Last Update 06 Jun 26

Fair value Decreased 21%SKIN: Future Returns Will Hinge On Delivering FY26 EBITDA Under Competitive Pressure

Narrative Update on SkinHealth Systems

Analysts have trimmed the SkinHealth Systems price target from $2.50 to $2.00, citing updated models that factor in recent earnings, ongoing competitive pressure at the lower end of the market, and adjusted long term assumptions for revenue growth, profit margins, discount rate and future P/E.

Analyst Commentary

Recent research commentary around SkinHealth Systems centers on recalibrated price targets, revised models following quarterly updates, and an ongoing focus on how the company manages competitive pressure at the lower end of the market.

Bullish analysts and cautious analysts are working off the same information, but they are emphasizing different aspects of execution, growth expectations and valuation support.

Bullish Takeaways

- Bullish analysts highlight that even with a lower price target of US$2.00, there is still room for potential upside if management delivers on its updated long term assumptions for revenue growth, margins and P/E.

- Some argue that recent quarterly results, while mixed, were solid enough versus expectations to justify maintaining exposure, especially if the company can keep costs in check and protect profitability.

- There is also attention on longer term EBITDA guidance, which, if achieved, could support a valuation that is above current trading levels, even after the reduced target.

- Bullish analysts point to the possibility that improved execution with distributors and better product mix could help offset some pricing and volume pressure from low cost competitors.

Bearish Takeaways

- Bearish analysts focus on the step down in price targets, which they see as a signal that prior growth and profitability expectations were too optimistic relative to the latest earnings and guidance.

- They remain concerned that competition from knock offs and scaled down devices for cost sensitive providers may limit pricing power and weigh on margins if SkinHealth Systems needs to discount more aggressively.

- There is caution around softer early quarter trends tied to broader macro pressure on distributor ordering, which some see as a potential drag on near term revenue visibility.

- Bearish analysts also question how quickly management can execute on its long term plan, given the need to balance investment in growth with tighter assumptions for discount rates and future P/E multiples.

What’s in the News

- SkinHealth Systems received a Nasdaq notice on May 8, 2026 that its Class A common stock has been below the US$1.00 minimum bid for 30 consecutive business days. This triggered a 180 day compliance window to restore the bid price to at least US$1.00 for a minimum of ten consecutive business days. The company indicated it will monitor the share price and consider options to address the deficiency. (Source: Nasdaq notice summary)

- The company refreshed its Keravive scalp treatment as HydraScalp with Keravive, a professional in office scalp treatment that uses Hydrafacial Vortex Fusion Technology and biomimetic peptides. The update includes new Purify and Nourish tips intended to improve precision, provider workflow and consistency of visible scalp and hair results, supported by clinical findings on hair fullness, scalp hydration and appearance. (Source: Product announcement)

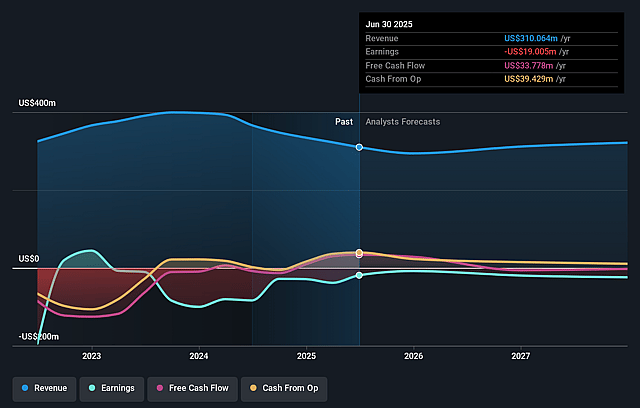

- SkinHealth Systems revised earnings guidance for the second quarter of 2026, indicating expected net sales of US$72 million to US$77 million. For full year 2026, the company indicated expected net sales of US$280 million to US$295 million. (Source: Company guidance)

- On April 22, 2026, The Beauty Health Company changed its name to SkinHealth Systems Inc., accompanied by a restated certificate of incorporation and updated bylaws that reflect the new name and make several governance and administrative updates. (Source: Corporate filings)

- The company reported that from October 1, 2025 to December 31, 2025 it repurchased 0 shares. Cumulatively, it completed the repurchase of 10,350,749 shares, or 7.81% of its stock, for US$30.18 million under the buyback announced on September 12, 2023. (Source: Buyback update)

Valuation Changes

- Fair Value: Updated fair value has fallen roughly 21% from $1.69 to $1.34, reflecting the revised modeling inputs.

- Discount Rate: The discount rate has risen slightly from 12.33% to 12.46%, indicating a modestly higher required return in the updated analysis.

- Revenue Growth: Revenue growth assumptions have fallen from 2.30% to 1.79%, pointing to more muted top line expectations.

- Net Profit Margin: Profit margin assumptions have risen from 6.16% to 8.12%, reflecting expectations for a higher share of revenue translating into earnings.

- Future P/E: The future P/E multiple has fallen from 16.08x to 10.39x, implying a lower valuation multiple applied to expected earnings.

Key Takeaways

- Overreliance on premium offerings and Hydrafacial leaves the company vulnerable to shifting consumer trends, economic pressures, and evolving competitive dynamics.

- Rising regulatory and sustainability demands may increase costs and suppress margins, hampering long-term revenue and earnings growth.

- High recurring revenue from consumables, successful product innovation, expanding global reach, strong operational discipline, and industry-leading brand loyalty support sustainable growth and profitability.

Catalysts

About Beauty Health- Designs, develops, manufactures, markets, and sells esthetic technologies and products in the Americas, the Asia-Pacific, Europe, the Middle East, and Africa.

- Investor expectations may be too optimistic regarding the company's ability to maintain strong growth in premium beauty device and consumable sales, overlooking the risk that lower birth rates and an aging population in developed markets could stagnate or slow long-term demand for new discretionary beauty treatments, potentially capping future revenue growth.

- The stock could be overvalued if the current price reflects an assumption that Beauty Health will continue expanding its addressable market across all demographics, even though persistent economic inequality and macro pressures limit consumer spending on premium and elective beauty procedures, creating headwinds for both revenue and margin expansion.

- Increased global scrutiny on environmental impacts and regulatory requirements-especially as governments raise standards on product safety, efficacy, and sustainability-may lead to higher operational costs, limiting margin improvements and potentially dampening demand, which would negatively impact net margins and earnings over time.

- A reliance on the Hydrafacial franchise for the majority of revenues increases the risk to top-line growth if consumer tastes evolve or if new at-home or digital skin health solutions reduce demand for in-office treatments, leading to revenue volatility and limiting the company's longer-term growth trajectory.

- Competitive threats from large multinational beauty companies and innovative indie brands investing in high-tech and personalized skincare could intensify, driving price pressures and eroding Beauty Health's market share, ultimately weighing on future revenue and profit growth.

Beauty Health Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming SkinHealth Systems's revenue will grow by 1.8% annually over the next 3 years.

- Analysts are not forecasting that SkinHealth Systems will become profitable in next 3 years. To represent the Analyst Price Target as a Future PE Valuation we will estimate SkinHealth Systems's profit margin will increase from -2.2% to the average US Personal Products industry of 8.1% in 3 years.

- If SkinHealth Systems's profit margin were to converge on the industry average, you could expect earnings to reach $25.4 million (and earnings per share of $0.18) by about June 2029, up from -$6.5 million today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 10.4x on those 2029 earnings, up from -12.0x today. This future PE is lower than the current PE for the US Personal Products industry at 17.3x.

- Analysts expect the number of shares outstanding to grow by 2.19% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 12.46%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Strong, growing recurring revenue from consumables: The company reported that over 70% of revenue now comes from consumables (razor-razor blade model), with year-over-year growth in Americas and EMEA, high loyalty among providers, and successful, clinically-backed product launches. This recurring, sticky revenue stream underpins gross margin expansion and earnings resilience.

- Successful innovation pipeline and launch cadence: The rapid launch and adoption of new boosters (e.g., HydraFillic with Pep9), planned introduction of backbar and skincare lines, and continued investment in clinically-validated innovation indicate robust product development that can drive both device utilization and consumables growth, positively impacting future revenue and margins.

- Expanding global footprint and diversified revenue: The installed base of devices has grown (35,000+ active devices), with ongoing international market penetration, double-digit consumables growth in EMEA, and strategic reorganization in China positioning the company for future stable sales and reduced overreliance on North America, supporting long-term revenue growth and earnings stability.

- Operational improvements and cost discipline: The company has delivered three consecutive quarters of exceeding revenue and adjusted EBITDA guidance, achieved a significant increase in gross margins (GAAP 62.8%, adjusted 65.9%), reduced operating expenses by nearly 18%, and managed inventory efficiently, resulting in improved profitability and potential for stronger net margins.

- Strong brand leadership and channel loyalty: HydraFacial remains one of the most in-demand, recognized treatments globally, driving high patient and provider engagement. The company excels in provider partnerships, boasts a high Net Promoter Score, and is rolling out strategic loyalty and engagement programs, which should boost customer lifetime value and support long-term recurring revenue and earnings visibility.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $1.34 for SkinHealth Systems based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $2.0, and the most bearish reporting a price target of just $1.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $312.3 million, earnings will come to $25.4 million, and it would be trading on a PE ratio of 10.4x, assuming you use a discount rate of 12.5%.

- Given the current share price of $0.61, the analyst price target of $1.34 is 54.7% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on SkinHealth Systems?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.