Last Update 07 Jun 26

MRU: Succession Plan And Buybacks Will Balance Labour And Execution Risks

Metro's analyst price targets have been trimmed by CA$2 to CA$7 across several firms, with analysts citing updated assumptions on discount rates and future P/E multiples as they revisit their valuation work on the stock.

Analyst Commentary

Recent Street research has focused on reworking discounted cash flow assumptions and target P/E multiples for Metro, which has led to the CA$2 to CA$7 trims in price targets across several firms.

Bullish Takeaways

- Bullish analysts still see enough support in Metro's earnings profile to maintain coverage and publish updated targets rather than stepping away from the stock entirely.

- Revised models suggest that even with lower targets, analysts continue to assign value to Metro's ability to execute on its core operations, instead of signaling a breakdown in the underlying thesis.

- The spread in target cuts, from CA$2 to CA$7, indicates that some bullish analysts view the change in valuation assumptions as more of a calibration to updated discount rates and P/E inputs rather than a shift in how they view the business.

- By adjusting assumptions now, bullish analysts position their targets so that any improvement in execution or earnings quality can feed directly into future upside revisions without requiring a wholesale reset.

Bearish Takeaways

- Bearish analysts are signaling that prior valuation levels may have been too rich once they updated discount rates and future P/E multiples, which feeds into lower implied upside for the stock.

- The larger cuts, around CA$5 to CA$7, point to caution around Metro's ability to command the same valuation multiples that analysts previously used in their models.

- Lower targets imply that bearish analysts see less room for error in Metro's execution, with a tighter margin between current trading levels and their revised fair value ranges.

- By pulling back price targets across several firms at the same time, bearish analysts reinforce the idea that expectations for future growth and returns now sit on a more restrained footing.

What's in the News

- Metro announced that long-time President and CEO Eric La Flèche will retire effective September 27, 2026, at the end of the fiscal year. Current COO Marc Giroux is set to succeed him as CEO and join the Board on that date. Source: company announcement and recent press coverage.

- Following his retirement as CEO, Eric La Flèche is expected to become Chairman of the Board. Current Chairman Pierre Boivin will move to the role of Vice Chairman and Lead Director, keeping La Flèche involved at the Board level. Source: company announcement and recent press coverage.

- The company highlighted that this leadership change follows a multi year succession planning process. Metro pointed to Marc Giroux's long tenure since 2009 and his experience overseeing Québec and Ontario food divisions, supply chain, marketing, loyalty and digital initiatives. Source: company announcement.

- Metro reported that from November 25, 2025 to April 2, 2026, it repurchased 2,900,000 shares, representing 1.35% of its shares, for CA$279.8 million, completing the buyback tranche announced on November 25, 2025. Source: company announcement.

- The company is managing a strike affecting its produce distribution centre in Laval, as well as transportation and head office employees in Québec. It has activated a contingency plan while continuing negotiations with the union. Source: company announcement.

Valuation Changes

- Fair Value: CA$100.45 is unchanged, with the updated model keeping the same central estimate as before.

- Discount Rate: has fallen slightly from 6.61% to 6.46%, which increases the weight placed on future cash flows in the revised analysis.

- Revenue Growth: is kept effectively unchanged at about 3.50%, signaling no material adjustment to top line expectations in the model.

- Net Profit Margin: remains steady at roughly 4.52%, showing no shift in assumed profitability on each CA$ of revenue.

- Future P/E: has risen slightly from 21.38x to 21.84x, indicating a modestly higher multiple applied to Metro's projected earnings in the updated work.

Key Takeaways

- Store modernization, network expansion, and supply chain automation position Metro for sustained revenue growth and margin improvement as urbanization and health trends continue.

- Strong e-commerce momentum, private label outperformance, and effective loyalty programs support customer retention and earnings resilience in a competitive, inflationary market.

- Rising competition, inflationary pressures, and higher costs threaten Metro's margins and revenue stability, especially given geographic concentration and challenges in online and pharmacy segments.

Catalysts

About Metro- Through its subsidiaries, operates as a retailer, franchisor, distributor, and manufacturer in the food and pharmaceutical sectors in Canada.

- The company's ongoing investments in store modernization and network expansion-including new store openings, major renovations, and upgrades-position Metro to capitalize on Canada's urbanization and population growth, supporting higher long-term sales volumes and top-line revenue growth.

- Robust growth in pharmacy same-store sales (5.5% in the quarter, with further tailwinds from increasing prescription and specialty medication demand) suggests Metro is well-placed to benefit from rising consumer focus on health and wellness, bolstering both revenue and premium-margin opportunities.

- Sustained improvements in supply chain automation and productivity at new and upgraded distribution centers are contributing to higher gross margins and are expected to continue supporting further net margin expansion as efficiencies mature and more products move through automated systems.

- Strong momentum in e-commerce and online sales (up 14% in the quarter) and expansion of home delivery and click-and-collect partnerships (including a recent agreement with DoorDash) demonstrate that Metro is leveraging digital and omnichannel capabilities to drive customer retention and incremental revenue growth, as shopping behaviors shift online over time.

- Continued outperformance of private label sales versus national brands, along with increased promotional activity and customer loyalty program engagement, is likely to support gross margin resilience and protect earnings amid a highly competitive and inflationary market environment.

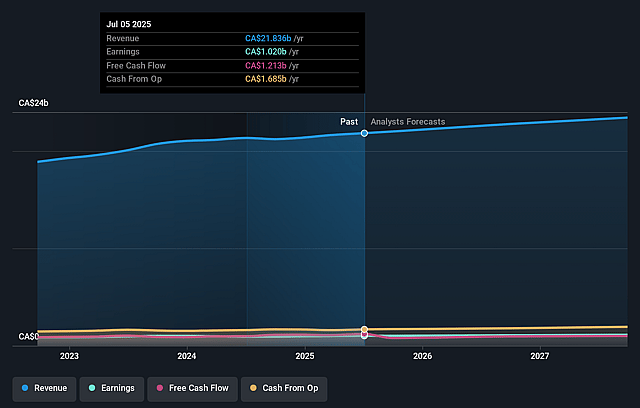

Metro Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Metro's revenue will grow by 3.5% annually over the next 3 years.

- Analysts assume that profit margins will increase from 4.4% today to 4.5% in 3 years time.

- Analysts expect earnings to reach CA$1.1 billion (and earnings per share of CA$5.56) by about June 2029, up from CA$983.7 million today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 21.9x on those 2029 earnings, up from 19.8x today. This future PE is greater than the current PE for the CA Consumer Retailing industry at 19.9x.

- Analysts expect the number of shares outstanding to decline by 2.01% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.46%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Intensifying competition from discount grocers and increased promotional activity, especially in Ontario, may lead to price wars and margin compression, directly challenging Metro's ability to grow revenues and maintain net margins.

- Acceleration of inflation in certain commodity categories (notably meat) and new tariffs are prompting more vendors to seek price increases, raising Metro's cost of goods and pressuring gross margins if those costs cannot be fully passed on to consumers.

- Elevated and rising SG&A expenses from recurring costs tied to new automated distribution centers and the rapid shift to online/third-party delivery partnerships could compress operating margins, especially if e-commerce growth requires higher-than-expected capital outlays with uncertain near-term profitability.

- Metro's high geographic concentration in Quebec and Ontario exposes it to regional economic downturns, competitive threats from new discount banner expansions, and demographic shifts that could lead to more volatile revenues and earnings.

- The shift towards generic pharmaceuticals (particularly pending Ozempic patent expiries) may dilute Metro's pharmacy margins, as distribution fees on generics are lower, posing a risk to long-term earnings growth in this segment.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of CA$100.45 for Metro based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of CA$112.0, and the most bearish reporting a price target of just CA$85.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be CA$24.6 billion, earnings will come to CA$1.1 billion, and it would be trading on a PE ratio of 21.9x, assuming you use a discount rate of 6.5%.

- Given the current share price of CA$92.64, the analyst price target of CA$100.45 is 7.8% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Metro?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.