Last Update 07 Jun 26

Fair value Increased 0.34%SKA B: US Transport Wins And Penn Project Will Support Upside Potential

Analysts have raised their Skanska price target slightly to SEK 277.50 from SEK 276.57, citing updated assumptions around revenue growth, profit margins and a modestly lower future P/E multiple following recent bullish Street research.

What's in the News

- Penn Transformation Partners, a consortium including Skanska, was chosen as preferred bidder to act as Master Developer for the New York Penn Station Transformation Project. This highlights Skanska's role in large scale US transport infrastructure (source: Penn Station Transformation Project announcement).

- A joint venture of Skanska, Traylor Bros and Walsh Construction won a US$1.02b subway extension project in New York City, adding another sizeable US transit contract to Skanska's project portfolio (source: Punch List news report).

- Skanska, together with Halmar in Penn Transformation Partners, can now enter exclusive negotiations with Amtrak to finalize a predevelopment agreement for Penn Station. The agreement covers contract negotiations, design and preconstruction activities through 2027.

- The company secured a US$1.29b Hudson Tunnel Project Package 1C contract in a joint venture, with Skanska's share at US$363m, about SEK 3.4b, for new rail tunnels under the Hudson River between New Jersey and Manhattan.

- Skanska signed a SEK 400m agreement with Region Gotland to rebuild the Visby water treatment plant in Sweden. This long term project is focused on water security and system resilience, with work running through 2028.

Valuation Changes

- Fair Value: SEK 277.50 vs SEK 276.57, a slight upward adjustment in the target level used in the model.

- Discount Rate: 7.38% vs 6.98%, a modest increase in the required return assumption applied to future cash flows.

- Revenue Growth: 6.14% vs 4.71%, a higher SEK revenue growth assumption built into the forecasts.

- Net Profit Margin: 4.49% vs 4.34%, a small uplift in expected profitability on future SEK revenues.

- Future P/E: 15.58x vs 16.16x, a slightly lower valuation multiple applied to the stock in the outer year assumptions.

Key Takeaways

- Strong order backlog, favorable market trends, and alignment with public investments position Skanska for sustained revenue and earnings growth across geographies.

- Emphasis on ESG leadership, selective project focus, and resilient financial health enhance margins, stability, and shareholder value despite regional market fluctuations.

- Weak property markets, delayed asset sales, higher restructuring costs, and industry risks threaten Skanska's margins, earnings stability, and ability to generate reliable cash flow.

Catalysts

About Skanska- Operates as a construction and project development company in the Nordics, Europe, and the United States.

- Skanska's record-high order backlog (19 months of production, SEK 268 billion) and strong book-to-bill ratios (>100% across all geographies) position the company to benefit from sustained government infrastructure spending, especially in the US and Europe, supporting future revenue growth.

- The company is seeing robust demand and improved outlooks in key markets (Swedish civil, Central European residential), which are driven by continued urbanization, population growth, and increased public investments in defense, energy, and water infrastructure, laying the groundwork for mid

- and long-term earnings expansion.

- Skanska's focus on high-quality, sustainable (LEED/green) projects and a strong track record on decarbonization (62% emissions reduction since 2015) aligns it with rising ESG standards, positioning it to capture higher-margin projects as green building becomes increasingly mandated-supporting both revenue and net margin improvement.

- Healthy cash flow, a strong balance sheet (net cash, 37% equity ratio), and prudent project selection enable Skanska to remain resilient in volatile markets, invest in technology, and return capital to shareholders, providing a buffer and potential for increased shareholder returns.

- Despite weak Nordic residential markets, Skanska has shown flexibility and selectivity-emphasizing higher-margin Central European projects and maintaining a solid pipeline-allowing for operational recovery in softer regions and supporting the stability of group-wide margins and earnings.

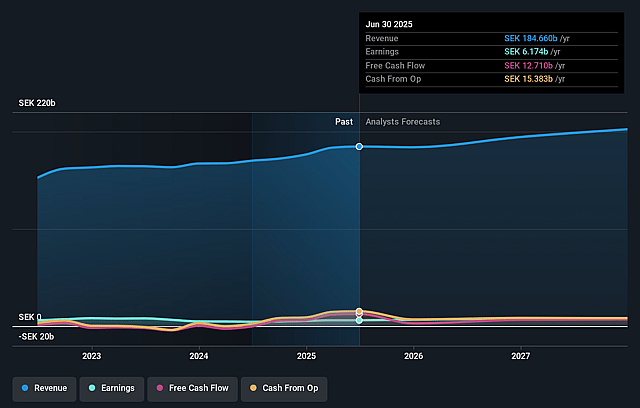

Skanska Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Skanska's revenue will grow by 6.1% annually over the next 3 years.

- Analysts assume that profit margins will increase from 3.3% today to 4.5% in 3 years time.

- Analysts expect earnings to reach SEK 9.2 billion (and earnings per share of SEK 20.49) by about June 2029, up from SEK 5.7 billion today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 15.6x on those 2029 earnings, down from 17.7x today. This future PE is lower than the current PE for the GB Construction industry at 18.3x.

- Analysts expect the number of shares outstanding to grow by 0.4% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.38%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Persistent weakness and slow recovery in the Nordic residential and commercial property markets, driven by low consumer confidence and broader macroeconomic uncertainties, could continue to depress volumes and margins in these core geographies, impacting overall revenue growth and earnings.

- The continued hesitancy and lack of transactions in the U.S. commercial property divestment market-primarily due to sustained high long-term interest rates-may delay planned asset sales, limiting Skanska's ability to recycle capital efficiently and suppressing earnings from property development.

- Elevated investment and restructuring costs, particularly those related to IT transformation and outsourcing of infrastructure, are causing central expenses to rise, potentially eroding net margins and limiting free cash flow available for dividends or reinvestment.

- The project development segment is currently in a net divestment cycle, and with a shallow transaction market and lumpy sales profile, there is heightened risk of irregular revenue recognition and increased earnings volatility over the medium term.

- Beyond company-specific execution, ongoing industry-wide risks such as construction labor shortages and potential cost inflation from regulatory demands or material prices could squeeze margins on both existing backlog and future projects, placing downward pressure on operating income and profitability.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of SEK277.5 for Skanska based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of SEK300.0, and the most bearish reporting a price target of just SEK240.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be SEK206.0 billion, earnings will come to SEK9.2 billion, and it would be trading on a PE ratio of 15.6x, assuming you use a discount rate of 7.4%.

- Given the current share price of SEK245.2, the analyst price target of SEK277.5 is 11.6% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Skanska?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.