlight that U.S. renewable activities account for about 65% of EDP Renewables' business, which they view as an important driver of the updated price targets around €17.50.

- Goldman Sachs points to what it sees as a gap between the market view and its own assessment of industry returns, and uses this to support a higher fair value range for the stock.

- Recent upgrades and higher external targets are cited as reinforcing confidence in EDP Renewables' growth pipeline and its ability to execute on U.S. projects.

- The clustering of target prices closer to €17.50 than to the internal fair value estimate around €14.73 suggests that some bullish analysts see additional upside if EDP Renewables delivers in line with their expectations.

Bearish Takeaways

- Bears remain cautious that, despite higher targets, the current market price could already reflect a meaningful portion of the U.S. renewables opportunity, limiting the margin of safety.

- Some bearish analysts question whether industry returns will match the more optimistic views, which could leave EDP Renewables' valuation exposed if project economics or funding costs differ from assumptions.

- The reliance on U.S. activities for about 65% of the business means execution issues, policy changes or delays in that market could have a material effect on growth and cash flow expectations.

- There is ongoing debate around how quickly EDP Renewables can convert its pipeline into operating assets, and any slower than expected pace could challenge the higher end of current valuation ranges.

What’s in the News for EDP Renewables

- EDP Renewables has a planned corporate action described as a 1 to 8.06452 stock split or significant stock dividend, scheduled for May 12, 2026, according to Key Developments data.

- The 1 to 8.06452 ratio indicates that each existing share is set to convert into slightly more than 8 shares, with the event categorized under Stock Splits & Significant Stock Dividends in company filings.

- Investors in EDP Renewables may want to monitor upcoming company communications around this event for details on how the split or stock dividend will be implemented and any related timetable confirmations.

Valuation Changes for EDP Renewables

- Fair Value has been revised slightly higher from €14.36 to about €14.73 per share, reflecting a modest uplift in the updated model.

- The Discount Rate has been adjusted up from roughly 9.02% to about 9.22%, implying a slightly higher required return on EDP Renewables' equity.

- Revenue Growth has been updated from about 9.99% to roughly 9.45%, pointing to a more measured long term euro revenue growth assumption.

- The Net Profit Margin has moved from around 20.42% to about 20.62%, indicating a small increase in expected profitability on future euro earnings.

- The Future P/E has been nudged higher from about 32.68x to roughly 33.88x, suggesting a slightly richer valuation multiple on expected earnings.

Key Takeaways

- Significant capacity additions in the US and strategic asset rotation are expected to boost future revenue and enhance earnings by consolidating value.

- Efficiency improvements and long-term PPAs with major tech firms are poised to enhance margins and ensure stable revenue growth.

- Declines in electricity prices and renewable generation shortfalls, combined with political and financial risks, threaten EDP Renováveis’ future profitability and revenue.

Catalysts

About EDP Renováveis- A renewable energy company, plans, constructs, operates, and maintains electricity power stations.

- EDPR's significant increase in capacity additions, particularly in the US solar projects, sets a strong foundation for future growth and is expected to boost revenue once these capacities are fully operational.

- The company's focus on efficiency improvements, resulting in a 7% year-on-year decline in core OpEx per average megawatt, is poised to enhance net margins by reducing operational costs.

- Significant demand growth for electricity in the US, driven by data centers, crypto mining, and industrial activities, indicates potential upward pressure on revenue as EDPR expands its capacity to meet this demand.

- EDPR's strategic asset rotation, including the acquisition of a minority stake in a European wind portfolio, aimed at reducing minority leakage and simplifying the portfolio, is expected to positively impact earnings through enhanced control and value consolidation.

- The strong demand and high prices for new PPAs, with 65% of agreements made with major tech companies, suggest robust future revenue growth from long-term contracts as the company capitalizes on stable cash flows amid fluctuating market prices.

EDP Renováveis Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming EDP Renewables's revenue will grow by 9.5% annually over the next 3 years.

- Analysts assume that profit margins will increase from 10.6% today to 20.6% in 3 years time.

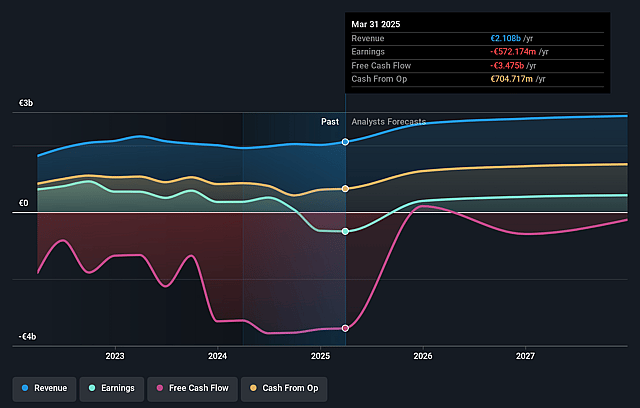

- Analysts expect earnings to reach €595.3 million (and earnings per share of €0.55) by about July 2029, up from €233.8 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting €767.7 million in earnings, and the most bearish expecting €487.7 million.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 33.9x on those 2029 earnings, down from 62.6x today. This future PE is lower than the current PE for the GB Renewable Energy industry at 62.1x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.22%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- The company has suffered a decrease in average selling prices due to lower electricity prices in Iberia, which could negatively impact future revenues.

- The renewable generation resources have been below expectations, especially in Brazil, impacting total renewable generation growth and future revenue forecasts.

- There is uncertainty around the U.S. political climate following the election results, which may cause policy changes that could impact the company's growth efforts and future earnings.

- Lower capital gains from asset rotations year-on-year have affected net profit despite top-line growth efforts, raising concerns about future profitability.

- Financial exposure to projects in countries like Colombia remains a risk; significant delays and slow progress in negotiations could impact future earnings and debt levels.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of €14.73 for EDP Renewables based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of €17.5, and the most bearish reporting a price target of just €9.5.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be €2.9 billion, earnings will come to €595.3 million, and it would be trading on a PE ratio of 33.9x, assuming you use a discount rate of 9.2%.

- Given the current share price of €13.92, the analyst price target of €14.73 is 5.5% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on EDP Renewables?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.