Last Update 07 Jun 26

EQBK: Earnings Quality And Capital Discipline Will Support Future Market Confidence

Analyst price targets for Equity Bancshares have shifted slightly, with recent research indicating a modest net change of about $1 as analysts weigh differing views on valuation drivers and earnings potential.

Analyst Commentary

Recent price target changes for Equity Bancshares point to mixed views on how much upside is left at current levels, even though the net shift is only about US$1. Bullish analysts and bearish analysts are reacting to the same set of fundamentals but are prioritizing different risks and opportunities.

Bullish Takeaways

- Bullish analysts see room for the stock to reflect stronger execution on core banking operations, which they view as not fully captured in prior targets.

- The US$1 upward adjustment is framed as a refinement rather than a major reset. This suggests these analysts think the company’s earnings profile can support slightly higher valuation multiples than previously assumed.

- Supportive commentary highlights confidence in management’s ability to keep returns and profitability aligned with peers, which underpins their willingness to raise estimated fair value.

- These analysts also point to potential for more consistent growth in fee and interest income over time, which they see as helpful for justifying a modest premium to earlier price assumptions.

Bearish Takeaways

- Bearish analysts use their US$1 reduction to signal that, in their view, the stock already reflects much of the accessible upside on current earnings expectations.

- They emphasize execution risk around maintaining margins and credit quality, which could limit how much investors are willing to pay relative to earnings and book value.

- Some of the more cautious commentary focuses on the possibility that growth in key revenue lines may not keep pace with prior assumptions, which feeds into slightly lower valuation estimates.

- These analysts also highlight that any stumble in cost control or capital deployment could pressure returns, making them reluctant to ascribe higher P/E or P/B multiples at this stage.

What's in the News

- Equity Bancshares reported first quarter 2026 net charge-offs of US$1.4 million, or 0.10% annualized, with the allowance for credit losses at 1.18% of outstanding balances and the allowance plus purchase discounts on loans at 1.77% of outstanding balances. (Source: Key Developments)

- From January 1, 2026 to March 31, 2026, the company repurchased 500,000 shares for US$22.37 million, representing 2.64% of its shares. (Source: Key Developments)

- Under the buyback announced on September 26, 2025, Equity Bancshares has completed the repurchase of 672,338 shares for US$29.55 million, representing 3.54% of its shares. (Source: Key Developments)

Valuation Changes

- Fair Value: Holds steady at $51.60, with no change between the prior and updated estimates.

- Discount Rate: Edged lower from 7.12% to 7.11%, a very small adjustment to the rate used to discount future cash flows.

- Revenue Growth: Remains effectively unchanged at 33.76%, indicating the same projected pace for top line expansion as before.

- Net Profit Margin: Stays essentially flat at 49.16%, keeping the same assumption for how much of each dollar of revenue is expected to turn into profit.

- Future P/E: Is broadly unchanged at about 6.11x, reflecting a stable view of how many times forward earnings the stock might trade on in the model.

Key Takeaways

- Expansion into high-growth mid-sized markets and strategic M&A enhance geographic reach, scale, and long-term revenue opportunities.

- Investment in digital banking and diversified services improves income mix, operational efficiency, and supports stable earnings growth with strong risk management.

- Rising digital competition, demographic shifts, sector concentration, and regulatory costs threaten long-term growth, profitability, and customer retention for the bank.

Catalysts

About Equity Bancshares- Operates as the bank holding company for Equity Bank that provides a range of banking, mortgage banking, and financial services to individual and corporate customers.

- The company's recent merger with NBC Bank expands its geographic reach into Oklahoma City-one of the Midwest's fastest-growing metro areas-positioning Equity Bancshares to benefit from rising demand for community-focused banking solutions in mid-sized markets; this is likely to drive above-average loan growth and revenue expansion over the long term.

- Accelerated adoption of digital banking tools and improved treasury, debit/credit, mortgage, trust, and wealth management offerings have resulted in increased non-interest income, while ongoing investments in digital platforms are expected to lower operational costs and improve net margins.

- The strong pipeline of commercial and C&I loan originations, alongside continued small business growth in regional economies, supports future commercial lending volume and fee income, which should stabilize and grow both revenue and earnings.

- Strategic consolidation through disciplined M&A (with a pipeline of acquisition targets in the $250 million–$1.5 billion range) provides opportunities for scale, cost synergies, and improved operating leverage, supporting sustained net margin and EPS growth.

- Capital flexibility from recent capital raises and a robust TCE ratio (10%+) allows the company to maintain conservative credit standards and proactively manage credit risk, supporting stable earnings and potential for higher book value compounding.

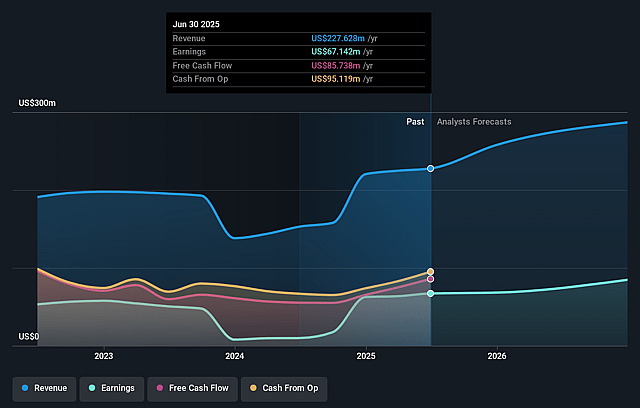

Equity Bancshares Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Equity Bancshares's revenue will grow by 33.8% annually over the next 3 years.

- Analysts assume that profit margins will increase from 11.2% today to 49.2% in 3 years time.

- Analysts expect earnings to reach $259.6 million (and earnings per share of $11.98) by about June 2029, up from $24.7 million today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 6.2x on those 2029 earnings, down from 39.1x today. This future PE is lower than the current PE for the US Banks industry at 11.6x.

- Analysts expect the number of shares outstanding to grow by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.11%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Accelerated shift to digital banking and increased consumer preference for seamless, technology-driven banking services may favor larger national banks and fintechs, potentially leading to customer attrition and stagnating revenue growth for Equity Bancshares if it cannot keep pace with innovation.

- Ongoing demographic trends, such as rural depopulation and the aging of populations in Midwest and South Central U.S. markets, could gradually erode the bank's core customer base, posing long-term risks to both deposit and loan growth (revenue impact).

- High reliance on commercial real estate (CRE) and sector-specific exposures (e.g., the cited QSR relationship and agriculture lending) increases vulnerability to sector downturns, which could result in elevated credit losses and higher non-performing assets, negatively affecting net earnings and asset quality.

- Industry-wide consolidation and M&A activity may favor banks that can achieve rapid scale and digital efficiencies; as a smaller regional player, Equity Bancshares could face rising operational costs and lose market share if unable to compete on technology and pricing, putting downward pressure on net margins.

- Prolonged cost pressures from tightening regulatory and compliance requirements could disproportionately impact smaller community banks like Equity Bancshares, driving up operational expenses and squeezing net margins and profitability over time.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $51.6 for Equity Bancshares based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $58.0, and the most bearish reporting a price target of just $47.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $528.1 million, earnings will come to $259.6 million, and it would be trading on a PE ratio of 6.2x, assuming you use a discount rate of 7.1%.

- Given the current share price of $46.64, the analyst price target of $51.6 is 9.6% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Equity Bancshares?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.