Catalysts

About CBIZ

CBIZ provides accounting, tax, advisory, benefits and insurance services to primarily mid market clients.

What are the underlying business or industry changes driving this perspective?

- Although the Marcum acquisition has created a much larger platform with year to date revenue of US$2.2b and a broader mid market client base, the integration plan still carries US$89 million of 2025 integration costs and additional 2026 costs that could limit the flow through of revenue into earnings if execution slips.

- Despite management highlighting stronger project based advisory demand and improved market conditions in the second half, these nonrecurring revenue streams remain sensitive to deal and project cycles, so any slowdown could weigh on revenue growth and restrain adjusted EBITDA expansion.

- While pricing in core accounting and tax is running at mid single digit rate increases that exceed inflation, rising competition for talent and the planned normalization of incentive compensation from unusually low 2025 levels could pressure total compensation and benefits and reduce net margins even if revenue continues to grow.

- Although investments in AI, data, offshoring in India and the Philippines, and a 60 person transformation team are aimed at improving efficiency, there is execution risk around adoption and process change that could delay expected productivity gains and keep adjusted EBITDA margin below potential.

- Despite a larger scale Financial Services segment with US$1.9b of year to date revenue and an updated synergy goal of US$50 million or more, pending real estate decisions in major metro markets and ongoing co location efforts mean some cost savings are still uncertain in timing, which could affect future operating margin and earnings visibility.

Assumptions

This narrative explores a more pessimistic perspective on CBIZ compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts. How have these above catalysts been quantified?

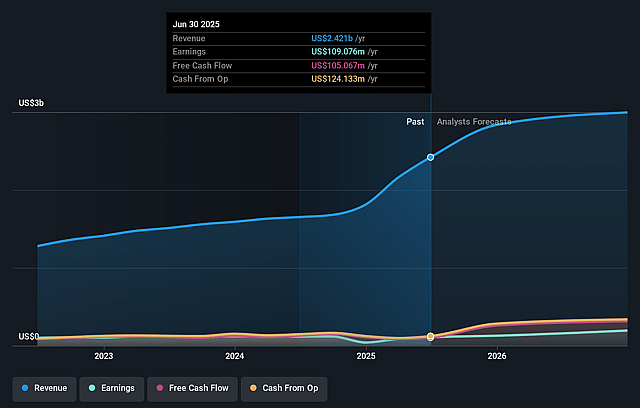

- The bearish analysts are assuming CBIZ's revenue will grow by 5.2% annually over the next 3 years.

- The bearish analysts assume that profit margins will increase from 3.9% today to 6.9% in 3 years time.

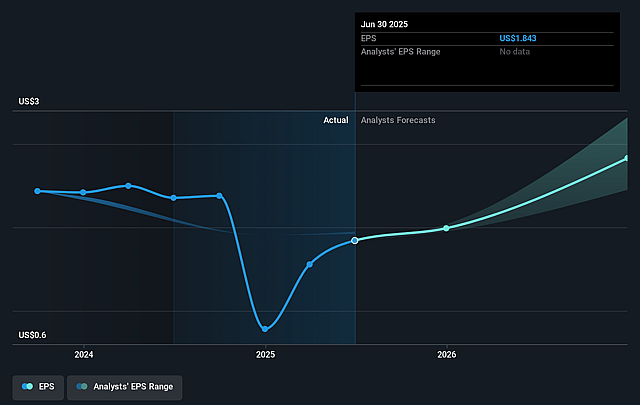

- The bearish analysts expect earnings to reach $213.5 million (and earnings per share of $3.77) by about January 2029, up from $104.1 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 19.8x on those 2029 earnings, down from 27.9x today. This future PE is lower than the current PE for the US Professional Services industry at 25.1x.

- The bearish analysts expect the number of shares outstanding to grow by 1.17% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.43%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?

- The Marcum integration plan includes US$89 million of 2025 integration costs and additional 2026 costs, and management has highlighted higher severance and future real estate actions. If integration drags on longer than planned or generates less than the US$50 million or more in targeted synergies, earnings and net margins could fall short of expectations and weigh on sentiment about long-term profitability.

- CBIZ is leaning heavily on long-term efficiency projects such as AI deployment, offshoring in India and the Philippines, and a 60 person transformation team. If adoption is slower than hoped or productivity gains are smaller than expected, operating expenses could stay elevated and limit improvement in adjusted EBITDA margin and earnings.

- A meaningful part of revenue depends on nonrecurring, project based advisory and M&A related work that is sensitive to deal cycles and client confidence. If market conditions weaken or rate cuts do not translate into sustained transaction activity, revenue growth could slow and reduce operating leverage into earnings.

- The company ended the quarter with approximately US$1.6b of net debt, higher interest expense of US$28 million in the quarter and a leverage target that may now extend to 2027. If cash flow is weaker than planned or refinancing costs remain elevated, more cash could be directed to debt service rather than growth initiatives, which would limit future earnings expansion.

- Management is prioritizing mid single digit pricing increases and significant investment in talent retention and incentive compensation. If competition for skilled professionals intensifies or clients resist ongoing price increases over time, total compensation and benefits could rise faster than revenue, putting pressure on net margins and adjusted EPS.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The assumed bearish price target for CBIZ is $60.0, which represents up to two standard deviations below the consensus price target of $81.0. This valuation is based on what can be assumed as the expectations of CBIZ's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $98.0, and the most bearish reporting a price target of just $60.0.

- In order for you to agree with the more bearish analyst cohort, you'd need to believe that by 2029, revenues will be $3.1 billion, earnings will come to $213.5 million, and it would be trading on a PE ratio of 19.8x, assuming you use a discount rate of 8.4%.

- Given the current share price of $54.24, the analyst price target of $60.0 is 9.6% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on CBIZ?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.