Last Update 25 Jun 26

Fair value Increased 3.10%NWH: Record Results And Expanded Services Will Support Measured 2026 Outlook

Analysts have slightly raised their price target for NRW Holdings to A$6.98 from A$6.77, citing updated assumptions around revenue growth, profit margins and the P/E multiple used in their forecasts.

What's in the News

- NRW Holdings reported record first half FY2026 results, with revenue up 19.5%, underlying EBITDA up 36.5% and underlying NPAT up 42.3% compared with the prior period. Source: Recent H1 FY2026 results coverage.

- Management upgraded FY2026 revenue guidance from A$3.42b to A$3.77b, with about 90% of the revised guidance reported as secured in the current order book. Source: Company guidance update.

- The acquisition of Fredon Industries in September 2025 expanded NRW Holdings' service offering to electrical, mechanical, instrumentation and technology services, and the business has secured additional contracts following the deal. Source: Acquisition and integration commentary.

- Despite these developments, some commentary suggests NRW Holdings is trading below certain estimates of fair value. This has drawn interest from investors who see potential value in the stock. Source: Valuation-focused news coverage.

- NRW subsidiary Primero advanced commercialisation efforts for its proprietary ALi atmospheric leach process after PMET Resources selected it as the preferred lithium processing route for further study, with bench-scale testing producing 99.8% battery grade lithium carbonate. Source: ALi process assessment news.

Valuation Changes for NRW Holdings

- Fair Value: The A$ fair value estimate increased from A$6.77 to A$6.98, an upward adjustment of about 3.1%.

- Discount Rate: The discount rate remained effectively unchanged at 9.01%, reflecting only a very small technical adjustment.

- Revenue Growth: The assumed A$ revenue growth rate rose from 9.73% to 10.05%, a modest uplift of around 0.3 percentage points.

- Net Profit Margin: The assumed net profit margin increased from 4.41% to 4.44%, indicating a slight improvement in projected profitability for NRW Holdings.

- Future P/E: The future P/E multiple used in the model moved from 19.49x to 19.77x, a small increase in the valuation multiple applied.

Key Takeaways

- Strong project pipeline, infrastructure investment, and diversification boost revenue visibility and margin stability across mining and civil operations.

- Enhanced ESG focus and strategic acquisitions position NRW Holdings for sustainable earnings growth and successful contract retention.

- High exposure to weather, client insolvency, tight margins, sector reliance, and elevated financial risk threaten long-term profitability and resilience.

Catalysts

About NRW Holdings- Through its subsidiaries, provides diversified contract services to the resources and infrastructure sectors in Australia.

- The significant expansion in the project pipeline and order book, underpinned by ongoing global demand for critical minerals such as lithium and copper for electrification and energy transition, positions NRW Holdings to capture robust future revenue growth as mining investment in Australia accelerates.

- Growing public infrastructure spending in Western Australia and Queensland, driven by acute infrastructure needs and government stimulus, is fuelling a record near-term tender pipeline and strong revenue visibility, supporting top-line growth and margin resilience in the Civil division.

- Investments in safety, environmental performance, and Indigenous engagement strengthen NRW Holdings' profile as a preferred contractor for miners and government agencies facing heightened ESG standards, enhancing prospects for contract wins and supporting long-term revenue growth.

- Recent diversification into adjacent infrastructure markets and the expansion of recurring services offerings (e.g., maintenance, products, and parts) are expected to reduce earnings volatility and improve EBITDA/net margin stability over time.

- Strategic M&A (e.g., HSE, South Walker Creek acquisition) and major contract extensions are expected to drive step-changes in run-rate revenues and operational leverage, contributing to sustainable earnings growth as weather impacts normalise.

NRW Holdings Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

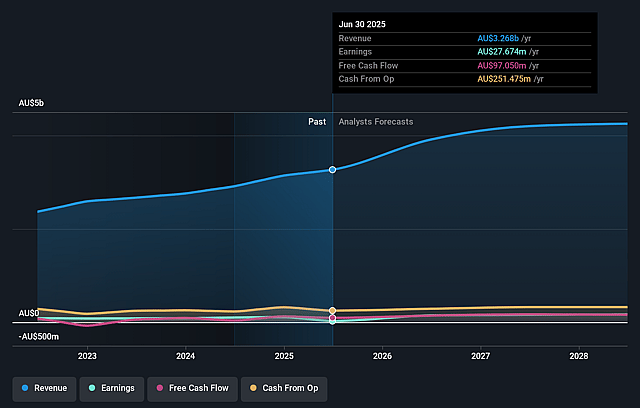

- Analysts are assuming NRW Holdings's revenue will grow by 10.1% annually over the next 3 years.

- Analysts assume that profit margins will increase from 1.4% today to 4.4% in 3 years time.

- Analysts expect earnings to reach A$212.6 million (and earnings per share of A$0.46) by about June 2029, up from A$48.8 million today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 19.8x on those 2029 earnings, down from 67.8x today. This future PE is lower than the current PE for the AU Construction industry at 27.0x.

- Analysts expect the number of shares outstanding to grow by 0.46% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.01%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- The company's earnings are highly exposed to weather-related disruptions, as demonstrated by the significantly reduced Mining margins due to above-average rainfall in Queensland, highlighting long-term climate risks that could continue to negatively impact revenue and earnings volatility.

- NRW Holdings faced material exposure to client insolvency and government intervention, as seen in the OneSteel administration and resulting receivable impairment, which underscores ongoing risks of revenue concentration and credit losses from large contracts, directly impacting profitability and working capital.

- Margin pressures remain elevated due to competitive project bidding and a greater earnings contribution from lower-margin Civil and MET businesses, indicating that even with higher revenue, net margins and return on invested capital may be structurally constrained in the long term.

- Ongoing reliance on the resources sector for growth, particularly coal and iron ore projects, leaves NRW vulnerable to secular declines in traditional mining investment stemming from global decarbonization and energy transition efforts, potentially eroding future contract opportunities and long-term revenue growth.

- Increased requirements for capital management (e.g., bank debt drawdowns, elevated equipment financing, and acquisition costs) heighten financial risk and may constrain future cash flows or dividends, particularly if market conditions become less favorable or if strategic projects fail to deliver anticipated returns.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of A$6.98 for NRW Holdings based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of A$8.1, and the most bearish reporting a price target of just A$6.3.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be A$4.8 billion, earnings will come to A$212.6 million, and it would be trading on a PE ratio of 19.8x, assuming you use a discount rate of 9.0%.

- Given the current share price of A$7.2, the analyst price target of A$6.98 is 3.2% lower. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on NRW Holdings?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.