Last Update 29 Jul 26

Fair value Increased 31%500463: AI Alliances And Planned Fundraising Will Support Future Upside

Analysts have reset their price target on Black Box from ₹837.5 to ₹1,100.5, citing updated assumptions around discount rate, revenue growth, profit margins and a higher future P/E multiple as the key drivers of this change.

What’s in the News for Black Box

- Black Box entered a strategic alliance with AIONOS, an AI native enterprise technology company, to support AI related transformation for enterprises across digital infrastructure, AI platforms, and industry focused solutions, covering India, North America, EMEA, and APAC. Source: Key Developments.

- The alliance with AIONOS targets India’s Global Capability Centre ecosystem, with an emphasis on AI ready infrastructure, enterprise grade AI deployments, and integrated operations linked to global parent organizations. Source: Key Developments.

- Black Box Products FZE, a step down subsidiary of Black Box, incorporated Black Box Technologies Company in Saudi Arabia as an overseas subsidiary. Source: Key Developments.

- Black Box scheduled a Board Meeting on May 26, 2026 to consider audited standalone and consolidated financial results for the year ended March 31, 2026, a potential final dividend, and possible fund raising during FY2026-27, subject to approvals. Source: Key Developments.

- Black Box called a Special or Extraordinary Shareholders Meeting for June 19, 2026 at 11:00 Indian Standard Time to consider authorisation to raise up to ₹2,500,000,000 in securities, higher borrowing limits, and creation of security interests over company undertakings under section 180(1)(a) of the Companies Act, 2013. Source: Key Developments.

Valuation Changes

- Fair Value: The assessed fair value for Black Box is now ₹1,100.5 compared with the earlier ₹837.5, representing a sizeable upward revision.

- Discount Rate: The discount rate assumption has risen slightly from 15.37% to 15.91%, indicating a modestly higher required return in the model.

- Revenue Growth: The long term revenue growth assumption has been reset from 26.30% to 20.77%, reflecting a more measured growth outlook in the valuation framework.

- Net Profit Margin: The net profit margin input has moved from 5.37% to 5.88%, suggesting a slightly stronger profitability assumption for Black Box over the forecast period.

- Future P/E: The future P/E multiple has been raised from 38.0x to 52.9x, which represents a significant uplift in the valuation multiple applied to projected earnings.

Key Takeaways

- Strategic shift to larger, integrated contracts and industry verticals improves revenue visibility, recurring earnings potential, and strengthens competitive positioning in digital infrastructure.

- Operational focus on high-value customers, leadership changes, and cross-selling enhance profitability and position the company for long-term growth in emerging tech areas.

- Margin pressure, earnings volatility, and stagnant growth risk are heightened by intense competition, reliance on large contracts, slow service transformation, macroeconomic headwinds, and weak innovation investment.

Catalysts

About Black Box- Provides information and communications technology solutions in India, the United States, Ireland, the United Kingdom and internationally.

- Strong order book momentum and ongoing shift to larger, high-value contracts (including wins in data centers, financial services, OTT, and public sector) support robust revenue visibility and backlog growth; this positions the company to benefit as enterprises accelerate digital adoption and infrastructure investments, likely driving topline growth in upcoming quarters.

- Intensifying focus on providing integrated solutions to hyperscalers and global enterprises-coupled with increased engagement in high-growth verticals like data centers, healthcare, and government-aligns with industry-wide migration to cloud and hybrid environments, offering significant headroom for recurring revenues and earnings expansion through both project and annuity contracts.

- Implementation of an experienced leadership team and a new go-to-market strategy is resulting in higher win rates, greater customer wallet share, and improved cross-selling across solutions such as connectivity, cybersecurity, and managed services, which should drive both revenue growth and gradual net margin improvement.

- Ongoing rationalization of the long-tail customer base, with a pivot to focusing on fewer, higher-value customers, is streamlining operations and reducing SG&A costs, setting up better operating leverage and supporting sustained improvements in EBITDA margin.

- Long-term opportunities in AI-led infrastructure refresh, proliferation of IoT and edge computing, and 5G expansion will require significant new deployments and retrofits of IT architecture; Black Box's global presence and rising order pipeline in these domains make it well-positioned to capture incremental demand, underpinning future revenue growth and backlog expansion.

Black Box Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

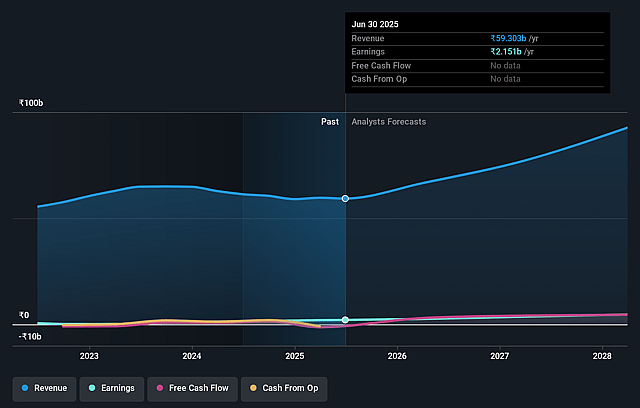

- Analysts are assuming Black Box's revenue will grow by 20.8% annually over the next 3 years.

- Analysts assume that profit margins will increase from 3.4% today to 5.9% in 3 years time.

- Analysts expect earnings to reach ₹6.5 billion (and earnings per share of ₹37.6) by about July 2029, up from ₹2.2 billion today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 53.1x on those 2029 earnings, down from 63.2x today. This future PE is greater than the current PE for the IN IT industry at 22.9x.

- Analysts expect the number of shares outstanding to grow by 4.54% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 15.91%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Intensifying competition and price pressure in core IT infrastructure and network deployment services, driven by the commoditization of offerings and the proliferation of global managed services providers, could compress Black Box's service margins and top-line revenue growth in the long term.

- Heavy reliance on landing large, complex contracts and a shrinking long-tail client base increases earnings volatility risk: delays, cancellations, or failures to win such deals can create sharp fluctuations in quarterly revenues and cash flows, undermining long-term earnings stability.

- Slower-than-expected execution of transformation from traditional hardware-based solutions to higher-margin managed or software-defined services-due to extended project lead times, lagging Day 2/support annuity, and the legacy orientation of the backlog-may restrict net margin expansion and limit sustainable revenue growth.

- Prolonged or recurring macroeconomic uncertainties (such as tariffs, supply chain disruptions, client capital expenditure delays, or currency fluctuations) can stall project execution and revenue recognition, resulting in unpredictable quarterly financials and long-term revenue headwinds.

- Insufficient investment in innovation, R&D, and co-innovation/IP partnerships with hyperscalers and strategic clients risks Black Box's ability to capture edge computing, AI infrastructure, or new cloud-based opportunities-potentially eroding market share and pressuring both margins and overall earnings in the face of evolving secular technology trends.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of ₹1100.5 for Black Box based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be ₹111.4 billion, earnings will come to ₹6.5 billion, and it would be trading on a PE ratio of 53.1x, assuming you use a discount rate of 15.9%.

- Given the current share price of ₹740.15, the analyst price target of ₹1100.5 is 32.7% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Black Box?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.