Last Update 16 Jun 26

Fair value Increased 0.87%AKZA: Merger Execution And Downgrade Reset Will Shape Fairly Valued Shares

Akzo Nobel's analyst price target has inched up to about €61.70 from roughly €61.18, as analysts factor in slightly higher fair value estimates and updated assumptions for discount rate, revenue growth and P/E. This follows mixed recent research that includes a resumed Buy rating and several price target cuts and downgrades.

Analyst Commentary

Recent research on Akzo Nobel reflects a split view, with some analysts pointing to upside potential and others focusing on execution risk and valuation constraints around the current price target range.

Bullish Takeaways

- Bullish analysts see the resumed Buy rating and €61 price target as consistent with the current blended target near €61.70. They indicate that their fair value work still supports the existing valuation framework.

- The positive view on a potential Akzo and Axalta merger is framed as a possible catalyst for scale, portfolio breadth and earnings mix. Bullish analysts connect this to support for current P/E assumptions.

- Supportive research implies confidence that management can execute on integration and cost plans well enough to justify slightly higher fair value estimates used in target price models.

- Pro merger analysts highlight the opportunity for Akzo Nobel to improve competitive positioning in key coatings segments. They view this as important for sustaining revenue assumptions embedded in their targets.

Bearish Takeaways

- Bearish analysts have recently cut their price targets. This signals concerns that previous valuation assumptions, including growth and discount rate inputs, may have been too optimistic for Akzo Nobel at current levels.

- Several downgrades point to execution risk around delivering on earnings and integration plans, with caution that any missteps could put pressure on the P/E multiples used in target setting.

- The series of target reductions indicates some hesitation about near term growth visibility, prompting more conservative models on revenue and margin progression for the stock.

- Downgrades from larger global brokers, including Goldman Sachs, underscore the risk that Akzo Nobel may need more proof points on consistent delivery before some analysts are comfortable with higher valuation multiples.

What’s in the News for Akzo Nobel

- Akzo Nobel rejected two all-cash takeover bids from Nippon Paint Holdings and Sherwin-Williams, after its boards concluded the offers were not superior to the planned merger with Axalta Coating Systems Ltd. (source: recent news reports)

- Following the rejection of the takeover bids, Akzo Nobel shares fell as much as 22%. This was reported as the largest one-day decline in the company’s history and was accompanied by downgrades and target price cuts from banks including Citi, Deutsche Bank, Barclays and Berenberg, with one cited move from €62.59 to €61.18. (source: recent news reports)

- Nippon Paint Holdings and Sherwin-Williams had submitted a conditional, non-binding proposal valued at €12.5b, or €73 in cash per Akzo Nobel share. The parties cancelled the acquisition on May 1, 2026 after the Akzo Nobel boards decided the proposal did not qualify as a superior proposal under the Axalta merger agreement. (source: company event filing)

- Akzo Nobel continues to pursue its planned merger with Axalta. The transaction remains subject to regulatory approvals and shareholder processes as set out in the existing merger agreement. (source: recent news reports and company event filing)

- Akzo Nobel successfully issued a €750m bond, to be listed on the Luxembourg Stock Exchange with settlement on June 16, 2026 and maturity on June 16, 2029, to support financing for the proposed Axalta transaction. Further details are expected to be filed with the U.S. Securities and Exchange Commission. (source: company announcement)

Valuation Changes for Akzo Nobel

- Fair Value: revised slightly higher from €61.18 to about €61.71 per share, a move of roughly 0.9%.

- Discount Rate: nudged up from about 6.47% to roughly 6.53%, indicating a modestly higher required return in the updated models.

- Revenue Growth: adjusted from about 1.97% to roughly 2.00%, a very small upward change in long term growth assumptions in euro terms.

- Net Profit Margin: moved marginally from about 7.29% to roughly 7.28%, a very slight reduction in projected profitability on future € earnings.

- Future P/E: inched up from roughly 16.54x to about 16.71x, reflecting a small change in how the Akzo Nobel stock is valued in forward earnings terms.

Key Takeaways

- Focus on sustainable product innovation and strategic divestments is driving higher margins, premium pricing, and a sharper concentration on core segments.

- Operational efficiency, supply chain optimization, and emerging market momentum position the company for improved resilience and revenue growth.

- Weak demand in mature markets, currency volatility, price competition, and increased regulatory costs threaten sustained revenue growth and profitability for Akzo Nobel.

Catalysts

About Akzo Nobel- Produces and sells paints and coatings worldwide.

- The company is capitalizing on accelerating demand for sustainable and eco-friendly coatings, highlighted by their leadership position in low-VOC and sustainable product innovations, which are set to drive premium pricing and increase net margins as regulatory and consumer preferences shift further toward sustainability.

- Ongoing efficiency and digitization initiatives, with completed SG&A programs, five additional site closures, and further operational cost-saving opportunities identified, are expected to structurally lower operating expenses and enhance EBITDA margins over the coming quarters.

- Strategic divestment of non-core or subscale businesses, such as the high-multiple India sale (with both cash proceeds for deleveraging and share buybacks, plus an ongoing royalty stream), will sharpen the portfolio's focus on higher-margin, core segments, likely boosting return on invested capital and EPS.

- Improving service levels through investment in supply chain and manufacturing optimization (e.g., OTIF metrics) are poised to support resilience, share gains in key markets, and potential top-line growth as conditions in currently weak regions (like North America or Turkey) stabilize.

- Akzo Nobel's exposure to infrastructure growth and urbanization in emerging markets is gaining momentum-evidenced by a strongly rebounding China Decorative Paints business and expected further recovery in LatAm-which positions revenue for upside as these long-term demand drivers play out.

Akzo Nobel Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Akzo Nobel's revenue will grow by 2.0% annually over the next 3 years.

- Analysts assume that profit margins will increase from 6.3% today to 7.3% in 3 years time.

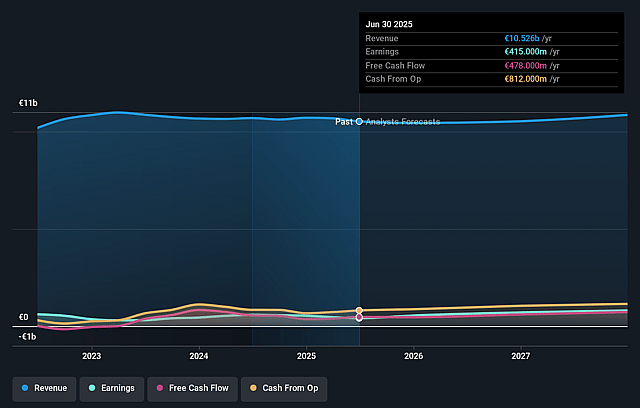

- Analysts expect earnings to reach €767.8 million (and earnings per share of €4.53) by about June 2029, up from €622.0 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting €869.4 million in earnings, and the most bearish expecting €633.8 million.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 16.7x on those 2029 earnings, up from 16.1x today. This future PE is greater than the current PE for the GB Chemicals industry at 16.2x.

- Analysts expect the number of shares outstanding to grow by 0.15% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.53%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Persistent volume declines in mature markets such as North America and Southern Europe, combined with ongoing market uncertainty and weak end-market demand, may constrain long-term revenue growth despite operational improvements.

- Currency volatility and prolonged foreign exchange headwinds, particularly the depreciation of the Turkish lira, Brazilian real, and related emerging market currencies, could erode revenue and profit margins as the company depends on multiple geographies for sales.

- Industry-wide price competition and difficulty extracting positive pricing in certain Coatings segments (such as Powder), amid ongoing commoditization and aggressive tactics by competitors, risk compressing net margins over time.

- The ongoing strategic shift involving portfolio disposals (e.g., India) and cost-cutting programs could limit future organic growth and reduce scale, while any failure to achieve meaningful top-line expansion in retained/core businesses may weigh on long-term earnings.

- Regulatory and geopolitical risks-including trade barriers, further regionalization, and higher compliance costs for environmental and chemical regulations-may increase ongoing SG&A and operational costs, pressuring both margins and free cash flow.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of €61.71 for Akzo Nobel based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of €73.0, and the most bearish reporting a price target of just €50.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be €10.5 billion, earnings will come to €767.8 million, and it would be trading on a PE ratio of 16.7x, assuming you use a discount rate of 6.5%.

- Given the current share price of €58.6, the analyst price target of €61.71 is 5.0% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Akzo Nobel?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.